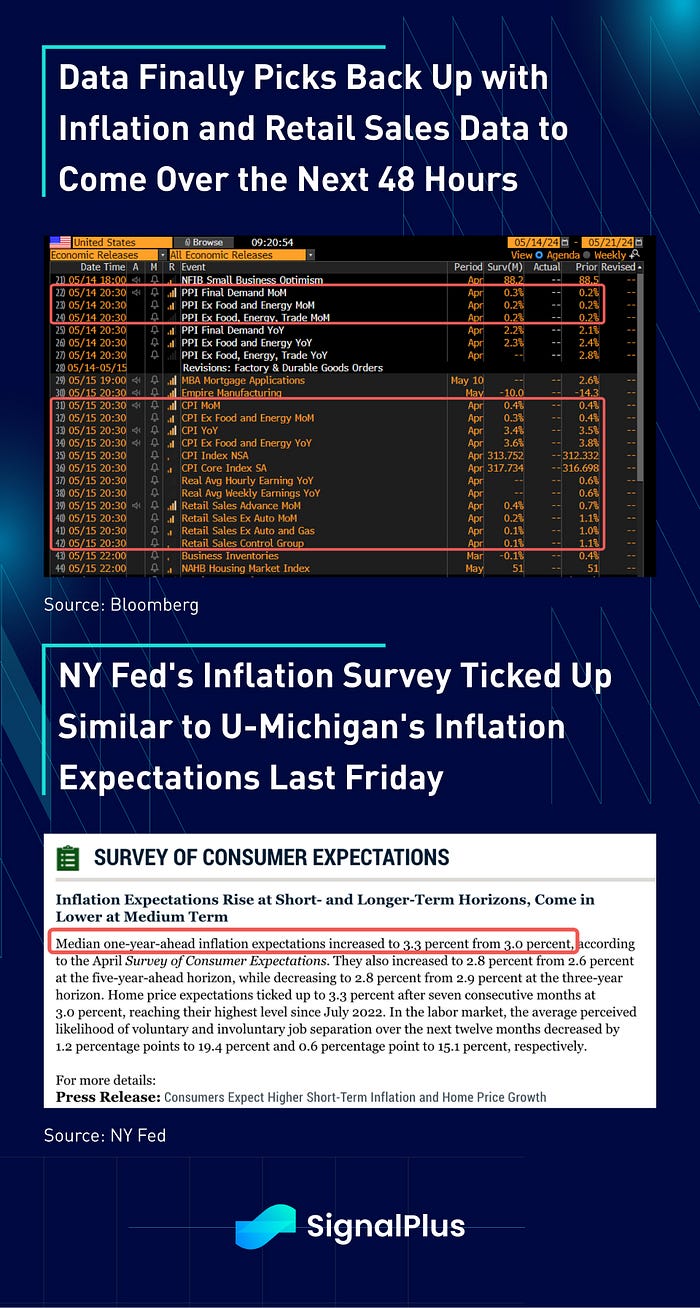

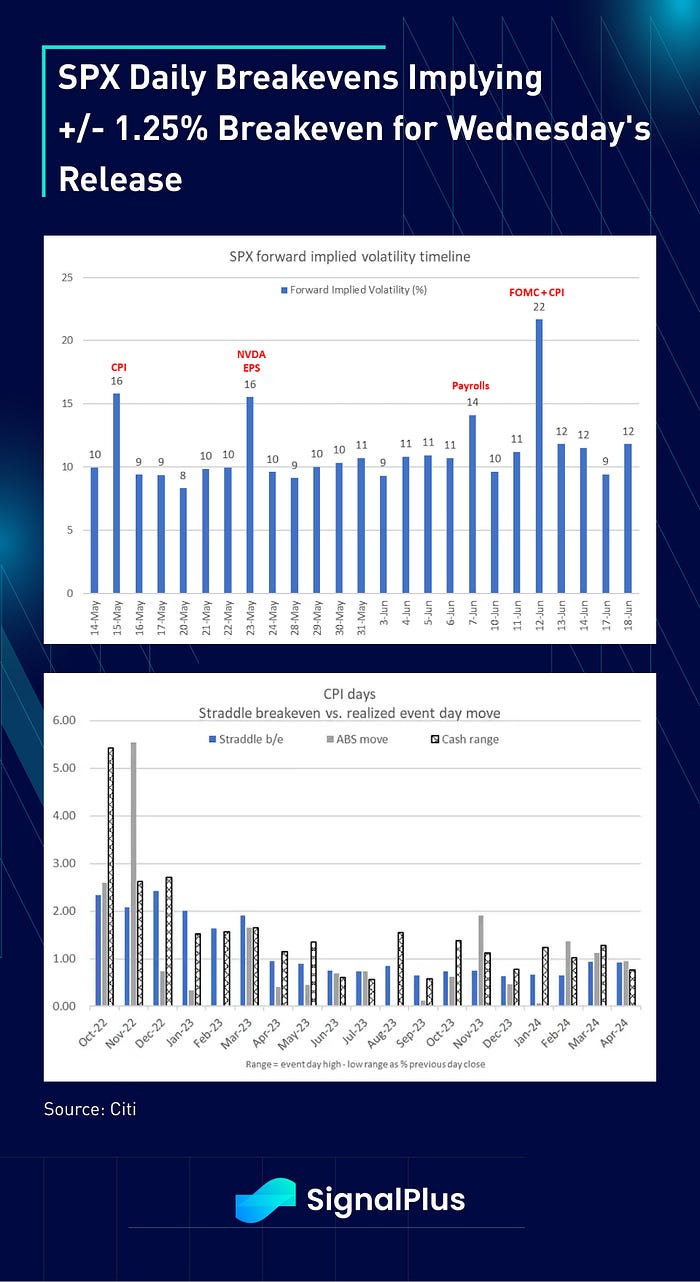

A quiet Monday to start the week with a slew of market moving data to arrive over the next few days. PPI will kick things off on Tuesday followed by a prime double-header of CPI and retail sales on Wednesday, with no shortage of sell-side analysts predicting the 3rd-decimal place outcome of where the index value is going to come in at. In the meantime, following the rise in U-Mich inflation expectations last Friday, the NY Fed’s survey of consumer expectations also saw a rebound in 1-yr ahead expectations to 3.3% (vs 3.0% prior), the first significant rebound in over a year.

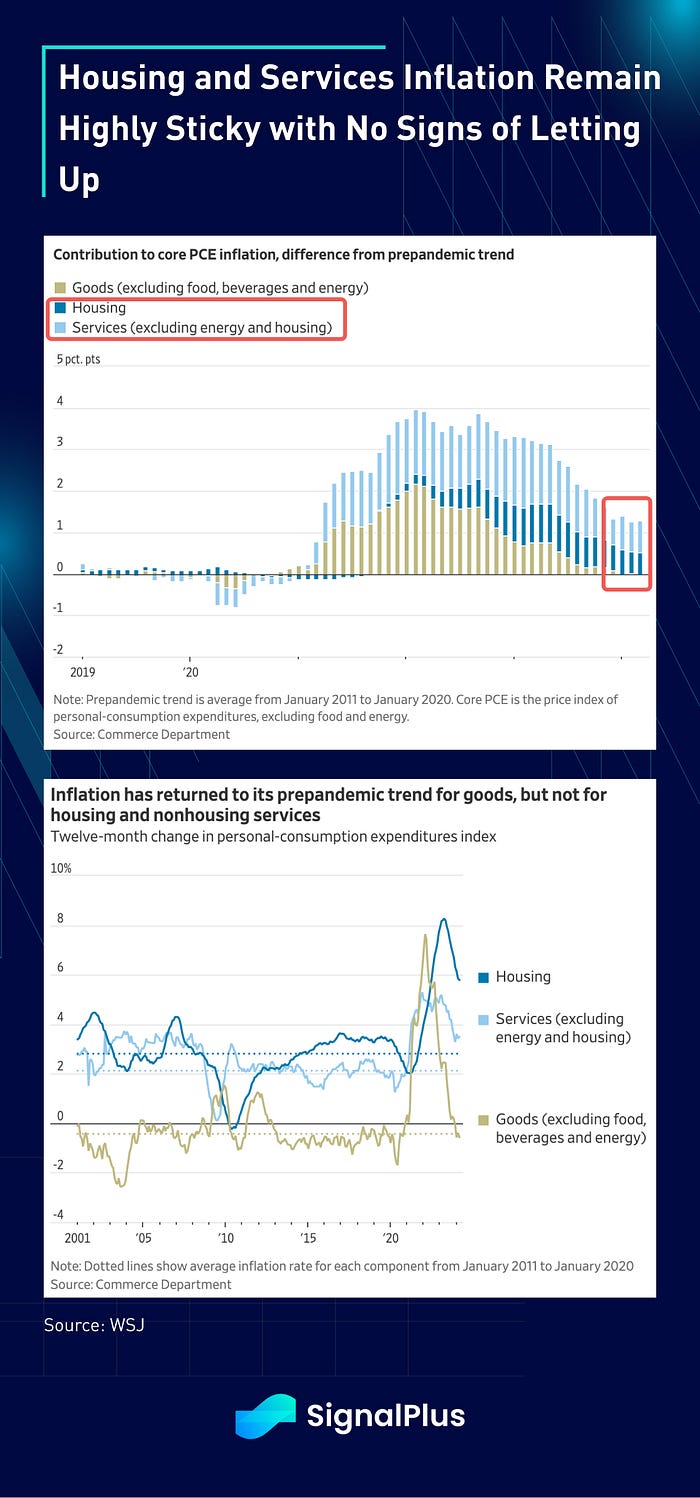

Without going into the nuanced details of CPI, what is clear this cycle is that housing and services inflation remain fully entrenched versus history. Anecdotal stories of housing supply shortages, rising raw materials input construction cost, and stubborn rent pricing (any one of you had your rents ‘deflated’ lately?) appear to be a permanent fixture of our times, just as QE / easy money was over the prior decades. Such is likely to put a floor on the nominal rate of inflation to come out of the report, but expect markets to ‘over-analyze’ any nuanced details or misses to the downside given the Fed’s asymmetric mandate of ‘justifying’ a dovish narrative.

According to Citi calculations, the SPX has moved an average of +/-1.3% over the past 24 CPI days, with about 40% of the trading days realizing below the 1-day straddle breakeven, and 60% above. Current straddle pricing is similar to March at around 1.25% daily breakeven, which remains towards the higher end of the recent range, but is reasonable given the double CPI + retail sales release on the same day. Strap your seatbelts on!

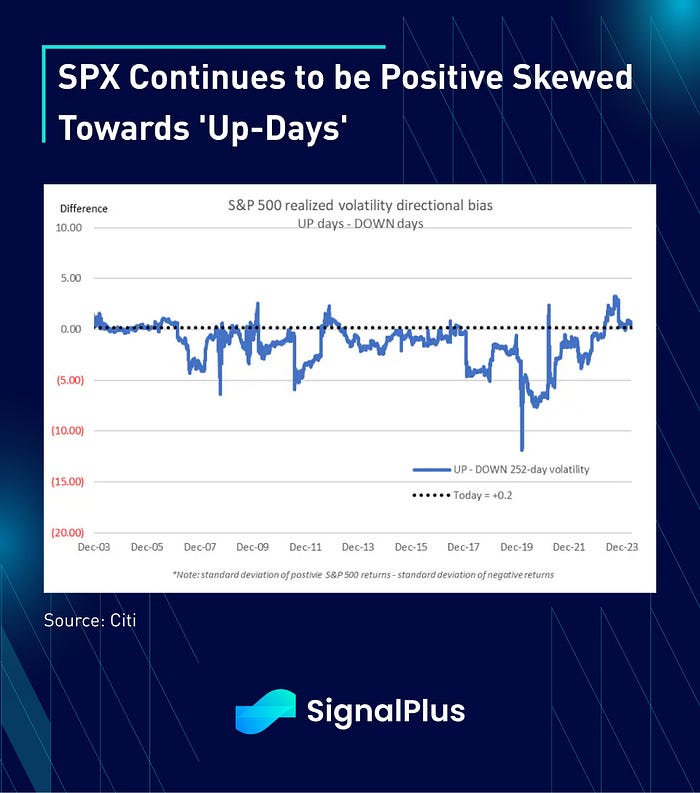

Outside of CPI, underlying vol metrics remain constructive for equities. VIX and it’s 2nd order VVIX cousin remains in a historically low percentile with convexity still favoring the upside. Said in another way, the SPX is continuing to realize stronger returns on up-days vs its down days, and the index has not since a -2% daily drawdown since mid February. The recent monthly and quarterly ranges are also amongst the lowest levels in almost 40 years with low implied correlation. In a nutshell, the goldilocks narrative remains well and alive, with the market pricing in 2nd-order or even 3rd-order policy adjustments from the Fed from the smallest changes in macro developments.

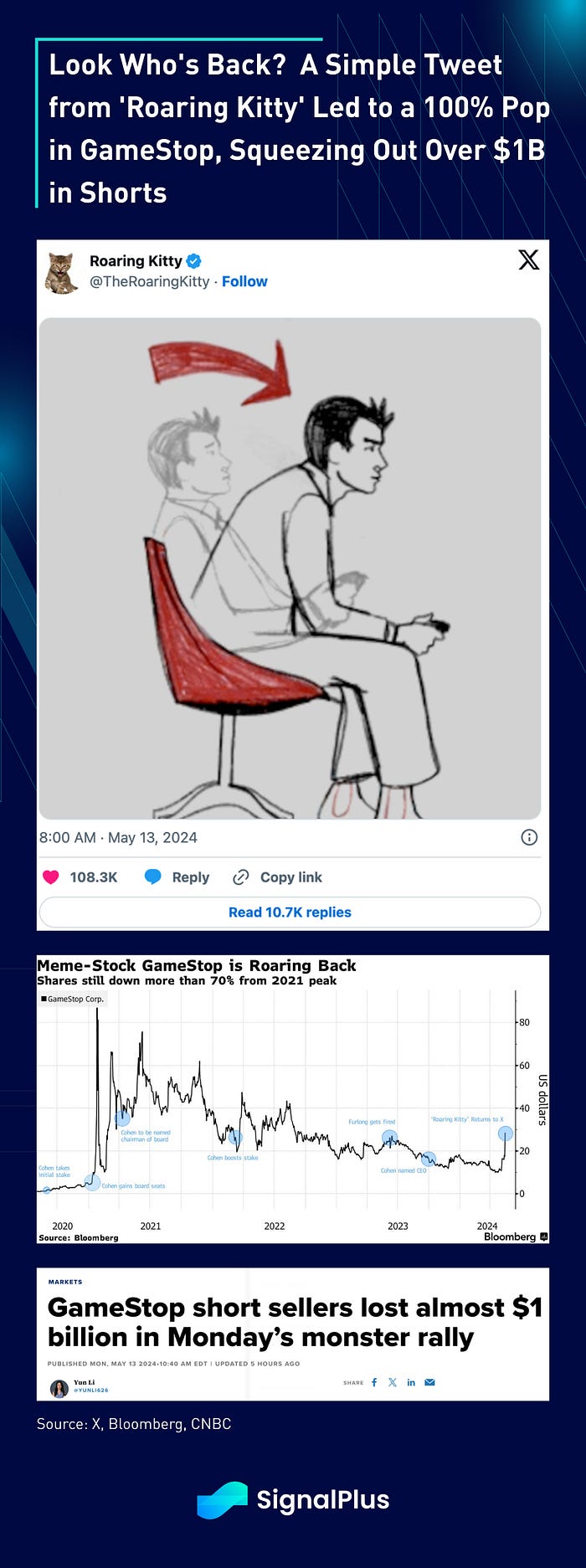

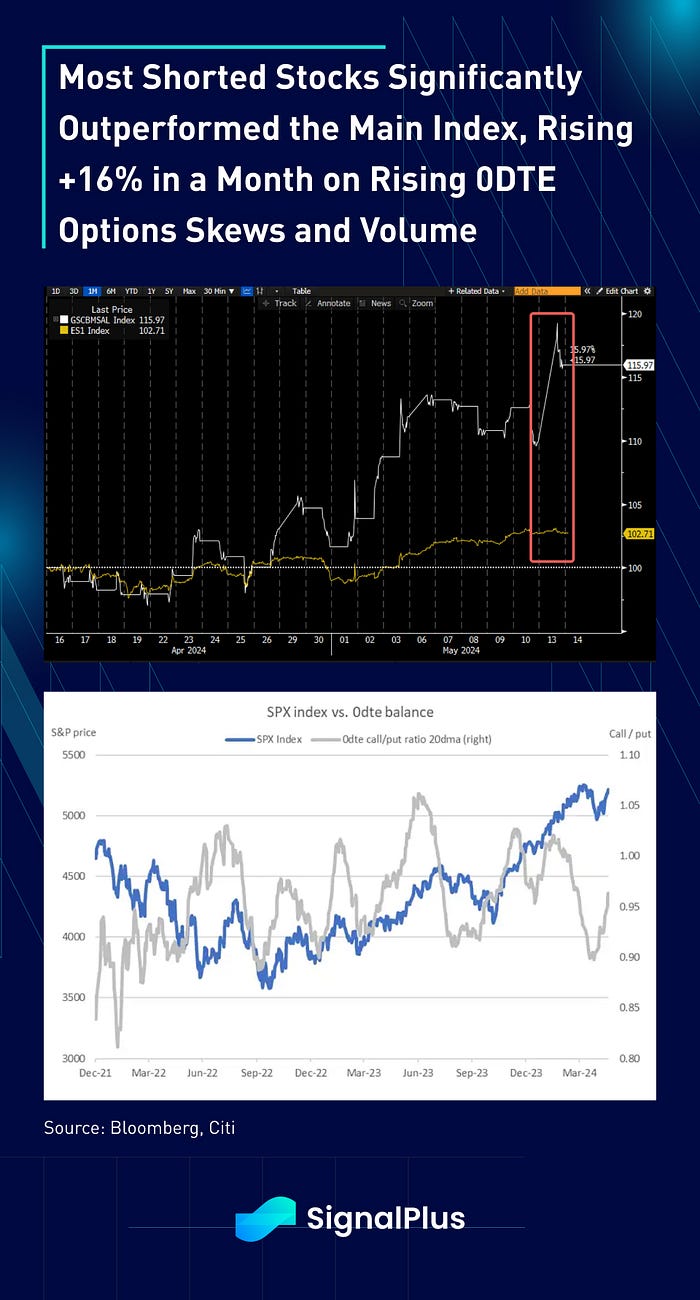

While crypto frenzy has died down recently, a famed TradFi meme-stock OG (Roaring Kitty) made his triumphant return on Twitter (X) yesterday with a simple meme with no accompanying message. Hysterically, his presence was enough to spur Gamestop to spike over 100% in prices yesterday, causing short-sellers (professionals?) to lose over $1bln yesterday, reminiscent of the go-go days during the covid lockdown. Over the past month, the SPX has been up a ‘mere’ 2% while the most-shorted stock basket has rallied nearly 16%, with 0DTE call-put ratio rising above 1 and on strong volumes. Look who’s laughing now?

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments