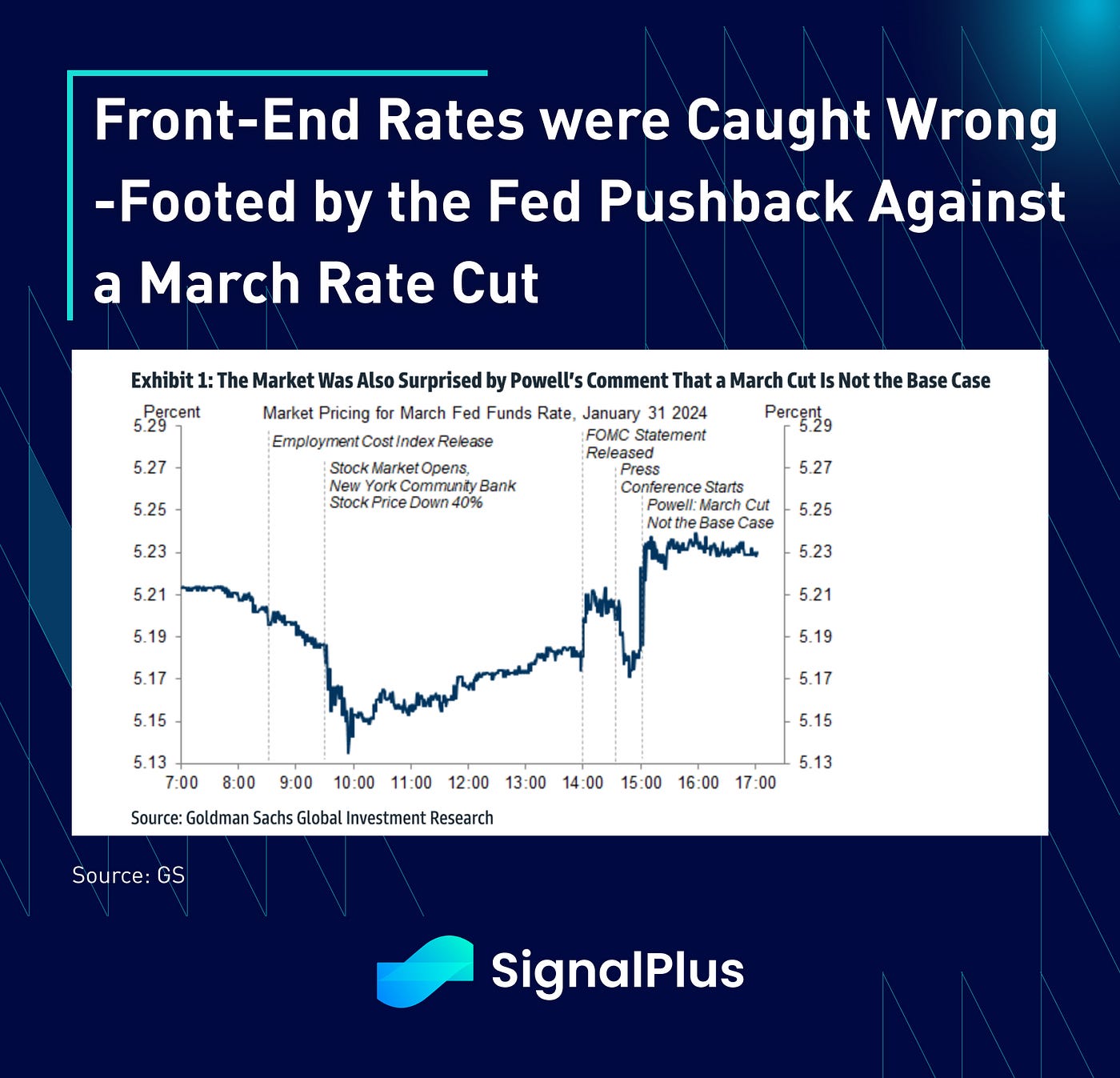

TL;DR — “The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent” and [Powell] “doesn’t think it’s likely that the Fed will cut rates in March”.

Yesterday’s FOMC meeting and market price action can be pretty much summed up in our opening quotes. While the Fed expectedly removed the hiking bias from their official statement, the market was caught off-side from that explicit hawkish push-back, even if one were to question what “greater confidence” ultimately means. In any case, this was taken as a direct Fed rebuttal against the growing expectations of a March cut, causing OIS rates to jump 10bp from the lows (unwinding the gains from the earlier weak ADP and Employment Cost Index) and easing probability to ~30%.

At the 2:30 press conference, Powell initially made attempts to ‘hedge’ against the hawkish statement by remarking that:

- Policy rate is “well into restrictive territory”.

- It’ll be appropriate to “dial back policy restraint at some point this year”.

- FOMC participants “have confidence that has been increasing but we want greater confidence” regarding easing inflation.

- “It is not that we are looking for better data but continuation of the better data.”

- On inflation specifically, Powell noted that the “composition of inflation data is less important” than the overall level of inflation, addressing the ongoing divergence between goods and services inflation.

Though any hopes of a dovish reversal were quickly dashed when the Chairman ended the Q&A by noting that:

- “There was no proposal to cut rates at this meeting.”

- There is “still a ways to go towards a soft-landing” and

- [Powell] “Doesn’t think it’s likely that the Fed will cut rates in March”.

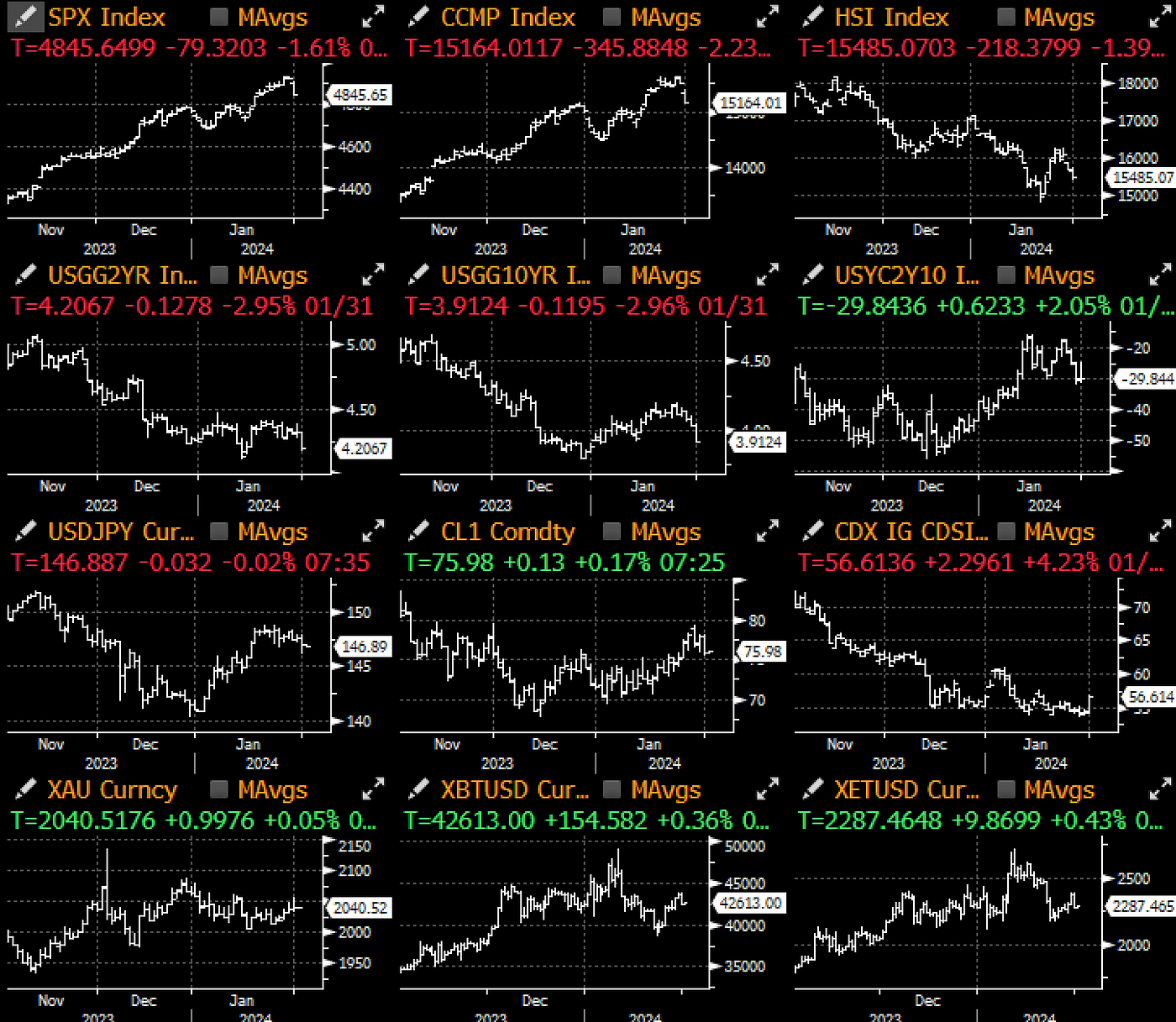

The last statement served as the KO punch which sent 2yr yields ~8bp higher and equities to plummet ~1.5% lower on the day. It would appear that the real 2024 is just about to get started.

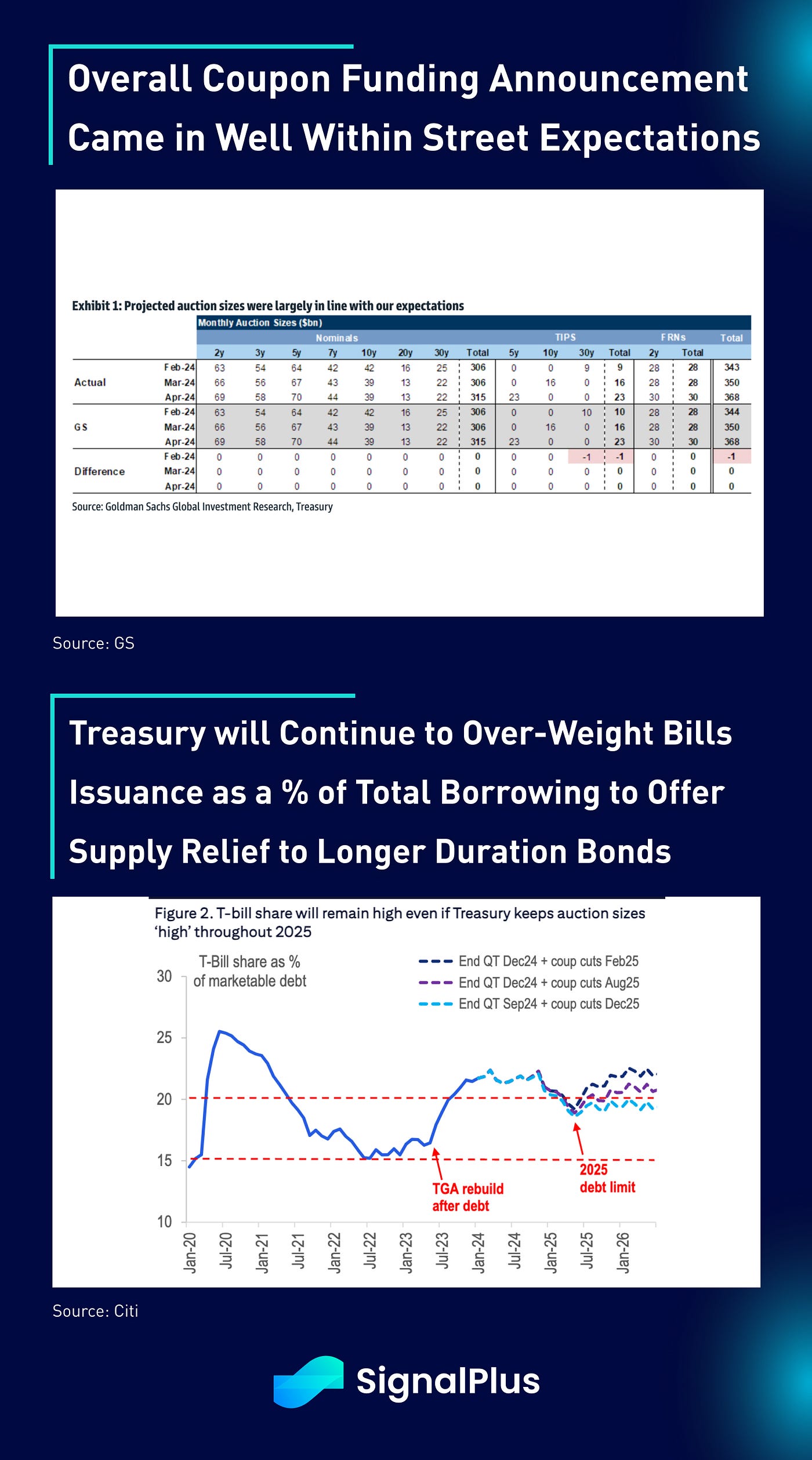

Outside of the Fed, there were other events on the agenda which were worth nothing. Firstly, the much anticipated coupon supply announcement came fully within market expectations and acted as a relief on bond prices. While the Treasury boosted the size of its quarterly issuance for a 3rd straight time, officials suggested that this will be the last increase for 2024, and the size of the supply ($121bln next week in 3y/10y/30y paper) is well within the cadence of the pace set in last November. Furthermore, the Treasury also confirmed that it will announce the start-date of its new buy-back program during the May refunding announcement, which is designed to assist with cash management and liquidity improvement for off-the-run treasuries.

On the maturity mix, the Treasury stated that it expects to at least maintain the current T-bill auction sizes into the end of Q1, followed by a small reduction into the subsequent quarter. In any case, this will keep T-bills share of total issuance above the recommended range, with the Treasury continuing to sacrifice some degree of funding prudence to offer supply relief to longer duration securities.

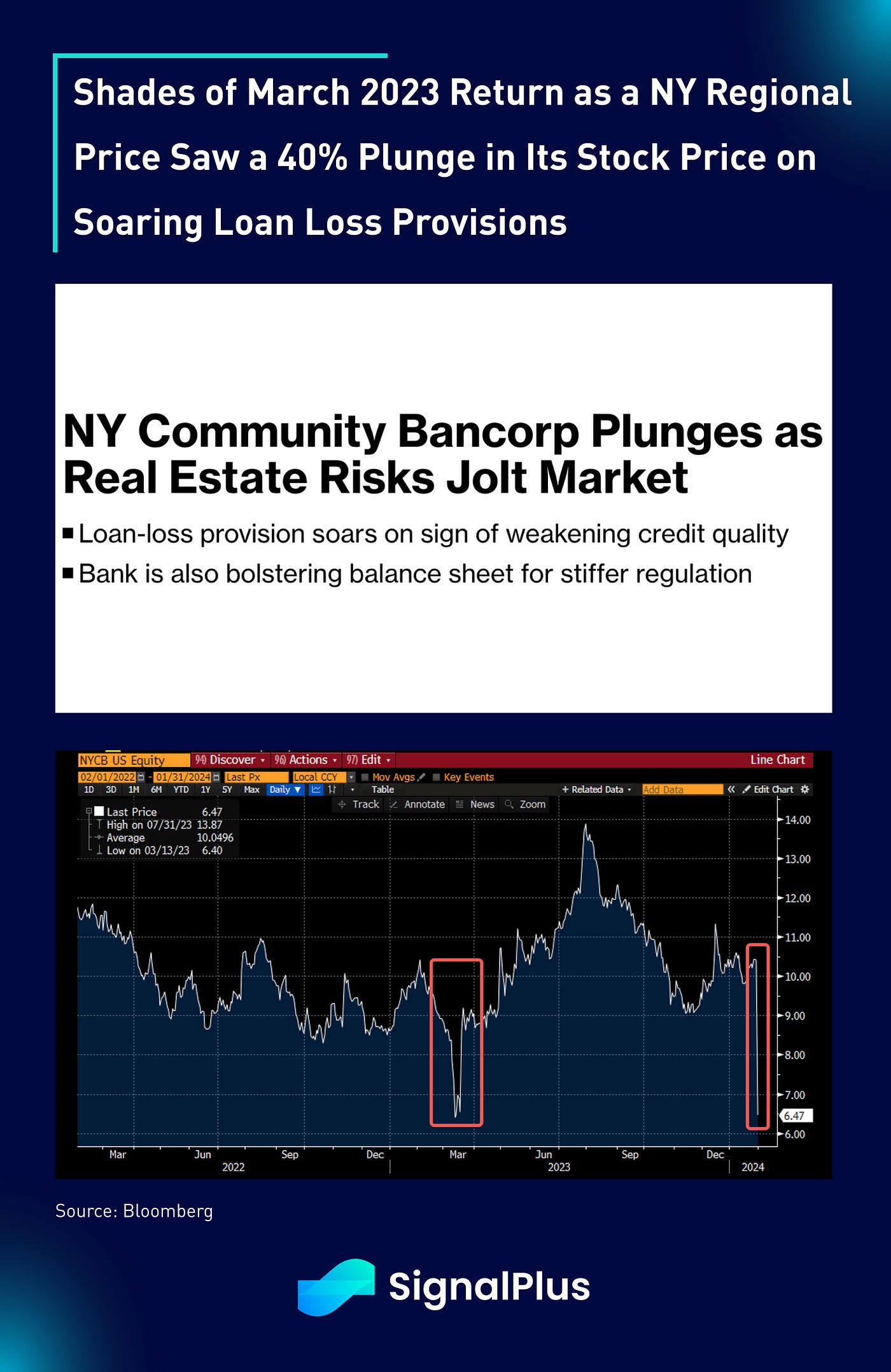

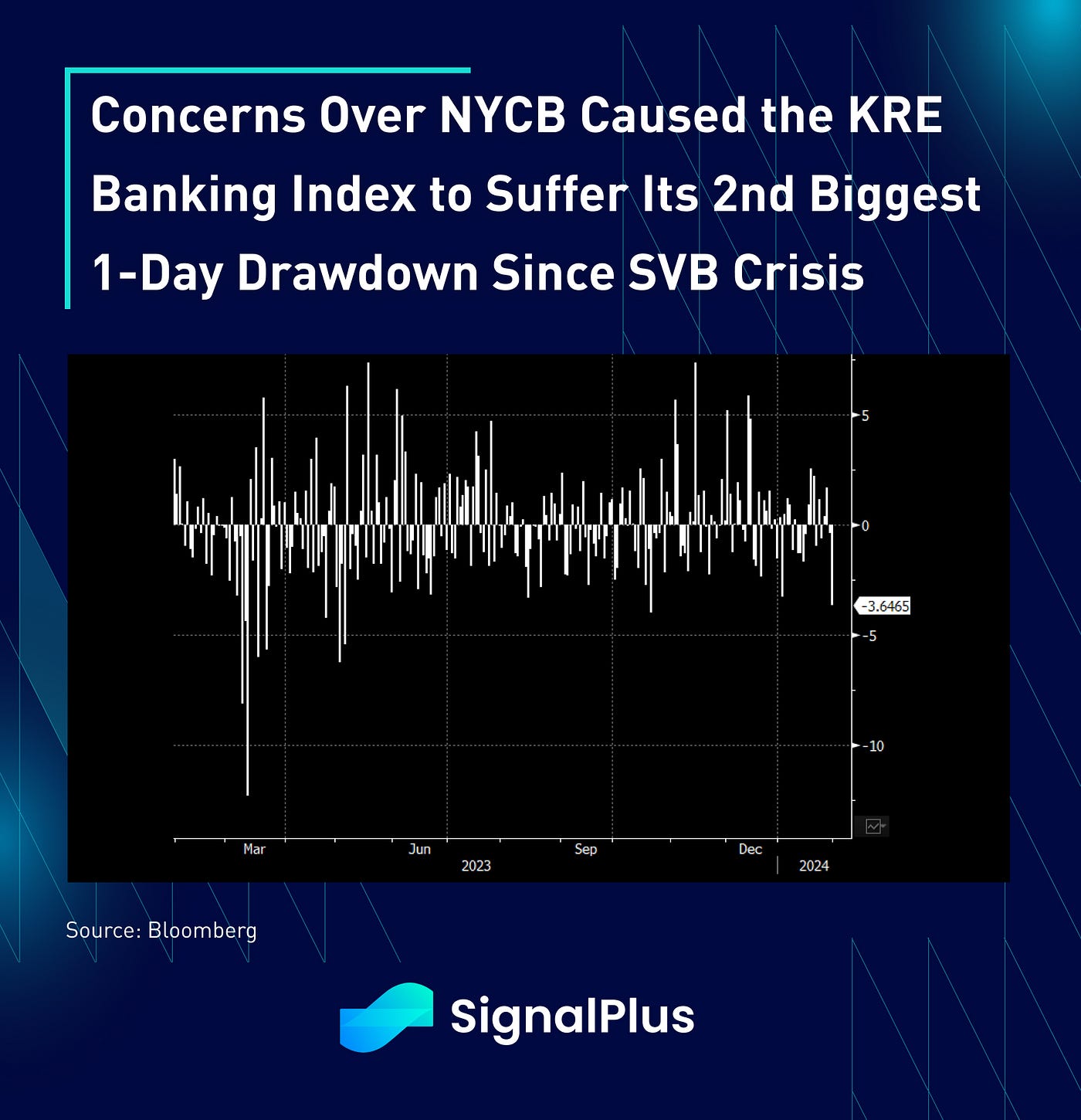

On the other hand, more ominous clouds were forming over weaknesses in ADP (+107k vs +158k last month), employment cost index (slowest annualized pace since 2021), Chicago PMI (46 vs 47.2), and a 40%(!) price drop in a New York Community Bancorp (a NY regional bank) as it announced dividend cuts during its earnings announcement due to substantial loan impairments.

The bank, which acquired a part of Signature Bank last year, stated that it ratcheted up its loan-loss reserves in anticipation of further weakness in commercial property markets, as 30 day+ delinquent loans jumped 48% higher in Q4 last year. Total charge-offs soared to $185mm in the quarter, which was more than its combined impairments over the past decade. Net loss for the bank arrived at -$252mm for Q4 versus a +$206mm gain as expected by analysts, and announced a ~70% cut in dividends payout as the firm sought to conserve cash.

While credit analysts appear to universally deem this to be an isolated and stock specific event, shades of March 2023 are still fresh in many people’s minds, and the rolling off of the BTFP facility in March certainly didn’t help to assuage fears. The US KBW banking index dropped by as much as -5.5% on the day, before recovering to around a -3% loss at the market close.

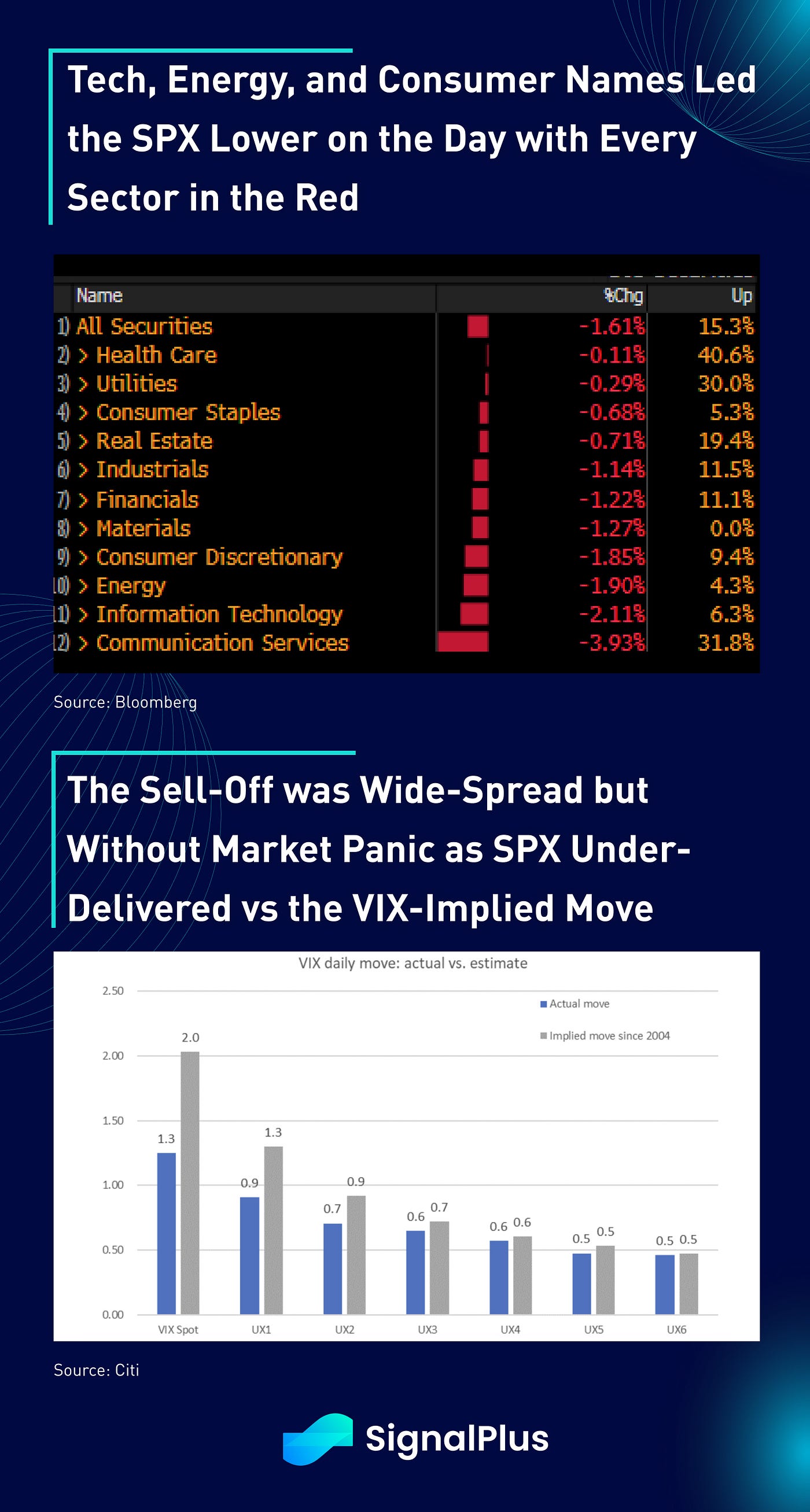

In equities, outside of the hawkish Fed and NYCB scare, earnings disappointed across the board with AMD (-2.6%), Samsung (-2%), Google (-7%), Microsoft (-2.5%), and Disney (-1%) all failing to live up to the lofty heights set by the current prices. Tech, energy, and consumer discretionary sectors led the way lower, though there was no widespread panic as the underlying SPX move actually underperformed the VIX-implieds based on historical data.

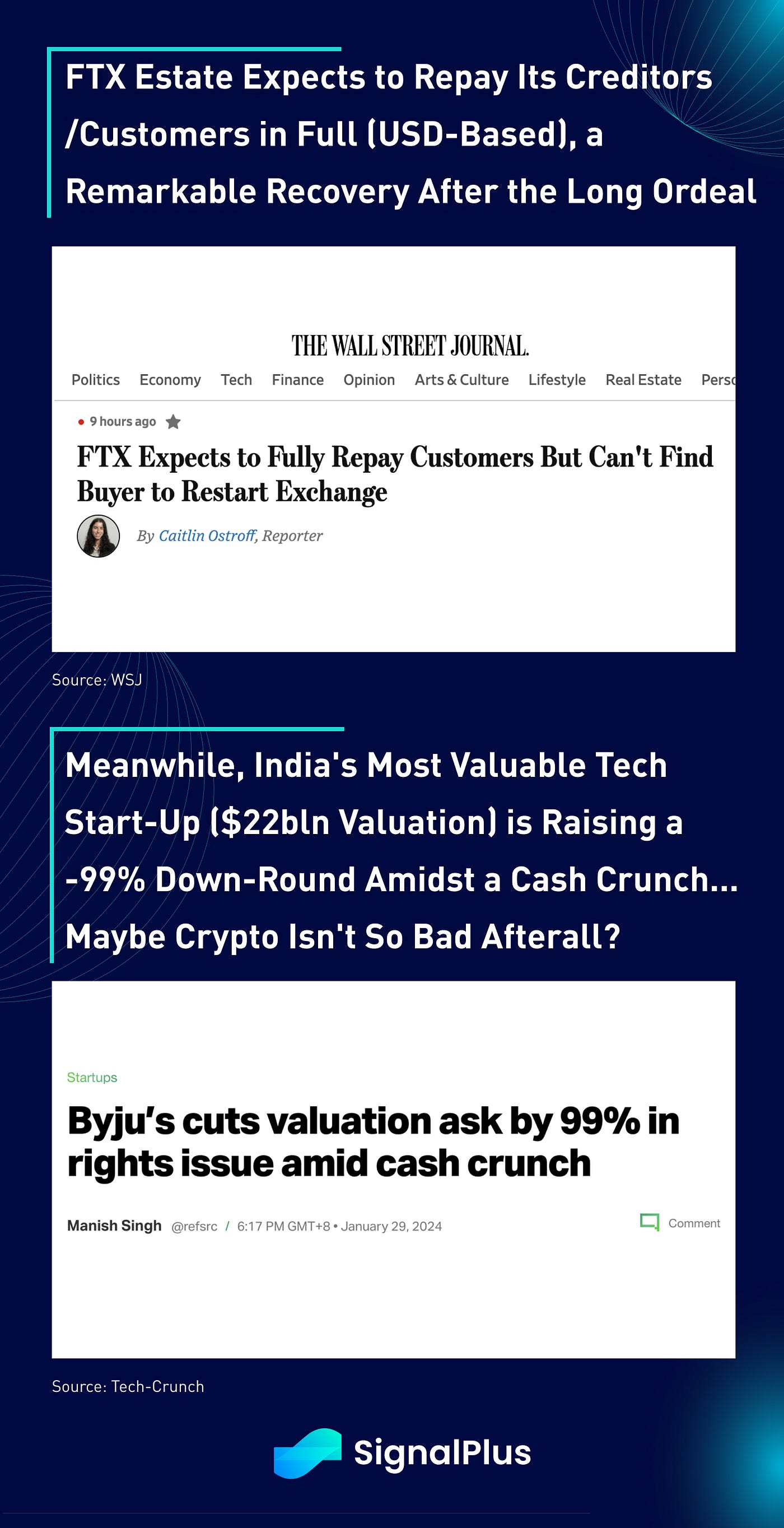

In crypto, prices didn’t participate in the FOMC fireworks (yet), though we appear to be getting confirmation via the court hearing that the defunct exchange now expects to repay its customers in full, but will scrap its plan to restart FTX 2.0 due to the difficulty in sourcing a buyer. Despite the mainstream villification of the sector (deservedly in some degree), the largest scandal ridden bankruptcy in crypto will now see a par return (USD based, not coin based), substantially better than the ‘pennies-on-the-dollar’ recoveries seen in many VC investments, private equity secondaries, Chinese property bonds, and US commercial real estate funds. Maybe crypto isn’t so bad after all?

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments