After 3 months of consecutive upward surprises, a roughly in-line CPI was all that was needed to spur risk markets to another blow-off record rally. The EoD scorecard looks something like the following:

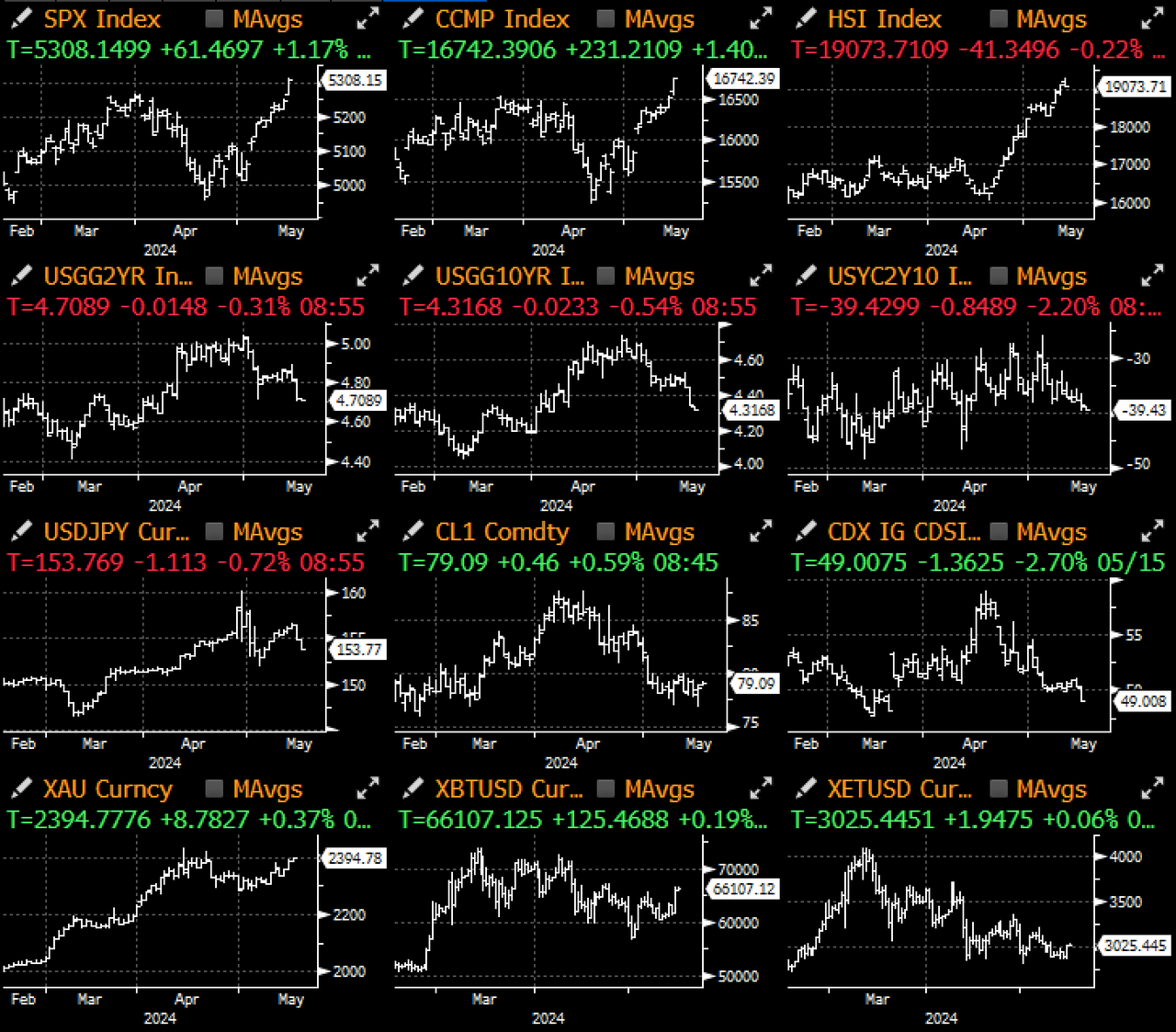

- Yet another new record high for the SPX

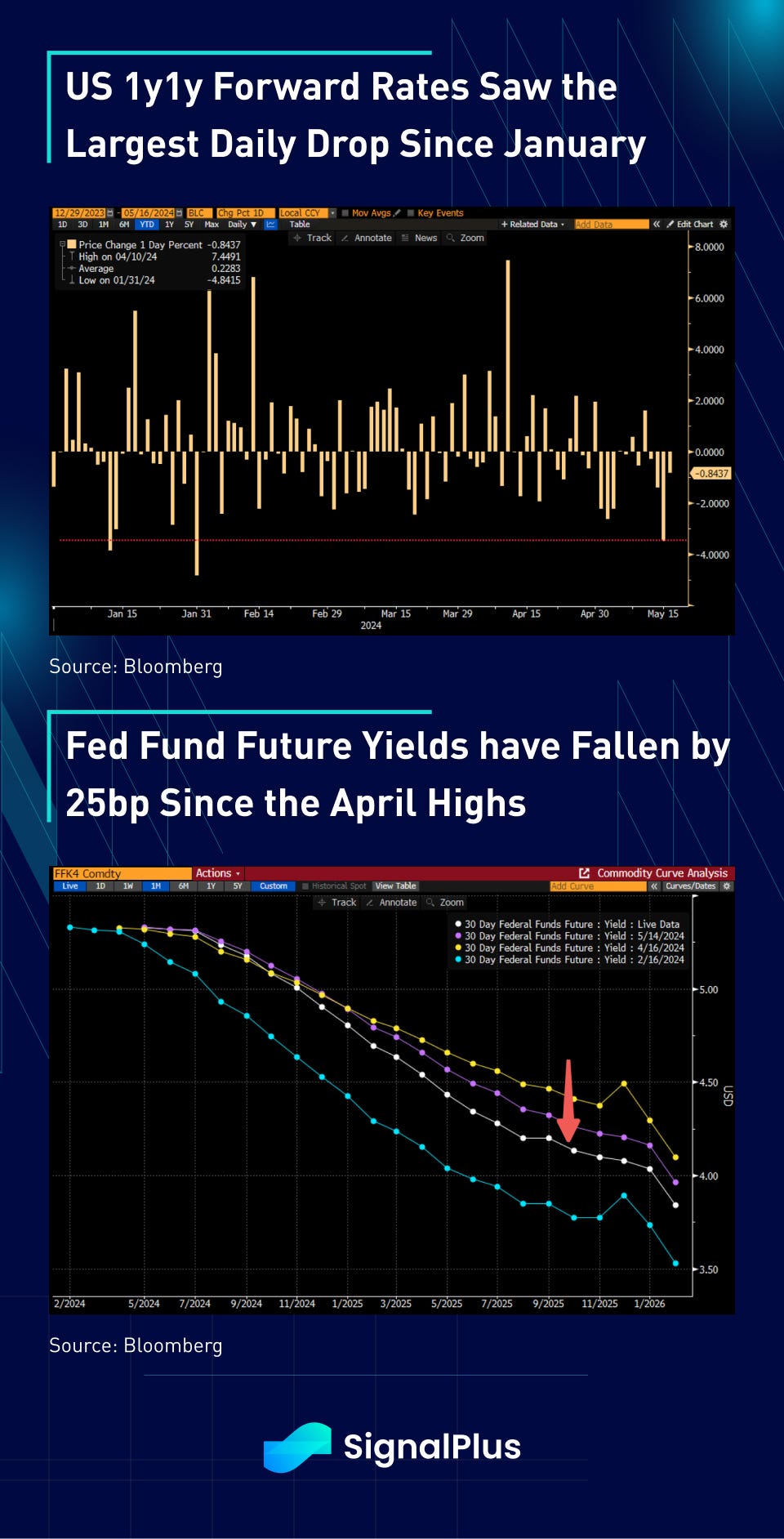

- Largest daily drop in US 1y1y forward rates since early January

- 2025 Fed Fund futures yields falling by 25bp (a full rate cut) since the April highs

- USD DXY saw the largest single day drop YTD

- Cross-asset volatility (FX, Equities, Rates) falling back to their interim and/or record lows

So is the Fed about to cut rates ASAP? June Fed Fund futures are pointing to merely a 5% chance for a rate cut and July at just 30%; even September odds are not much better than a toss-up at ~64%. So what was all the excitement about?

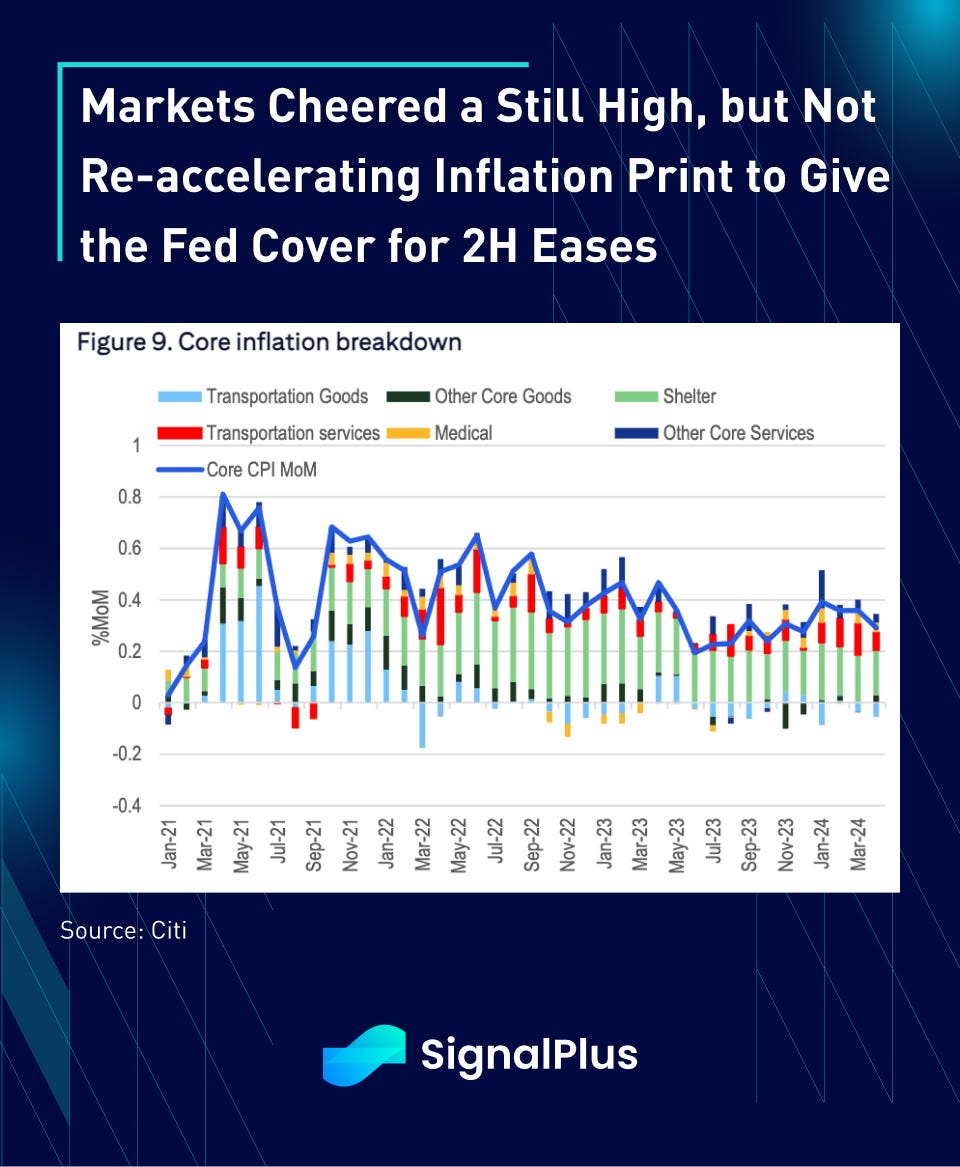

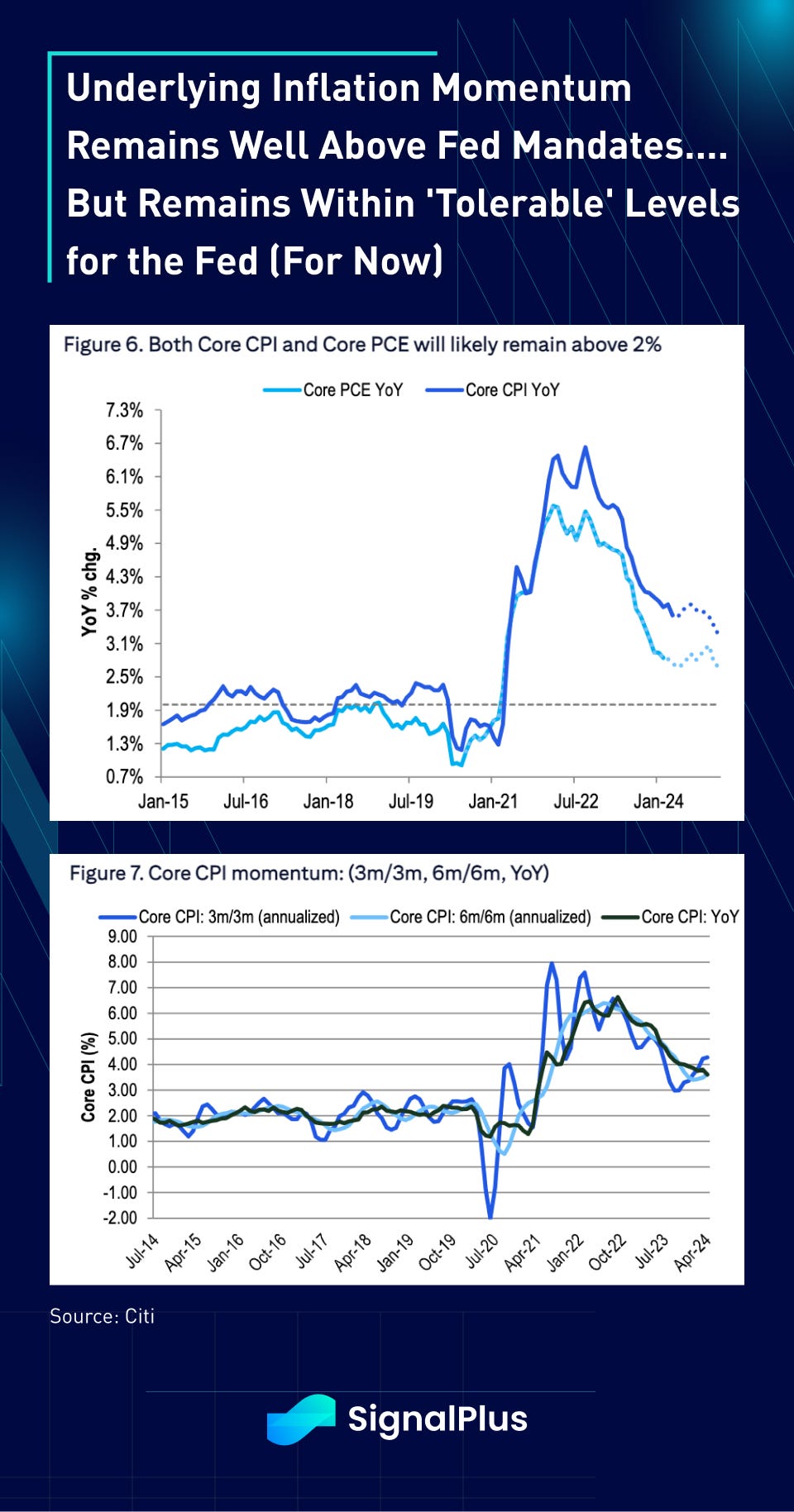

As we have been alluding to since the past FOMC, the Fed has shifted to a full asymmetric bias where sustained inflation pressures would be tolerated, as long as they are not reaccelerating, but any emerging weaknesses in labour markets would be taken as a policy easing impetus. As such, while headline and core inflation remain well above Fed mandates at 3.6% and 3.4%, respectively, the market’s fear was for a pricing reacceleration, which failed to materialize in the past month. That plays into the overriding theme that the Fed is back on ‘easing watch’, as the bingo card of ‘slowing job markets’ and ‘high but still-tolerable inflation’ are being checked off.

The actual CPI data showed core rising 0.29% MoM in April, basically just a hair beneath consensus after 3 months of consecutive upside misses. The softness was attributable to a drop in goods prices and manageable increases in shelter prices and OER. Core services excluding housing rose 0.42% MoM, roughly in line with estimates.

Post CPI/PPI, Wall Street expects core PCE to come in at around 0.24% MoM in April, thereby heading towards a 2% annualized level and towards the Fed’s comfort zone. Traders remain confident that inflation prices will continue to settle back lower in the 2H of the year.

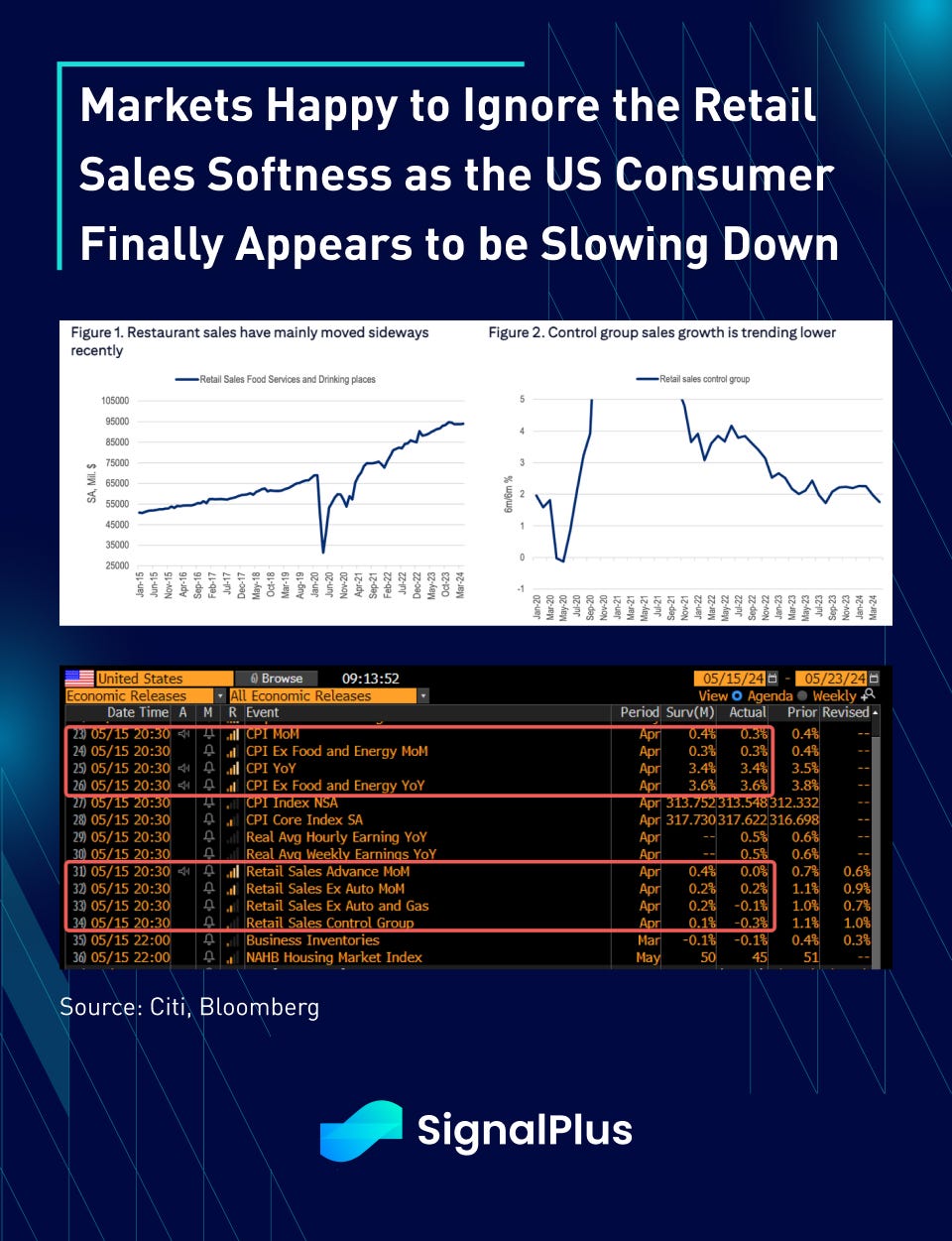

Lost in the CPI relief was a much weaker April retail sales report, which saw widespread weakness across various discretionary spending categories. Headline spending came in at flat versus consensus expectation of a 0.4% — 0.5% MoM rise, with the control group spending falling by 0.3% MoM with negative prior revisions. Drops in general merchandise and even non-store sales saw some of the largest declines since 1Q23.

The retail sales miss continues a string of recently softer consumer data over rising credit card and auto loans delinquency, exhaustion of accumulated excess savings, and deteriorating perceptions of labour market strength. While we are still entirely too early to call for a harder economic slowdown, it does feel like we are close to an inflection point for economic growth as high rates might finally be biting into the US economy?

As usual, markets are comfortable ignoring any slowdown risks and focusing on the first Fed easing function for now. As a reminder, public markets are supremely adept at pricing-in all available information and being forward looking — just not that forward looking, mind you. Enjoy the brief party while it lasts and try not to get in the way.

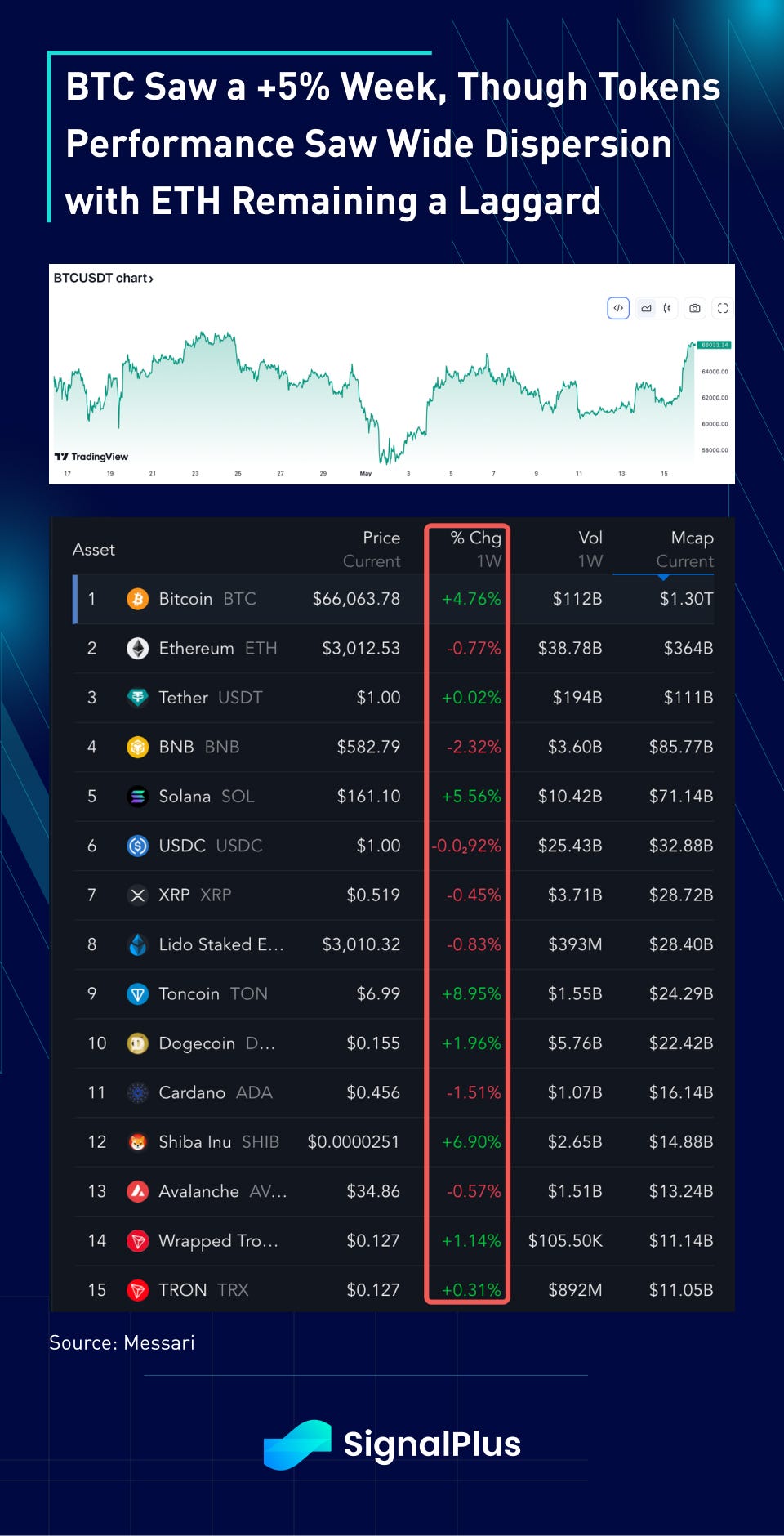

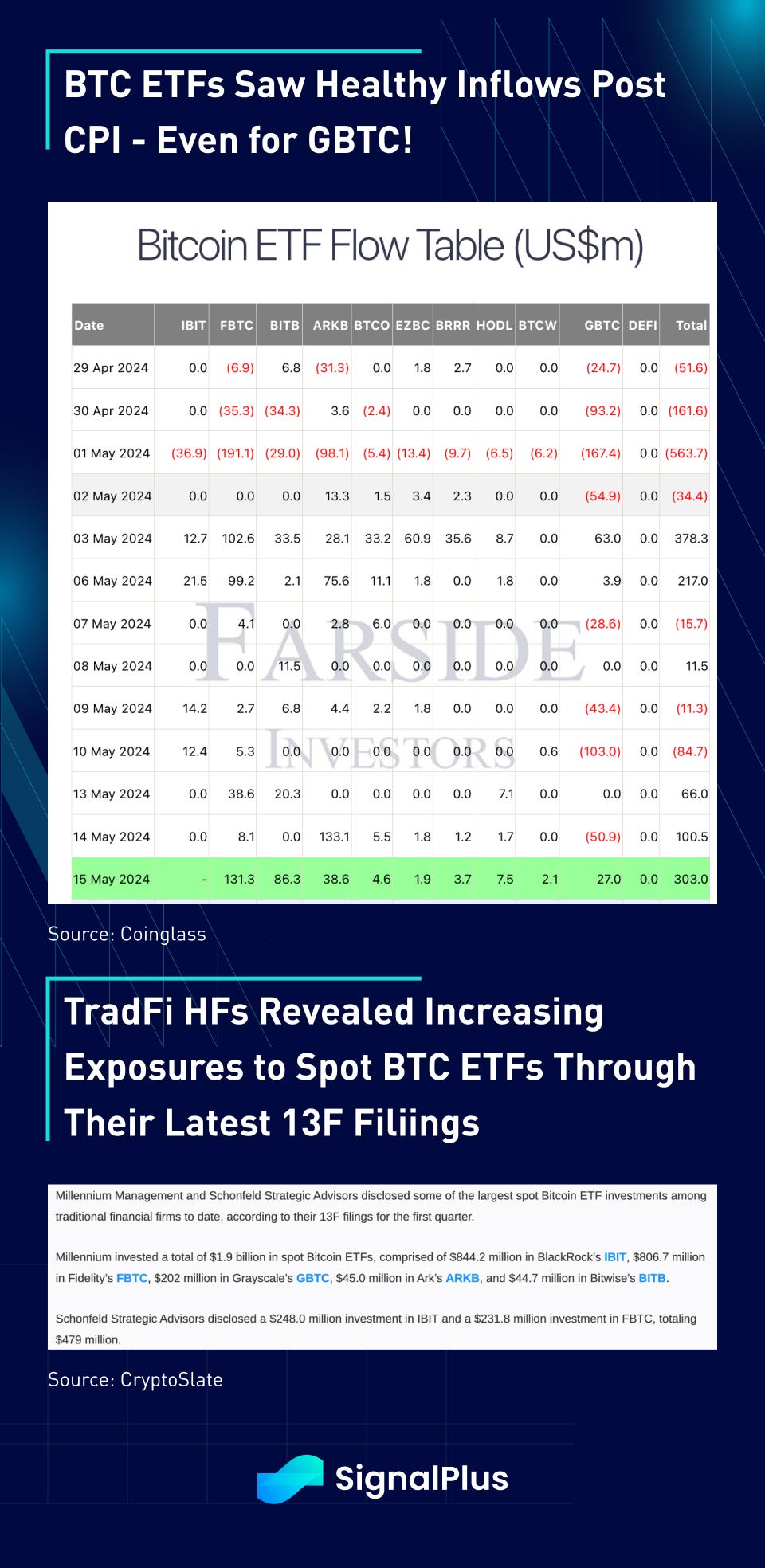

In crypto, BTC prices continued to be led by the flow and ebb of overall equity sentiment, with prices breaking its MTD highs and recovering back to the April peaks at around $67k. ETF inflows were also healthy, with a new +300M reported yesterday post CPI, with even GBTC showing a net inflow. However, underneath the surface, performance dispersion remains high across tokens, with ETH and a number of Top-20 assets struggling to make up any lost ground over the past week. Performance remains increasingly concentrated in a small pocket of winners (BTC, SOL, TON, DOGE), without any significant beta spillover.

We expect this to continue and remain focused on BTC as the main benefactor of continued TradFi inflows (13F filings showed increasing BTC ETF exposures from some large HF titans), and expect less wide-spread FOMO into natives-only or degen coins over this current cycle. Good luck friends!

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments