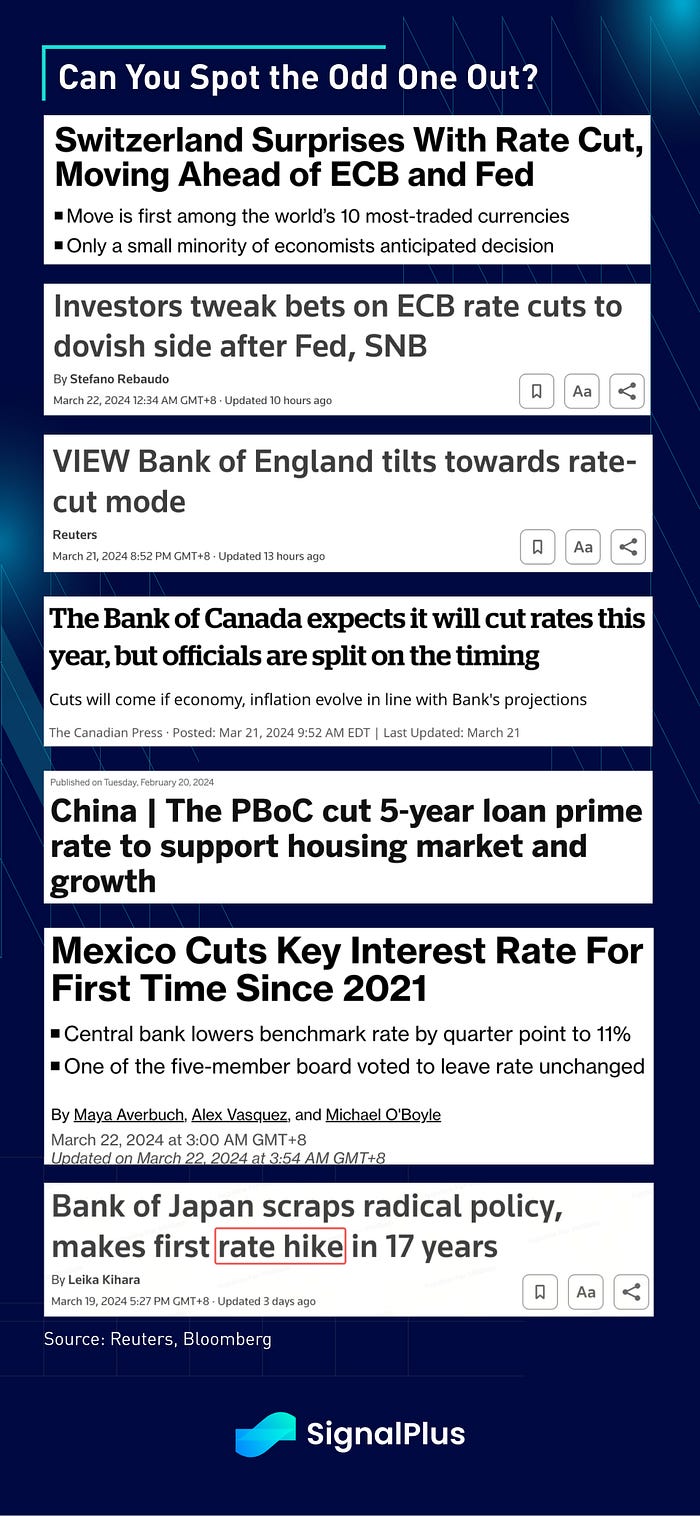

Following the Fed’s dovish surrender yesterday, the SNB surprised the market by being the first major central bank to cut rates, and likely marking the start of a year of rate cuts across developed economies. The Bank of England followed suit with its own ‘dovish hold’ on an 8–1 vote, with the committee expecting CPI to run “marginally weaker” than expected, and the probability of a June BoE cut rising from 65% to 80%. ECB rate cutting odds are also nearly 80% in June following the Fed, BoE, and SNB announcements, while the Bank of Canada and China’s PBoC are also firmly leaning towards the accommodative stance given lacklustre growth.

On the other hand, Japan remains an irregularity and continues to dance to its own beat with the only central bank to be hiking in the current cycle, with their stock market, real estate market and wage gains outperforming most of its peer group. Interestingly, while FDI and foreign inflows have been a major tailwind over the past 18 months, foreigners sold substantial equity exposure in December over concerns about the BoJ’s NIRP exit. However, and somewhat surprisingly, the TOPIX/Nikkei barely budged and have continued to forge new highs into and out of the BoJ hike. A similar pattern happened in September, where foreign outflows accelerated at the first signs of a policy change, only to pull a 180-reversal in October when things turned out to be a non-event. Will a similar pattern happen in the near future?

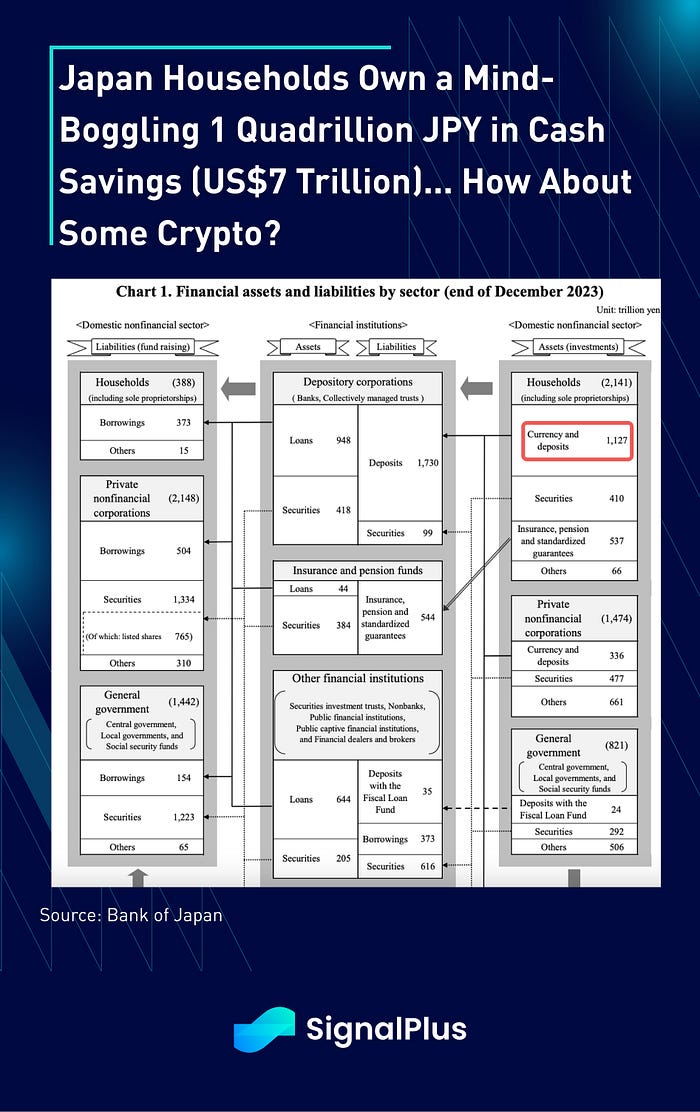

Furthermore, the BoJ’s latest monetary survey also showed a slew of interesting tidbts. Japan households hold a staggering 1 quadrillion JPY (~US$7 trillion) in cash and savings accounts, making up ~53% of household financial assets and substantially higher than the US (13%) and Europe (36%). Furthermore, the median household saw their equity investment values rise by ~30% YoY, and 1/10 households made over 6 million JPY in capital gains, equivalent to a full year of household income. With attitudes finally changing towards stock investments (Buffet effect), real estate purchases (foreign buying), wage inflation (largest union wage gains in 33 years), the NIRP exit, and an ongoing generation wealth transfer from the old to the young, what they will do with their excess US$7T in cash savings shall be one of the biggest macro stories in the years ahead. Can we interest them in some crypto diversification perhaps?

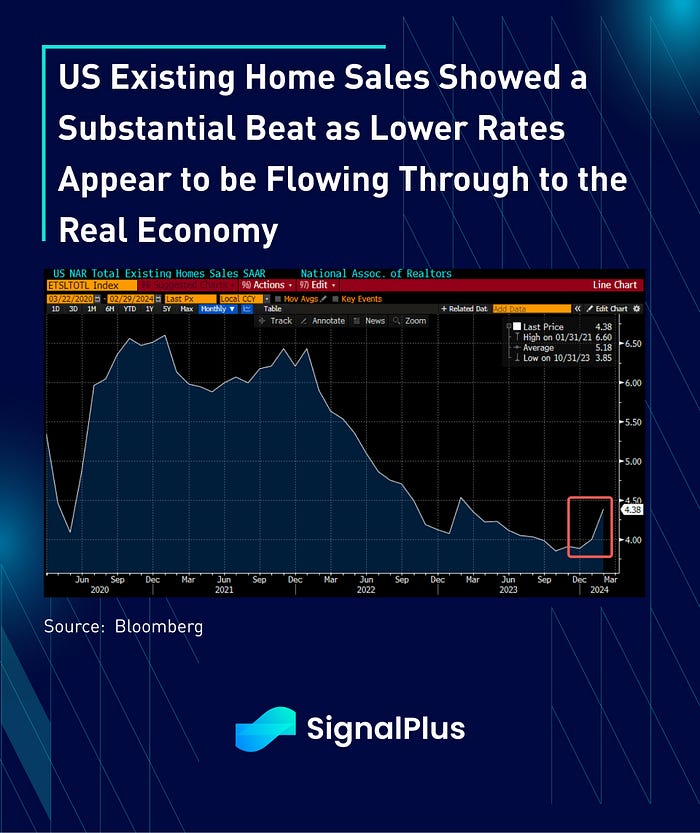

Back in the US, it was pretty much more of the same with equities levitating to new highs (thanks Fed!), with data showing existing home sales making a substantial beat as lower mortgage rates appear to be flowing well into the real economy now. Along with the headline beat, housing supply and the median price transaction (+0.5% MoM) are also showing healthy gains back to pre-pandemic levels, and further rate cuts from the Fed should only help to bolster demand even further in the 2H of the year.

In equities, the S&P 500 rose for a 4th consecutive to yet another new record high, with indices rising despite a -4% tumble in Apple shares as the DoJ sued the iPhone giant on violating antitrust laws. On the other hand, Reddit priced their long-awaited IPO which soared as much as +67% higher than its offering price, before ultimately settling ~48% higher as investors clamored to the company’s vision of providing a trove of training data for the proliferation of AI learning models around the world. The IPO’s success will likely open the door to a full line-up of private companies looking to tap a public market exit with sentiment running rampant.

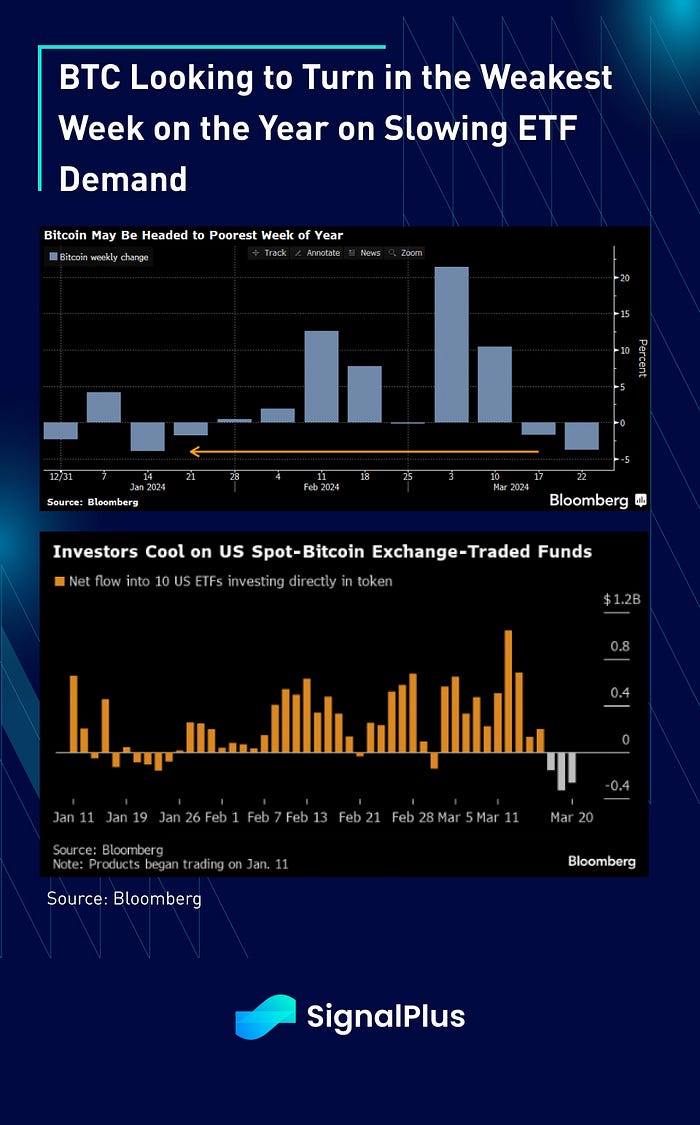

Finally, in crypto, the tone has turned more dour as Bitcoin is on track to turn in the poorest weekly performance of the year on slowing ETF demand. After hitting a string of daily record inflows topping over $1bln in the middle of March, net flows have turned decidedly negative over the last 3–4 years, coinciding with a slow down in price momentum as BTC is barely managing to hold above the $65k area despite the prevalent risk-on sentiment across nearly all other asset classes.

Furthermore, the SEC has likely returned to its old ways, as Forbes reported that the Ethereum Foundation is facing confidential questions from an unnamed “state authority” according to the group’s GitHub repository. Specifically, developers stated that “[t]his commit removes a section of the footer as we have received a voluntary enquiry from a state authority that included a requirement for confidentiality”, and the removal of a text that stated that the Foundation has never been contacted by any agency in the world under confidentiality.

This confidential inquiry is coming during a tricky time, with signs suggesting that the ETH ETF might not gain SEC approvals in May, as the agency remains adamant that ETH remains a security. ETH prices have dipped along with the Grayscale Trust’s ETH discount widening from -10 to -18%.

In any stretch, it does appear that the near-term euphoria has subsided a bit from the crypto space, and we might finally see a few days of sideway actions as the market rebuilds its footing.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments