Things certainly got a lot trickier for the Fed.

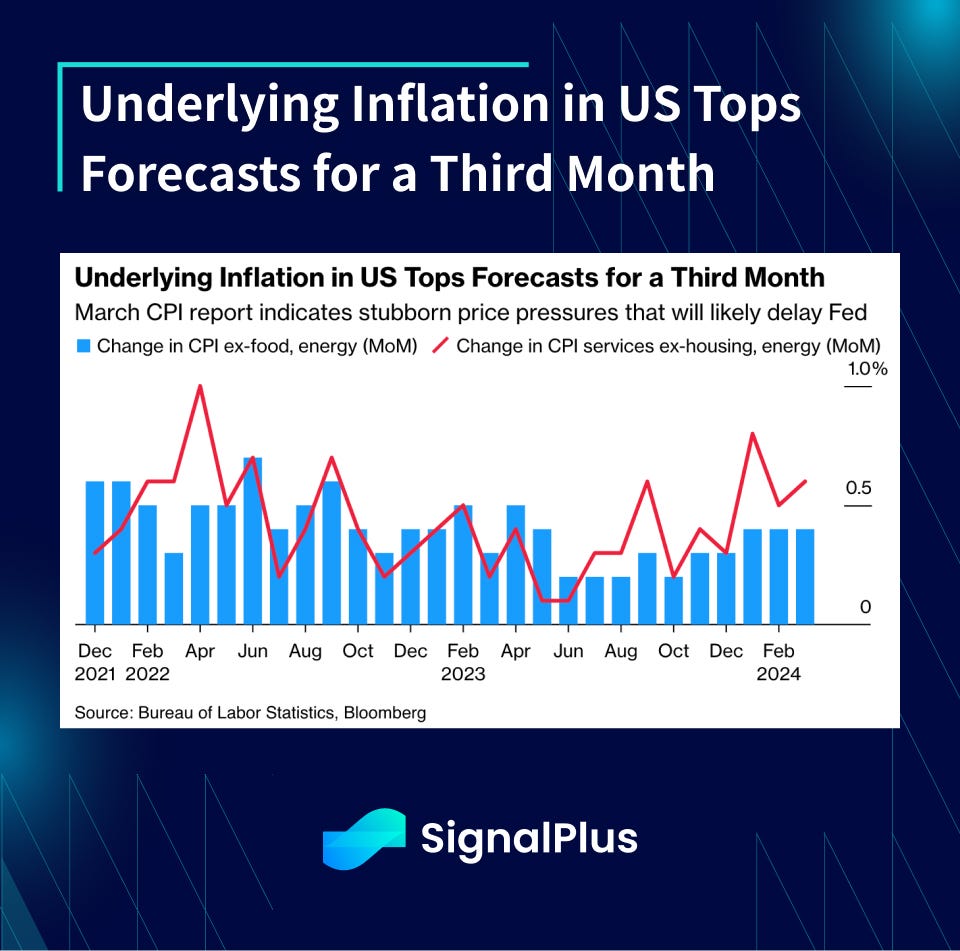

Markets were dealt with a couple of uncooperative inflation prints, particularly with Wednesday’s CPI which showed core prices moving in the wrong direction. March USD CPI rose 0.4% across both core and headline, with the headling YoY pace rising to 3.5% vs 3.2% last month, and core steady at 3.8%. Strength came from another +1.1% increase in energy, 0.5% in services and 0.4% in rental related fields. Supercore CPI rose another 0.65% MoM.

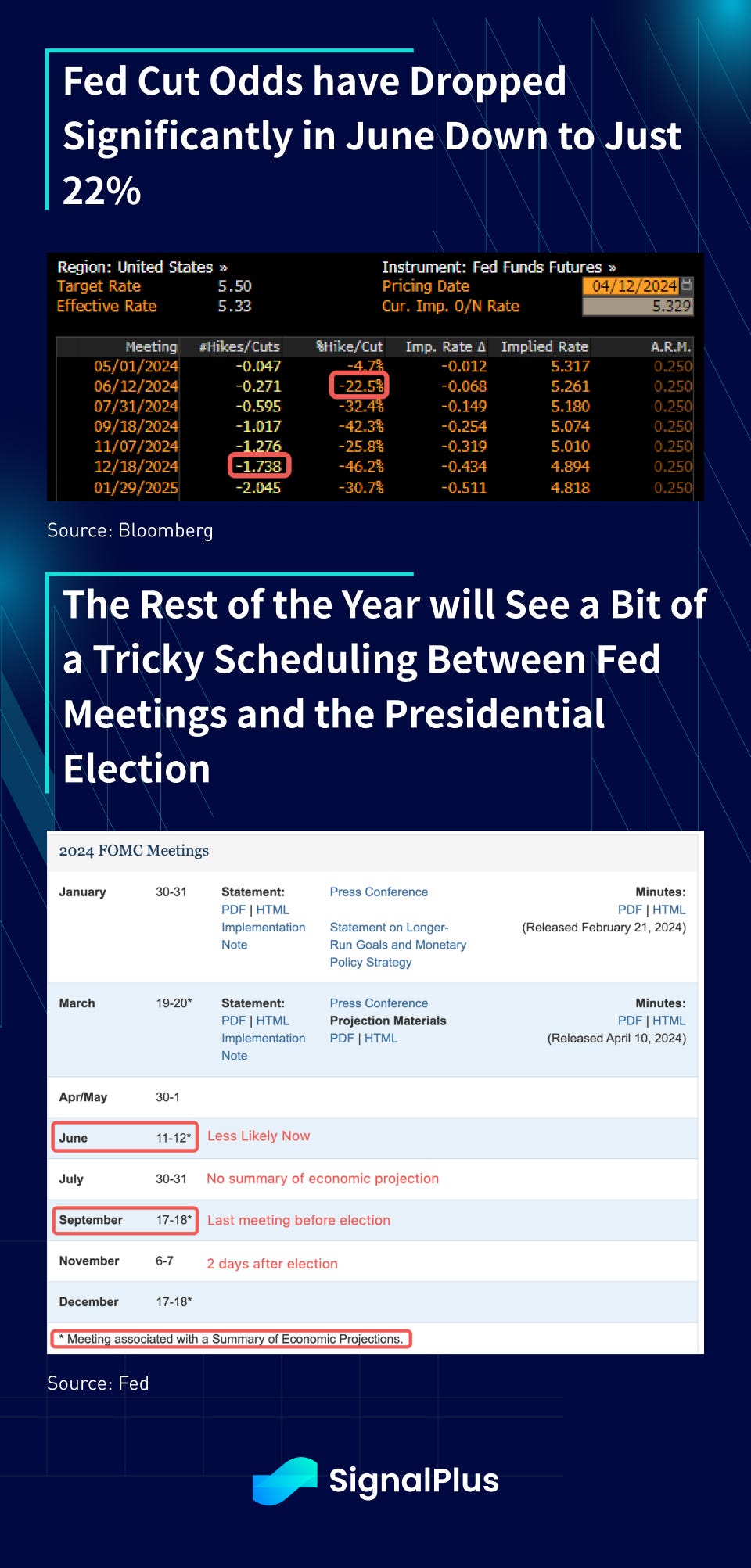

For those keeping track, this is the 3rd consecutive upside miss in core CPI, and has pretty much invalidated the ‘gradual disinflation progress’ that the Fed was hanging on to justify their 3x cuts in the dot-plot. Over the last few sessions, 1y1y rates have jumped by +45bp, June cutting odds have collapsed to ~22%, and the USD has rallied against most currency pairs, as the (ex-equity) market is pretty much giving a vote of no-confidence to Powell’s dovish pivot.

Thankfully for risk markets, yesterday’s PPI was much warmer to the touch, with both headline and core rising 0.2% in March, following respective gains of 0.6% and 0.3% in February. While the headline YoY pace has slowed from the March 2022 records of 11.7%, the recent print of 2.1% YoY is still moving in the wrong direction vs 1.6% in February, and still raising some questions on the validity of the disinflation narrative.

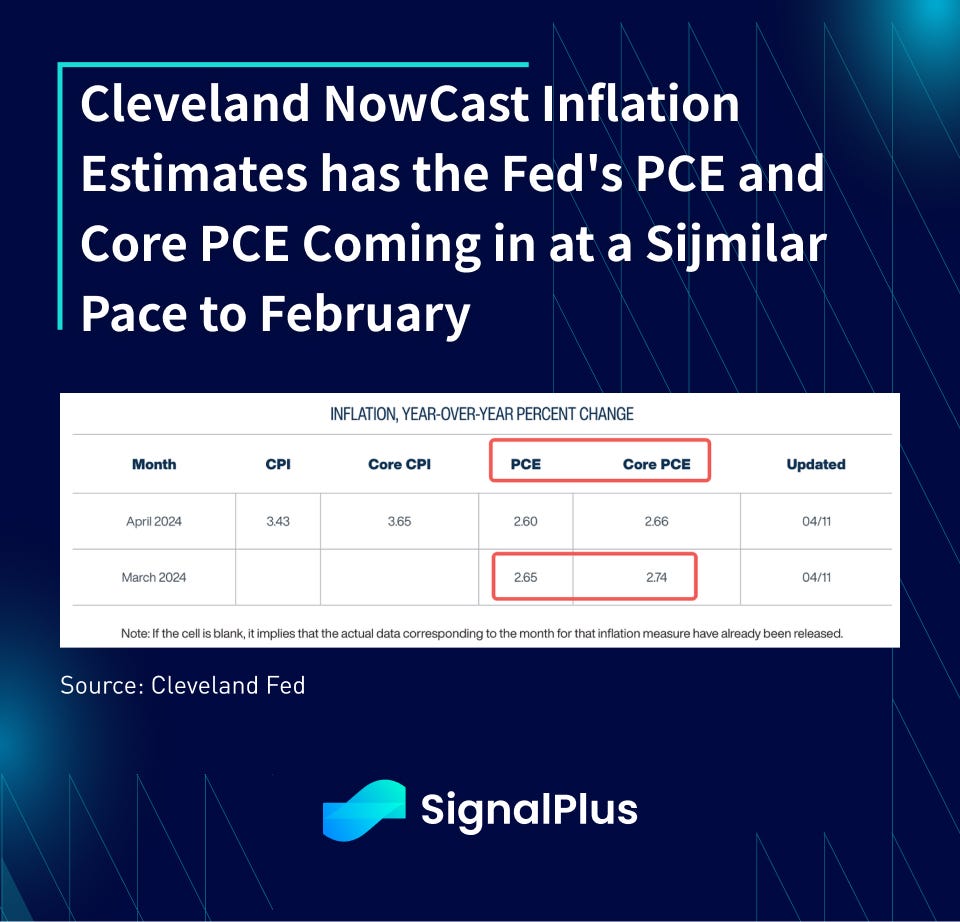

According to Citi and Cleveland estimates, based on the elements from CPI/PPI, the Fed’s preferred core PCE measure is now expected to come in at 0.26% MoM in March, similar to the pace in February, and would still see a fall in the YoY pace from 2.8% down to 2.7% due to base effects and index composition. Core services excluding housing is expected to come in at 0.29% MoM, while supercore CPI is still expected to remain high at 0.65% MoM.

Unsurprisingly, Fed speakers are busy walking back some of their earlier disinflation bravado, with Boston Fed’s Collins suggesting that “it may just take more time than previously thought” and that “CPI figures in Q1 came higher than I’d hoped”. Richmond Fed Barkin stated he wanted to see more “broader disinflation, not just in goods” after the notable overshoot in super-core services in Q1. Lastly, NY Fed Williams address in his Q&A that “rate cuts don’t appear imminent”, alluding that “there are definitely circumstances that we would need higher interest rates, but that’s not my base case.”

Rate cut odds have been pushed down to -22.5% for June, with less than 2 full cuts priced in for the full year now. Furthermore, in terms of scheduling, things are also much trickier now given the timing of the Fed meetings for the rest of the year.

- June: Low chance for cut

- July: No release summary of economic projections (less important meeting, likely to keep same pace as June)

- September: Last meeting before election

- November: couple of days right after US election

As we can see, should the Fed pass in June (22%), they are unlikely to cut in July (32%) unless data moves dramatically in their favour over a single month (controversial), especially with the meeting being a ‘lighter’ ones being a non-’SEP’ meeting. The next meeting will in September, when the US presidential election campaigns are in full swing, and the Fed will be heavily pressured politically not to act too favourably towards one candidate over the other. Furthermore, the 2H of the year is also likely going to be much more challenging for inflation given much less friendly base effects versus 2H23. Finally, following that, that leaves us with November, which takes place just a few days immediately after the election results; imagine the media headlines and conspiracy theories should the Fed stay on hold all year but decides to cut 2 days after a potential President Trump victory. Needless to say, the Fed has gotten themselves in between a rock and a hard place.

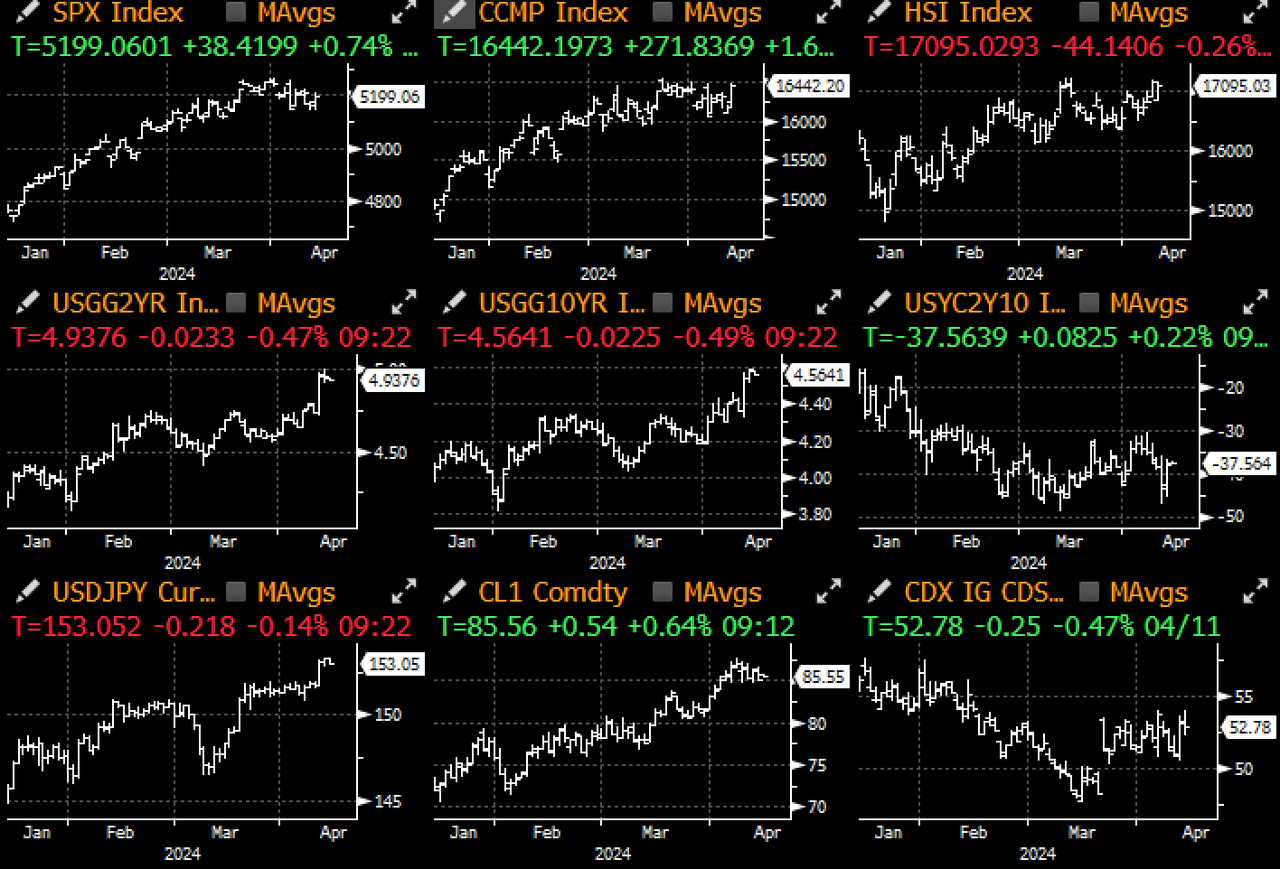

Bond markets have also voted very loudly. With 2yr yields making a rapid approach to 5%, and 10y above 4.50%, Wednesday’s 10yr auction was a terrible affair, with a massive 3.1bp tail and the weakest bid to cover ratio at 2.34x. Direct bidders also saw the lowest take down in 2.5 years at just 14.2%, and street dealers being left with a substantially larger share.

Yesterday’s 30yr bond yield was slightly better, but still on the soft side despite the yield consensus. Tail was 1bp with weak bid to cover, direct bidder participation, and dealers being left with 17% of the float vs 14% on average.

The YTD sell off in bonds have started to hit more concerted levels, with RSI starting to trade into over-sold (prices) territory, though understandably investors are less sanguine about having duration exposures here given the unfriendly mix of inflation with a somewhat cornered Fed.

Despite the doom-and-goom, 3 guesses as to which asset class took it in stride and kept coming back like a prized fighter? Well, long term readers would know the answer already, but equities took the initial rate cut disappointments but felt comfortable to focus on ‘good news is good news’ as stock prices recovered almost all their WTD losses post the economic releases.

The SPX’s incredible outperformance of everything (perhaps except crypto) puts their implied earnings yields vs treasuries at the lowest in almost 20 years, but that has not deterred equity investors from piling into the winners with no observable systemic risks on the horizon.

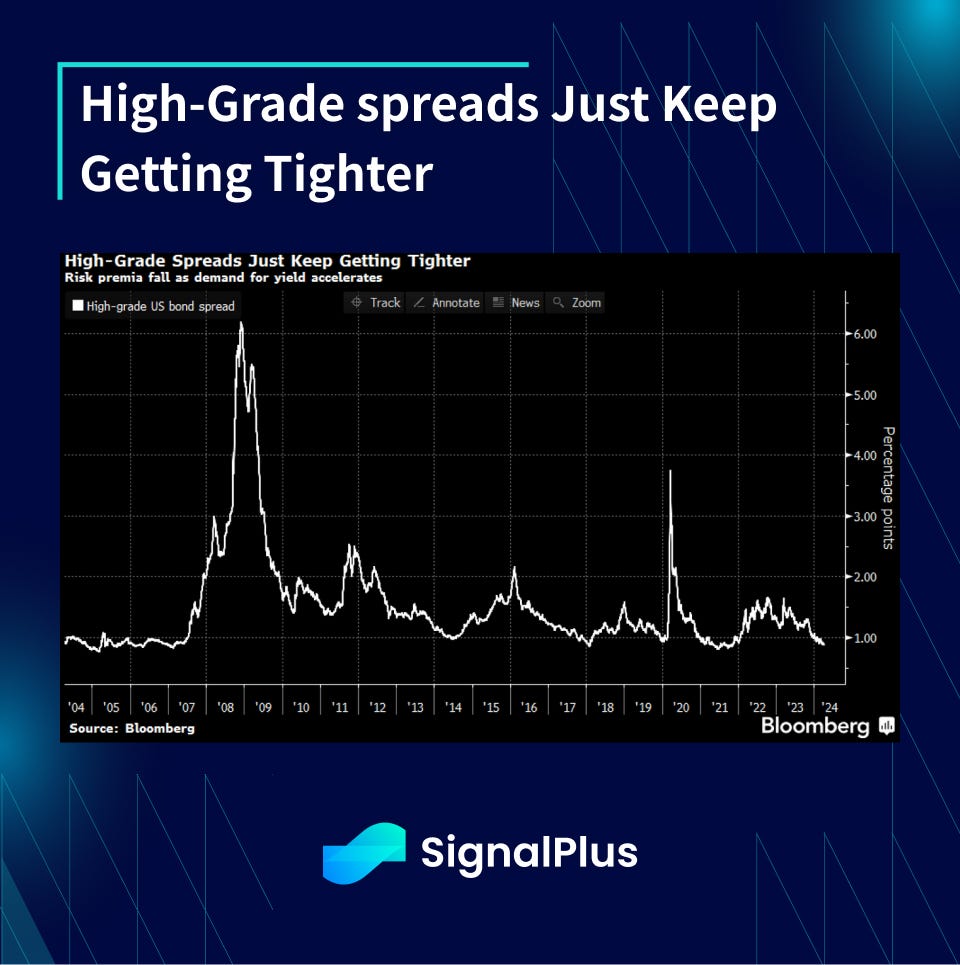

A similar phenomenon is taking place in corporate bonds as well, where the expectations of a slowdown in QT (ie. Tapering the taper) is causing more outright buying of corporate bond paper, thereby keeping high quality IG spreads at some of the tightest levels in history.

Finally, the billion-dollar question as to when rates would have an effect on stocks, Citi did an analysis where they studied previous ‘hawkish’ scenarios and concluded that we are still some ways away (~40–50bp) from the current rate move being detrimental to equities. Investors also see this as exceptionally unlikely as they believe (rightly) that the Fed is going to lean dovish into strong growth & inflation, so it’s almost unfamothable that they would be willing to completely take out all of the implied rate cuts. As such, investors are choosing to still focus on corporate earnings (coming up), economic growth (strong), and friendly Fed rhetoric to suppor equity sentiment higher. The actual rate cuts are just a bonus as long as the current economic trajectory holds up (for now).

In crypto, BTC prices have been orderly around 70k as dealers have reported some hedging and profit-taking of longs as majors are unable to make any significant headway higher. ETF inflows have slowed and sentiment has been more subdued as we head into the halving, with more sideways price action likely expected in the near future.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments