After the BoJ delivered a perfectly executed “dovish hike”, the Fed carried the mantle with its own “dovish stay”. While questions swerlled over how the FOMC would handle the recent bout of re-inflation, Chairman Powell delivered an equivocally dovish message which basically proclaimed that rate cuts are going to happen even if growth and inflation were to come in above forecasts.

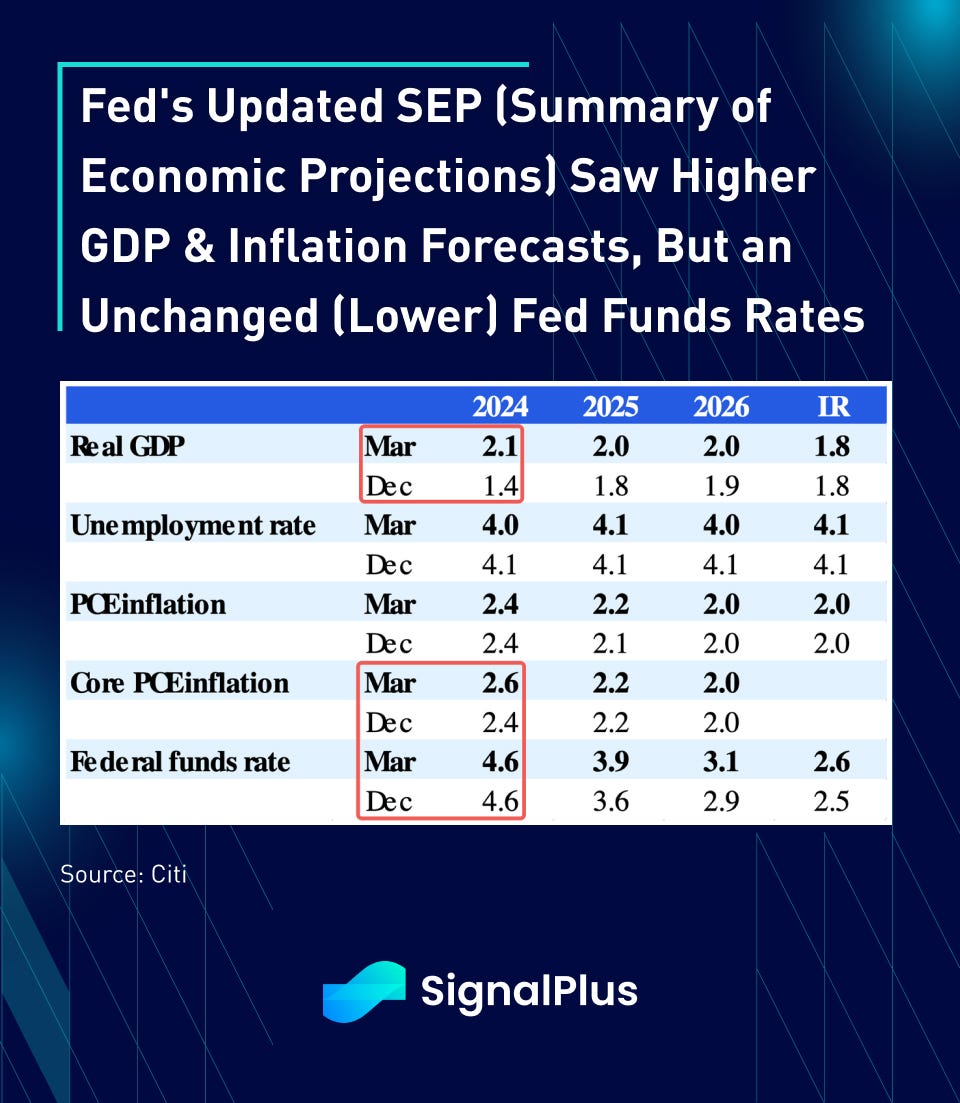

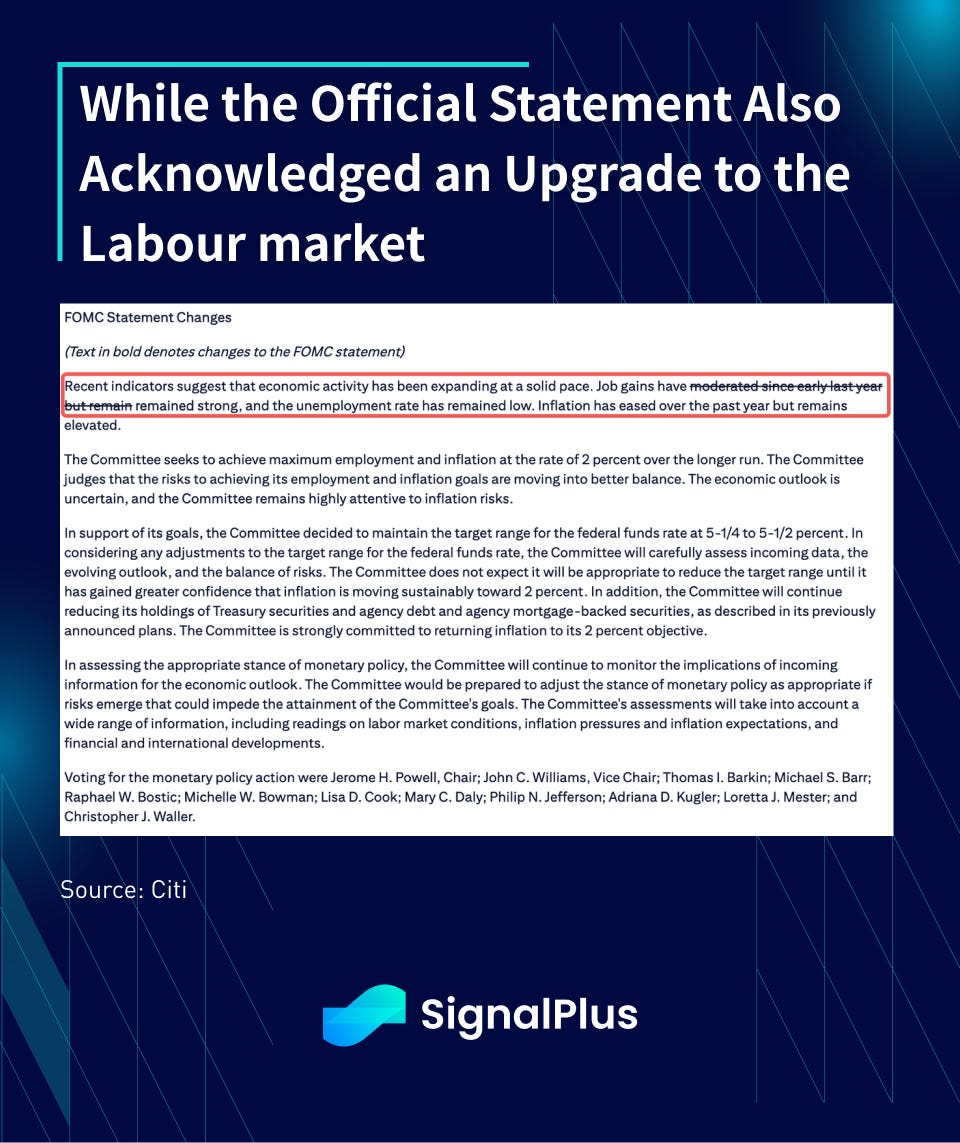

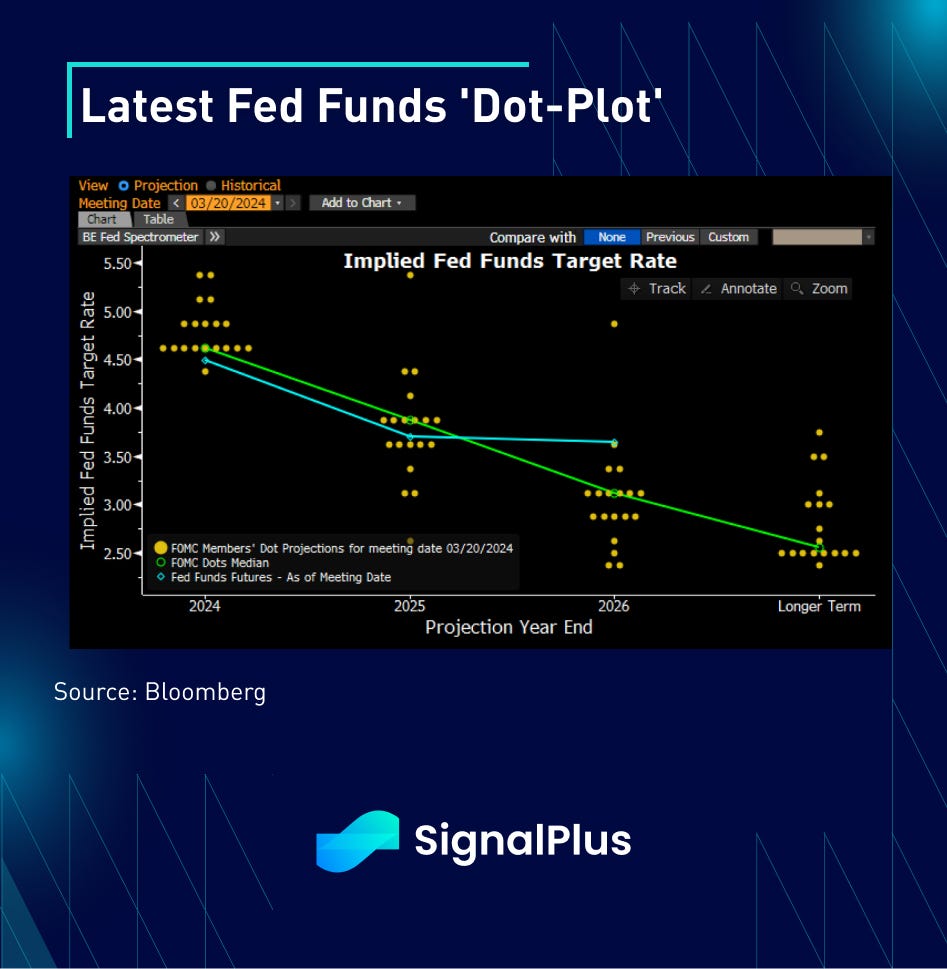

Traders were quick to note the unchanged median dot-plot (4.6% FF for 2024), despite significant upgrades to core PCE inflation (2.6% from 2.4%), real GDP growth (2.1% from 1.4%) and the unemployment rate (4.0% from 4.1%, removal of the word “moderated” from the official statement). The Fed attempted a small compromise by moving up the 2025 terminal FF rates to 3.9% (from 3.6%), but that did to dissuade the risk-on move as the Fed has pretty much ‘shown its hand’ with the risk-on tilt.

The dovish-sentiment only served to gain pace as we headed into the Q&A, with Powell dismissing the recent inflation surprises with a series of subtle comments:

- While admitting that the January and February price data were hotter than expected, the FOMC also expected the disinflation path would be “bumpy”

- Powell explicitly declared that the “overall story has not changed” since the December FOMC

- The Committee expects a “gradual” and “bumpy” road towards achieving the 2% inflation target “over time”.

- The Fed “didn’t excessively celebrate good inflation’’, and they “are not going to overreact to bad inflation” now.

- The Committee continues to expect that it would be appropriate to cut rates “at some point this year”

- While acknowledging more ‘upside risks’ to inflation projections, Powell also mentioned seeing new labour downside risks as a counterbalance, thereby supporting their easing narrative.

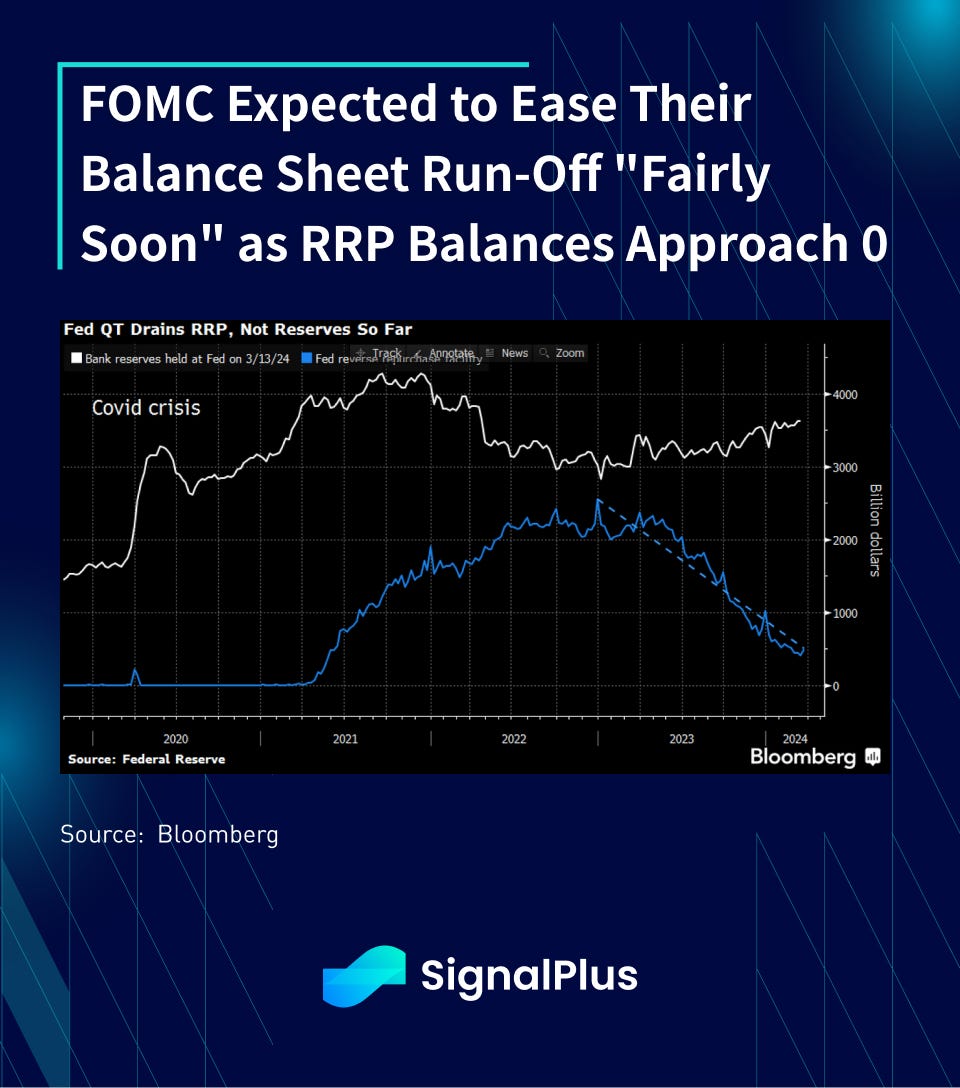

On the issue of the balance sheet run-off, the Fed expectedly discussed slowing the pace “fairly soon”, while trying to caveat the issue by stating that the QT process won’t actually end sooner, but is meant to ensure a smoother transition for funding markets.

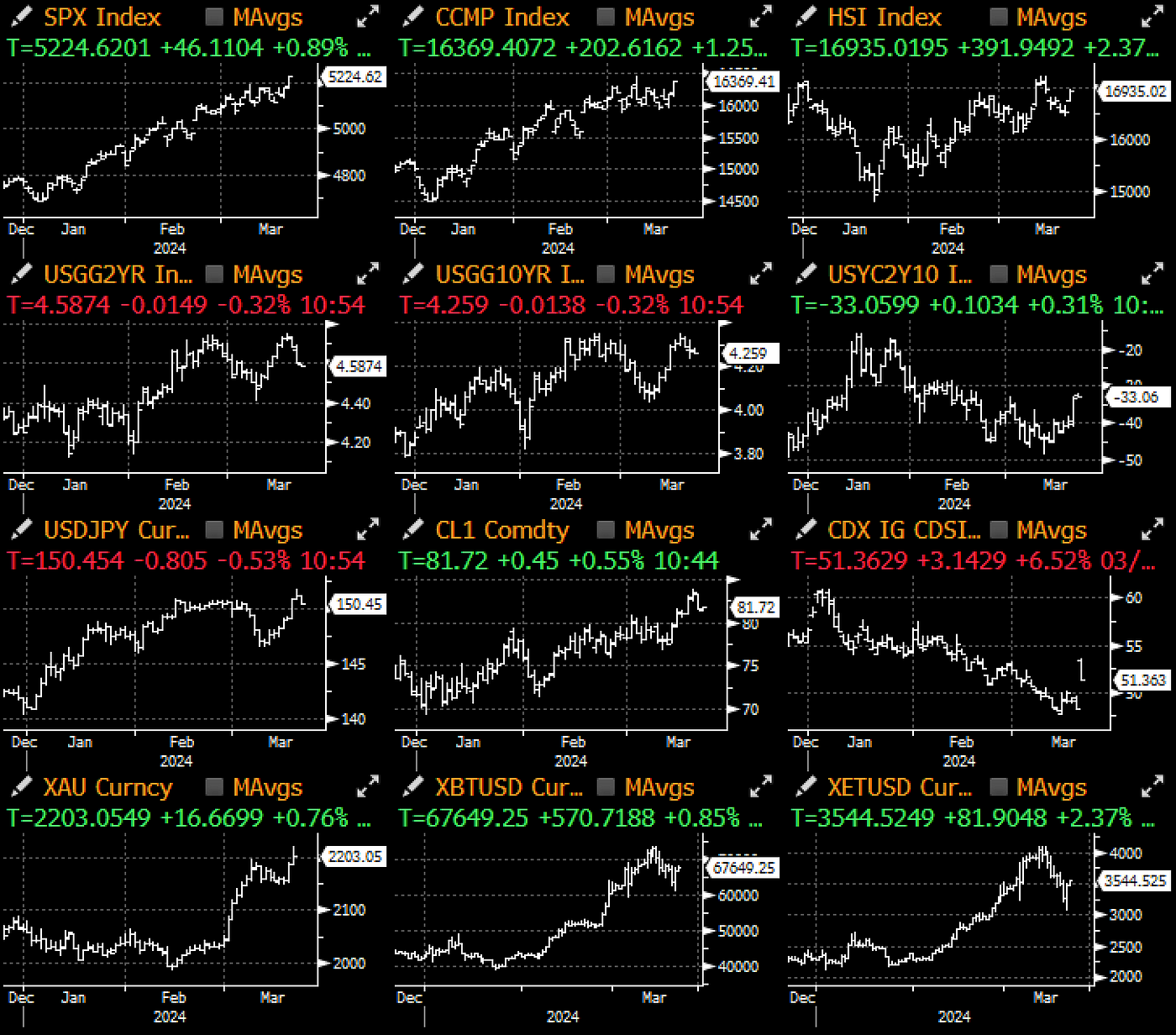

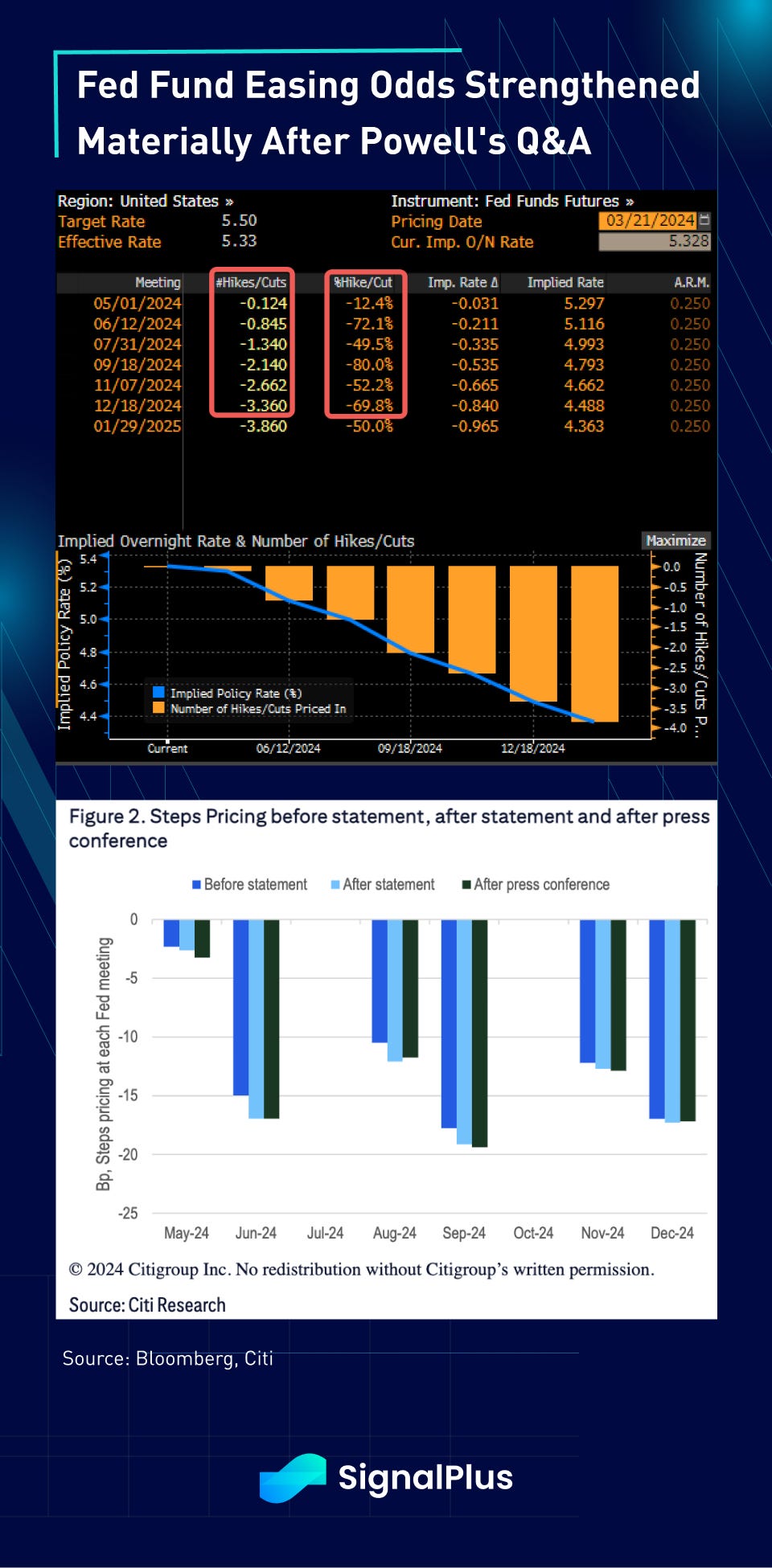

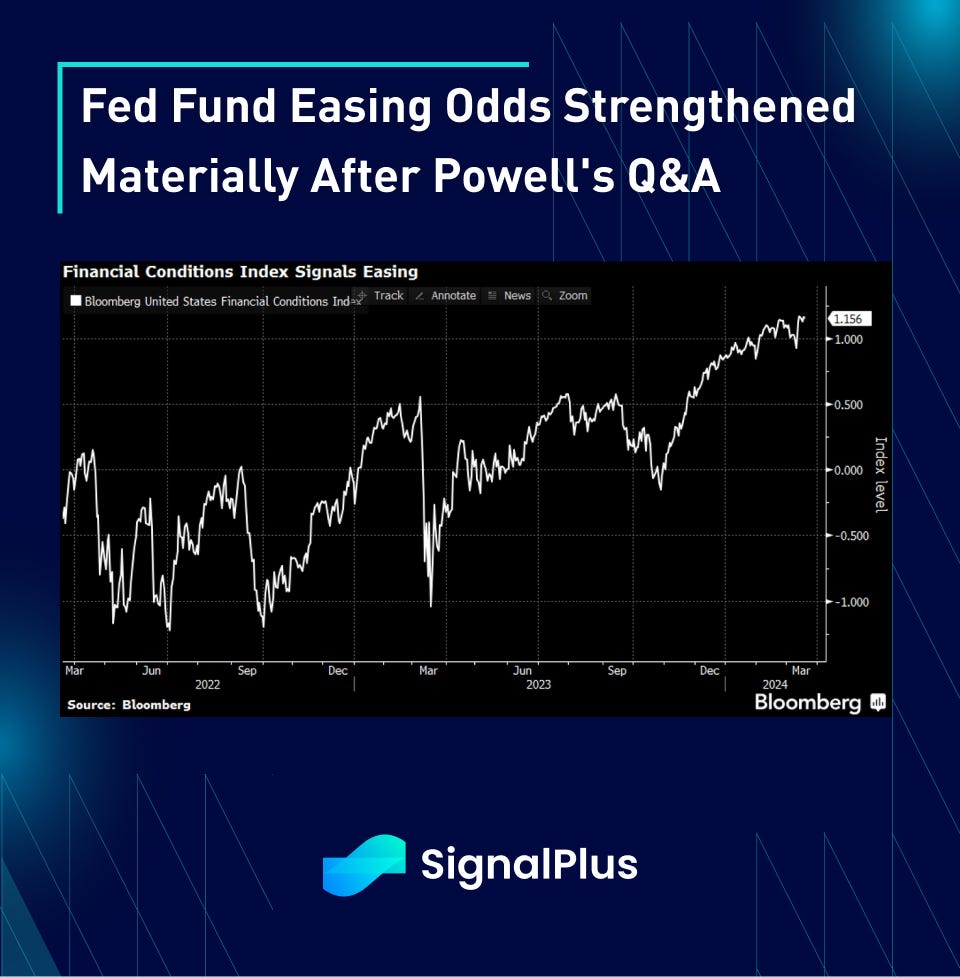

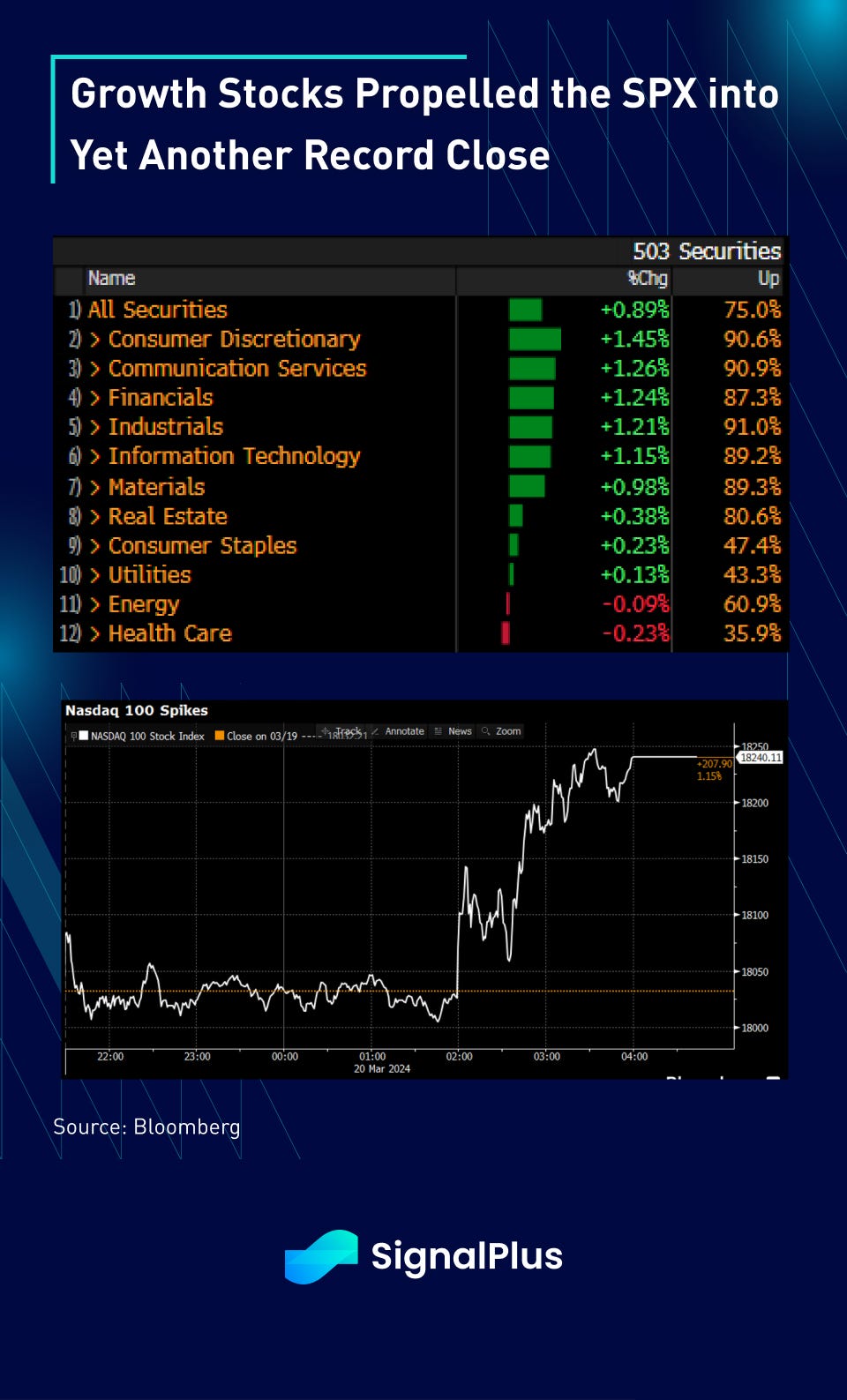

As one would expect, risk markets screamed into and out of the FOMC presser, with treasuries bull steepening (2yr yields -7bp, long end unchanged), US equities adding +1% into yet another record close, June cutting odds back to >70% and nearly 2 cuts fully-baked in by September, and financial conditions eased back to friendly levels over the past 3 years.

With the Fed throwing caution to the wind, the risk party looks to be back on, and the bar for compelling (or embarrasing) the Fed into a hawkish U-turn is now higher than ever. A softer labour market in the upcoming months will be seen as vindication for the Fed’s easing bias, while it will likely take more than a couple more CPI / PCE beats for the markets to dare question whether the Fed has miscalculated on inflation. The fundamental bear case has never been more challenged against the current risk backdrop.

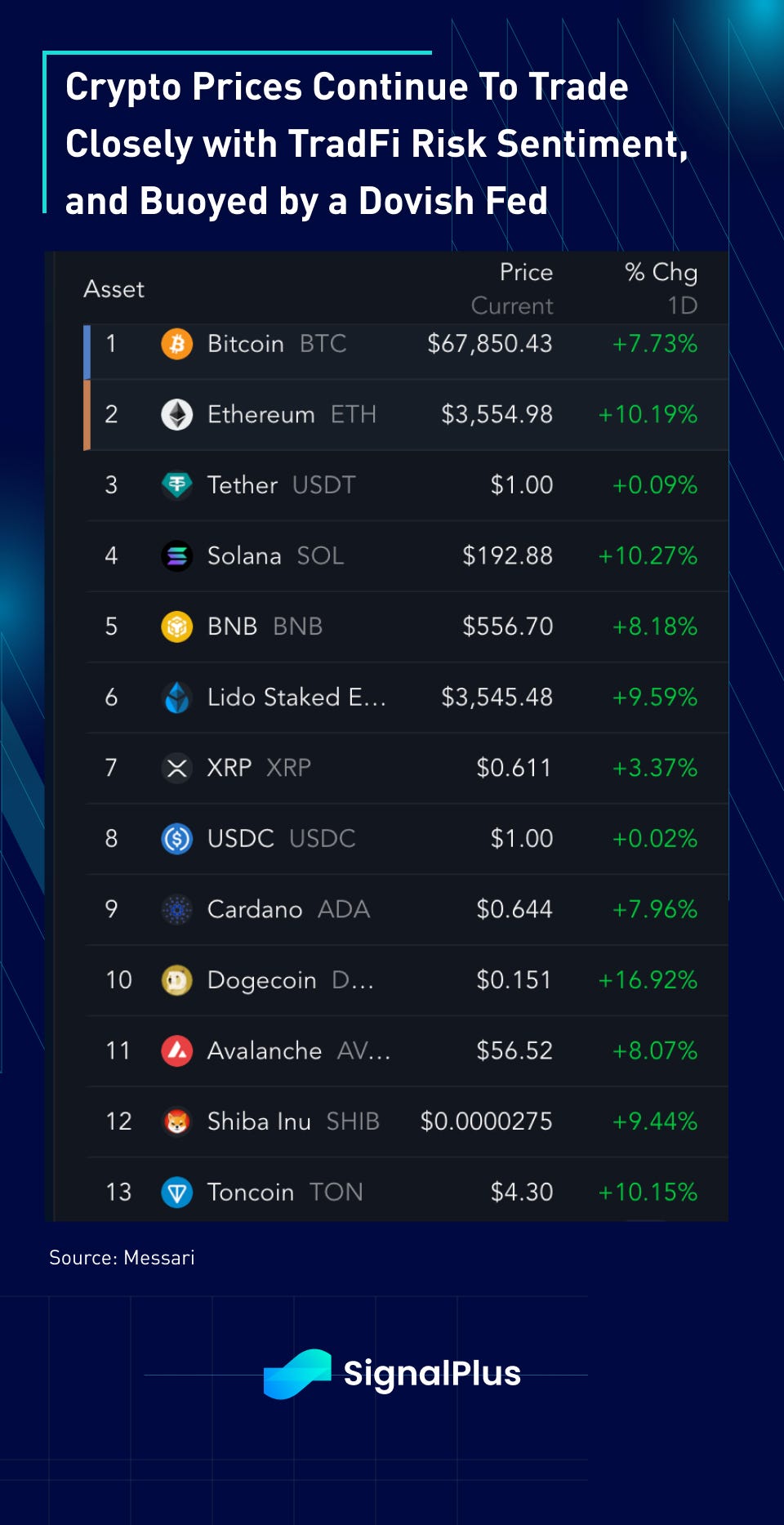

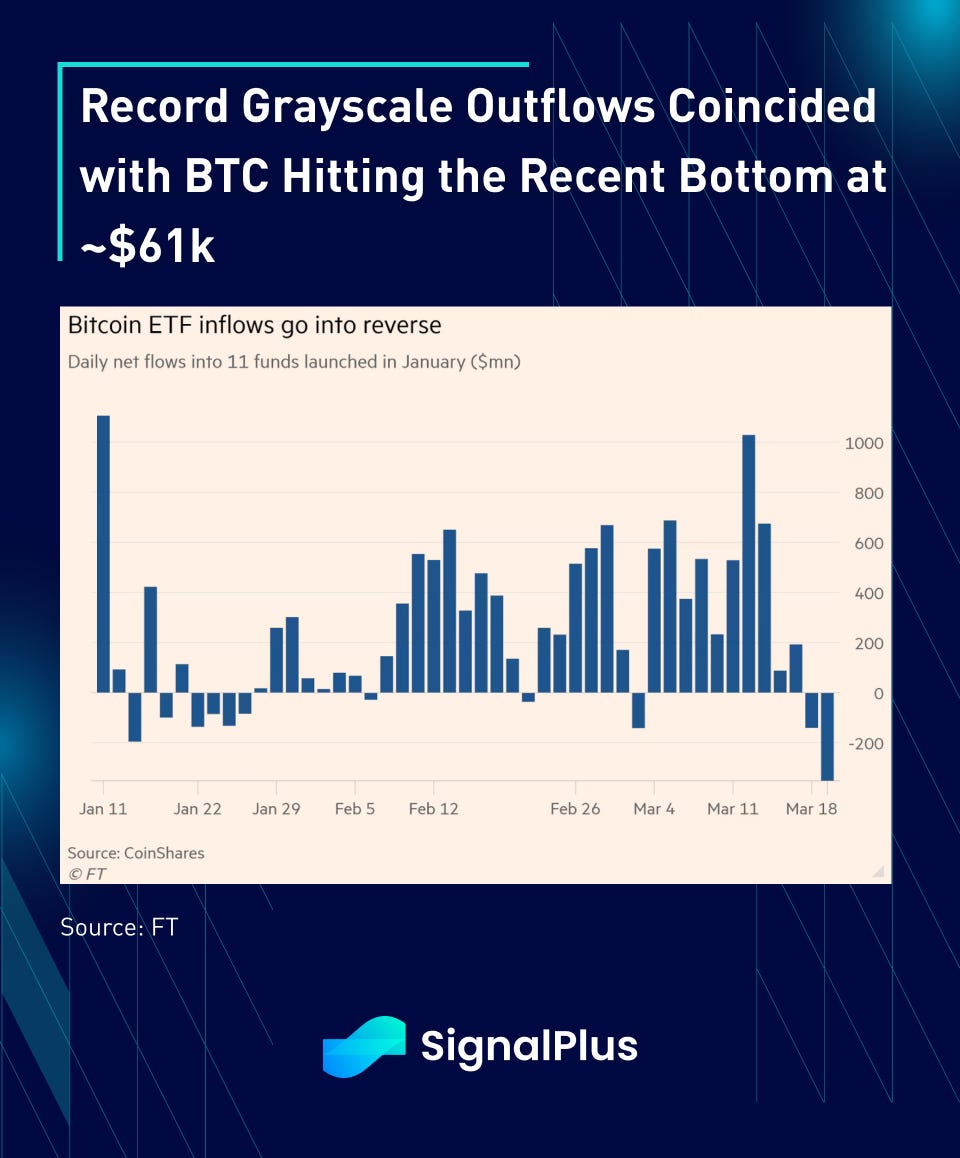

With TradFi sentiment now largely driving crypto, we saw a similar risk-on party with tokens rallying ~10% over the past 24 hours with the rest of the risk complex. Furthermore, the recent drop from $73k → $61k in BTC futures saw considerable long futures liquidation, with positioning now much cleaner than merely a week ago. As such, we also believe that the window for our earlier caution has now expired, and risk-reward should favour rising token prices in the near-term and possibly making new ATHs.

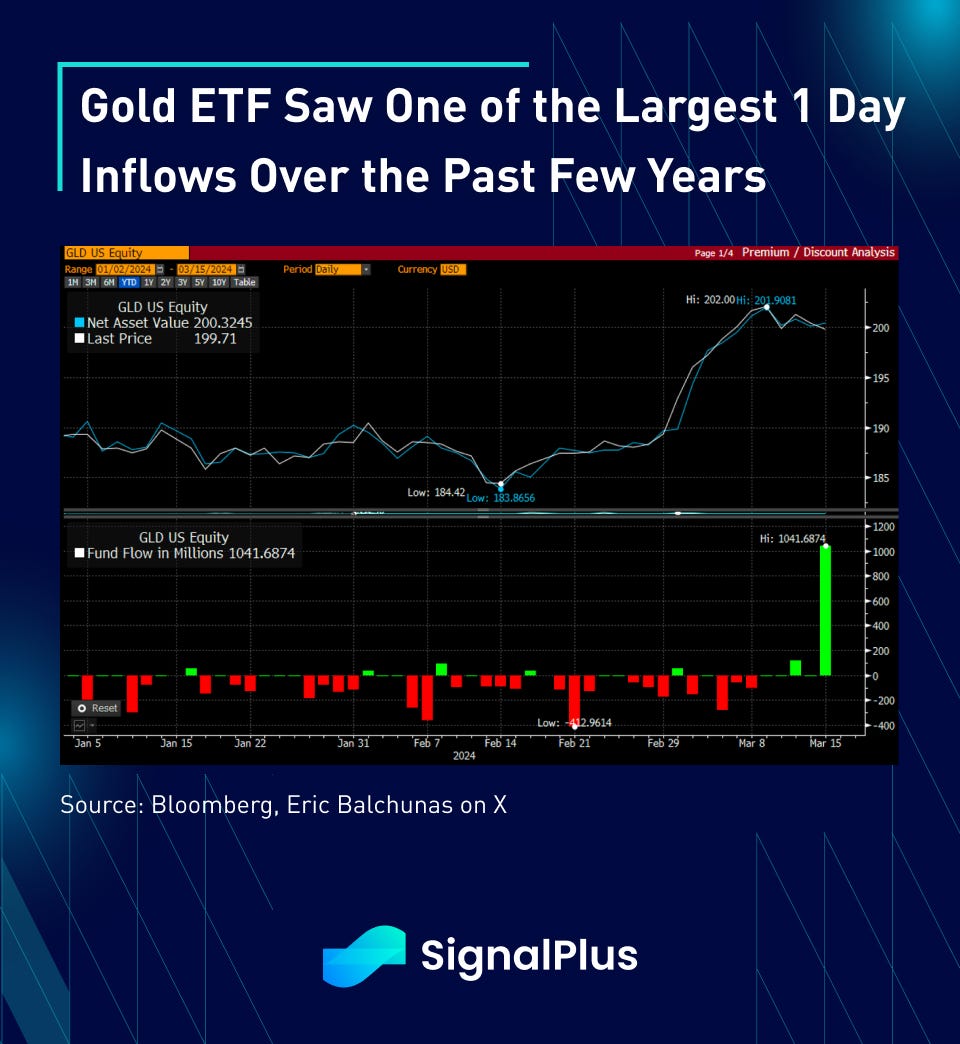

Not to be left behind, the gold ETF also saw one of the largest daily inflows over the past few years as it tries to make up for lost ground on crypto. The latest ‘dovish confirmation’ by the Fed should provide further tailwind for precious metals to rise higher in the near term as well.

Is it time for one of those “STFU and buy everything memes”? Let’s not jinx the party while we are in it.

Finally, in reiterating his comments from the Congressional Testimony weeks ago, Powell continued to downplay the likelihood of any imminent CBDCs. While he admitted that central banks “need to be knowledgeable” about digital currencies, it is however “wrong to say” that the Fed is planning a CBDC, and that Powell himself has not made a decision “at all” regarding the issue. So it’s probably safe to say that our worst-case, ‘Orwellian’ monetary scenario is nowhere close to happening, leaving us to continue building our digital infrastructure in the foreseeable future. Let’s hope it stays this way as long as possible.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments