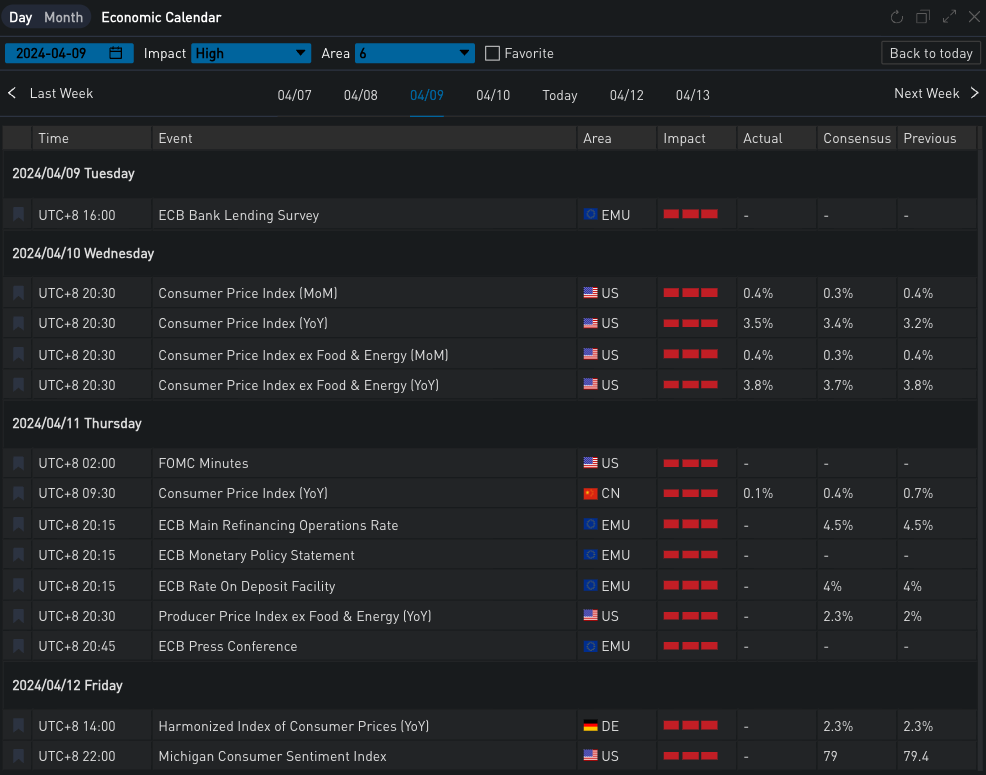

The full-scale higher-than-expected US CPI data yesterday (10 APR) dealt a heavy blow to the market. Specifically, the March CPI increased by 3.5% year-on-year, higher than both market expectations and the previous value, while the core CPI, excluding food and energy costs, increased by 3.8% year-on-year, 0.1% higher than expected and on par with the previous value. According to the report, the surge in gasoline and housing expenses contributed nearly 50% to the CPI increase in March. There was also growth in car insurance, medical expenses, and clothing costs. In the core index, the growth rate of goods costs slowed, while the service sector picked up again.

Following the release of the data, US Treasury yields jumped sharply, with the ten-year yield breaking above the 4.5% mark and the two-year yield approaching the significant 5% threshold, currently reported at 4.967%. The 5/30-year yield curve inverted for the first time since September last year. Consequently, the swap market has delayed the timing of the expected rate cuts. As of now, the probability of no rate cut in June has risen from the original 50/50 to 83.5%, with less than two rate cuts expected for the entire year. The postponement of rate cuts has put pressure on US stocks to fall, especially for companies with higher borrowing costs, with the three major stock indexes closing down around -1%. From another perspective, although expectations for rate cuts have been continuously lowered, the US economic data remains very strong. At this juncture, instead of betting on a direction, reducing risk exposure might be a better choice?

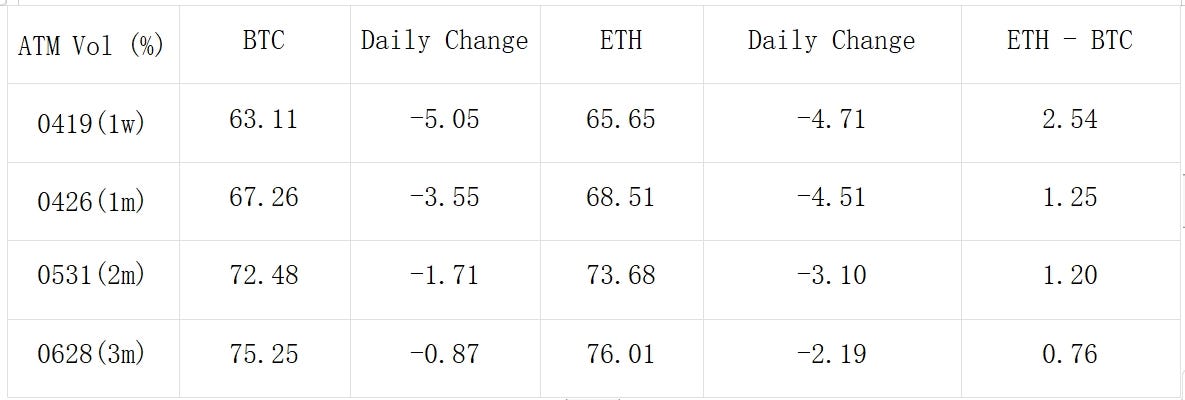

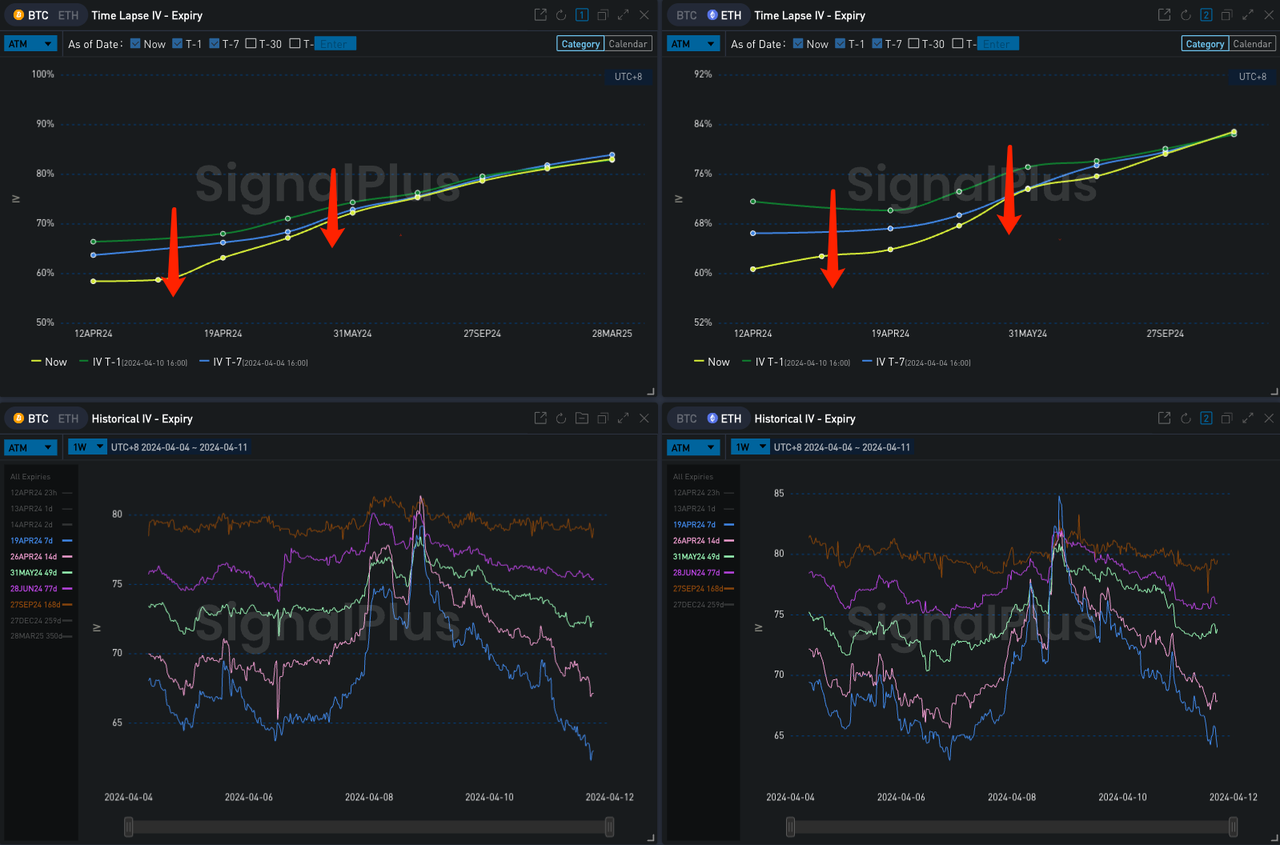

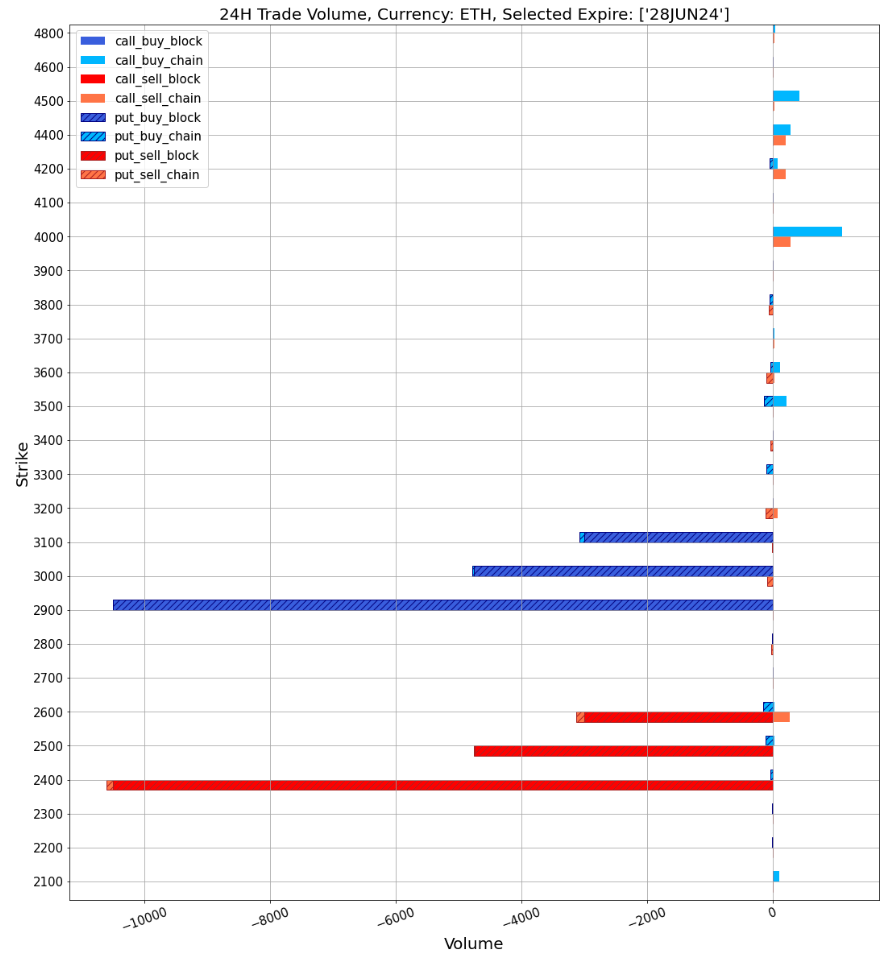

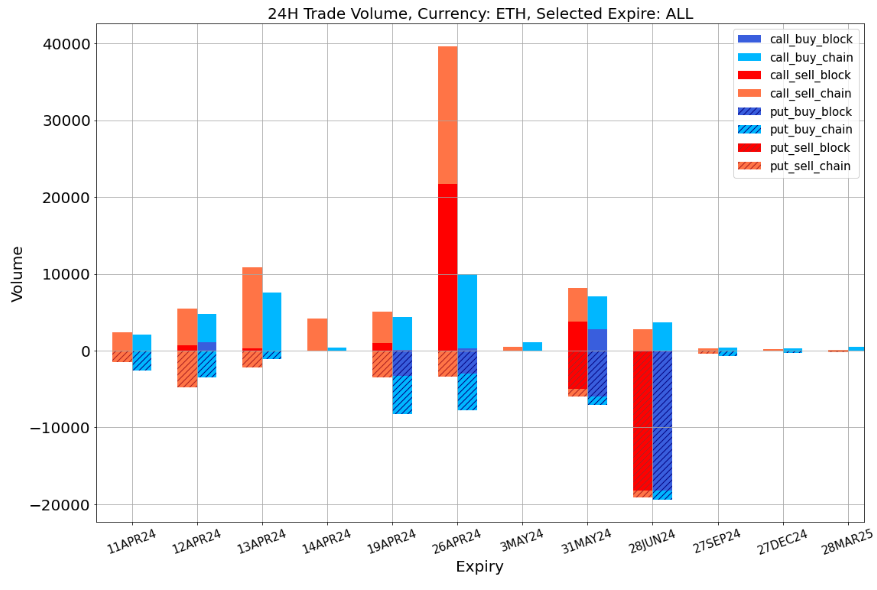

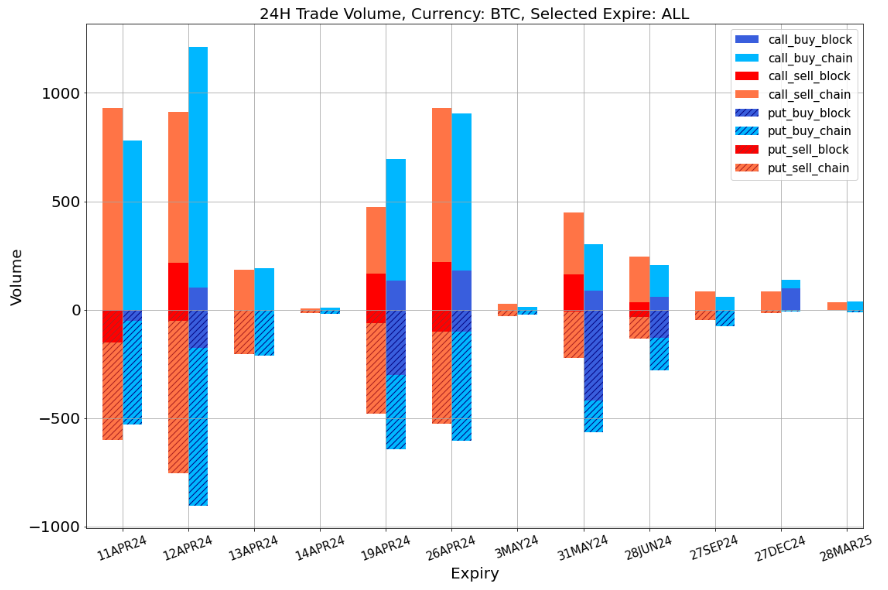

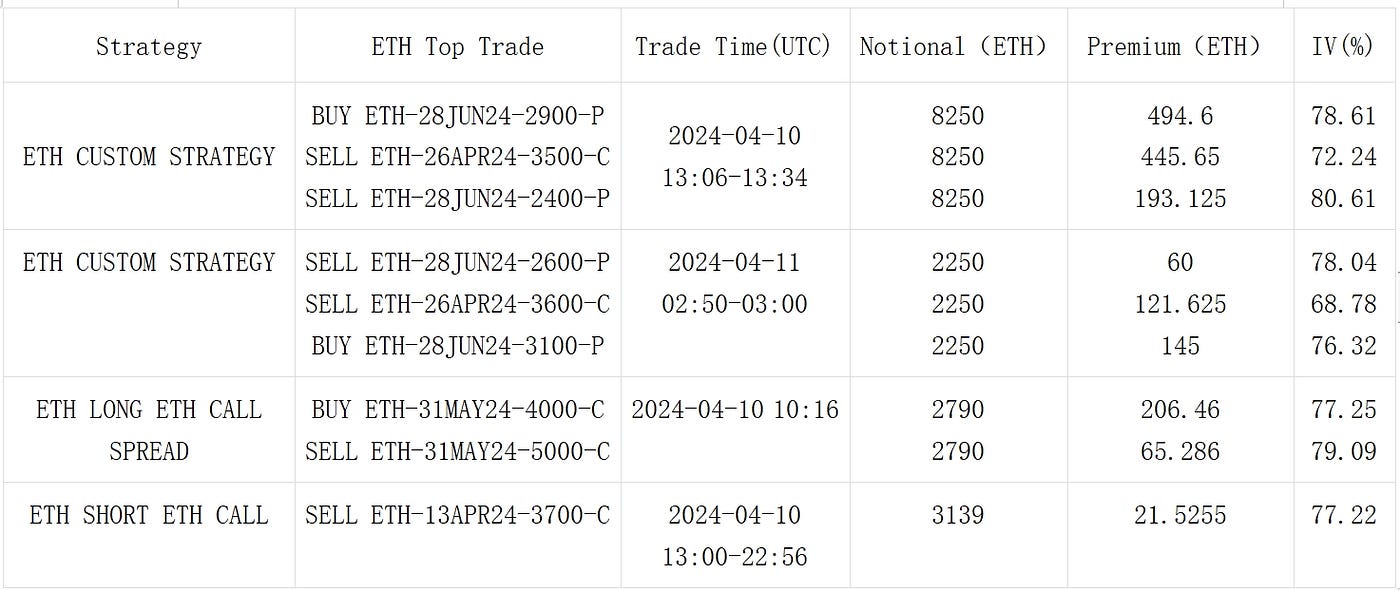

In the realm of digital currencies, BTC rebounded above 70K, with the long-term oscillation trend still within the contraction range. Looking at the options, the statistical data reveals a still significant IV/RV (Implied Volatility/Realized Volatility) exposure. The front-end implied volatility continues to decline under the massive sell-off of bullish options, where ETH’s Call options at the end of April closely followed the trend of BTC yesterday, presenting an overwhelming sell-off of bullish options. Additionally, the large volume of Put Spread Protection bought for ETH at the end of June is also a focus of market attention, while BTC’s Put options also gained favor in the market yesterday.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments