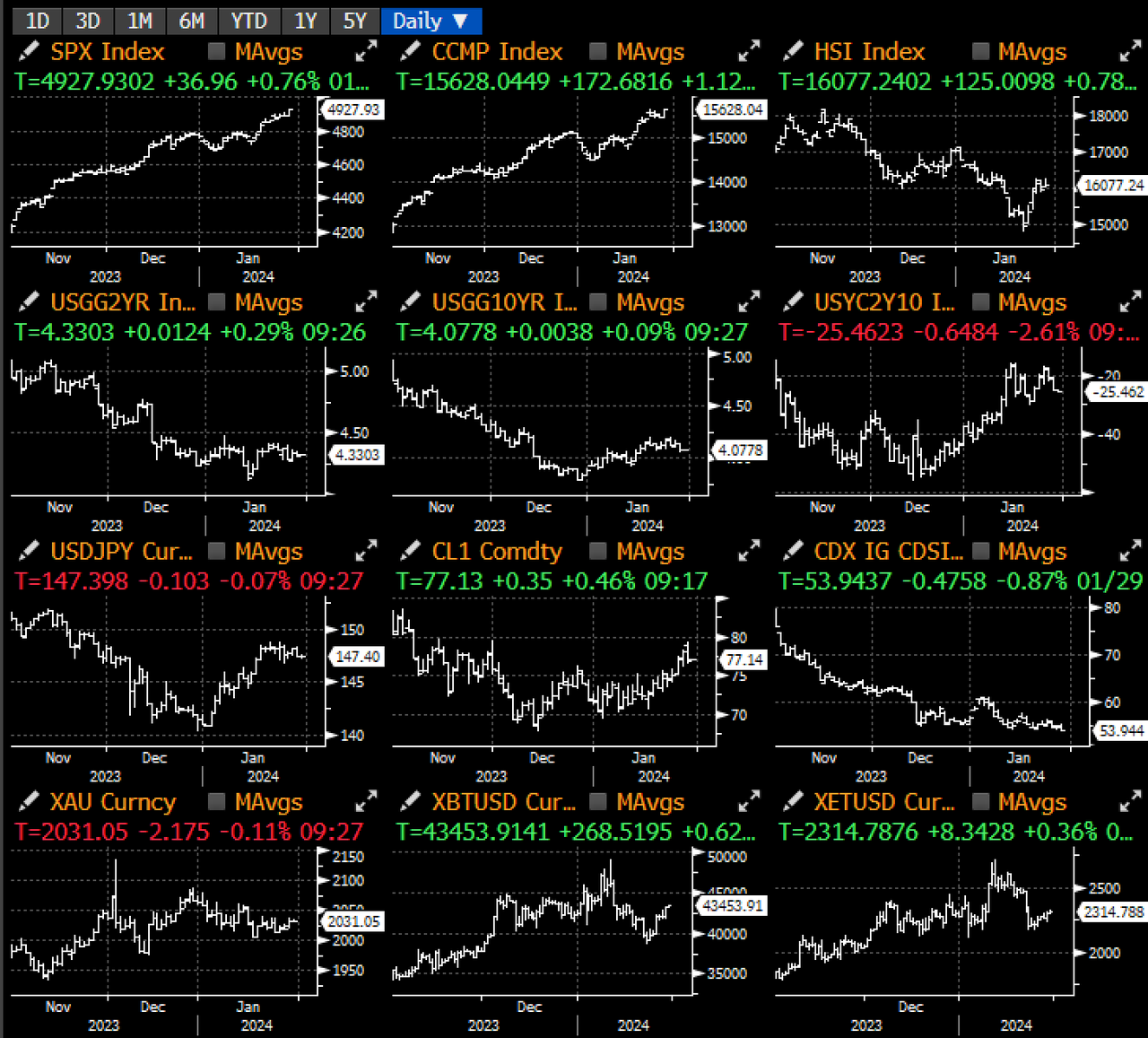

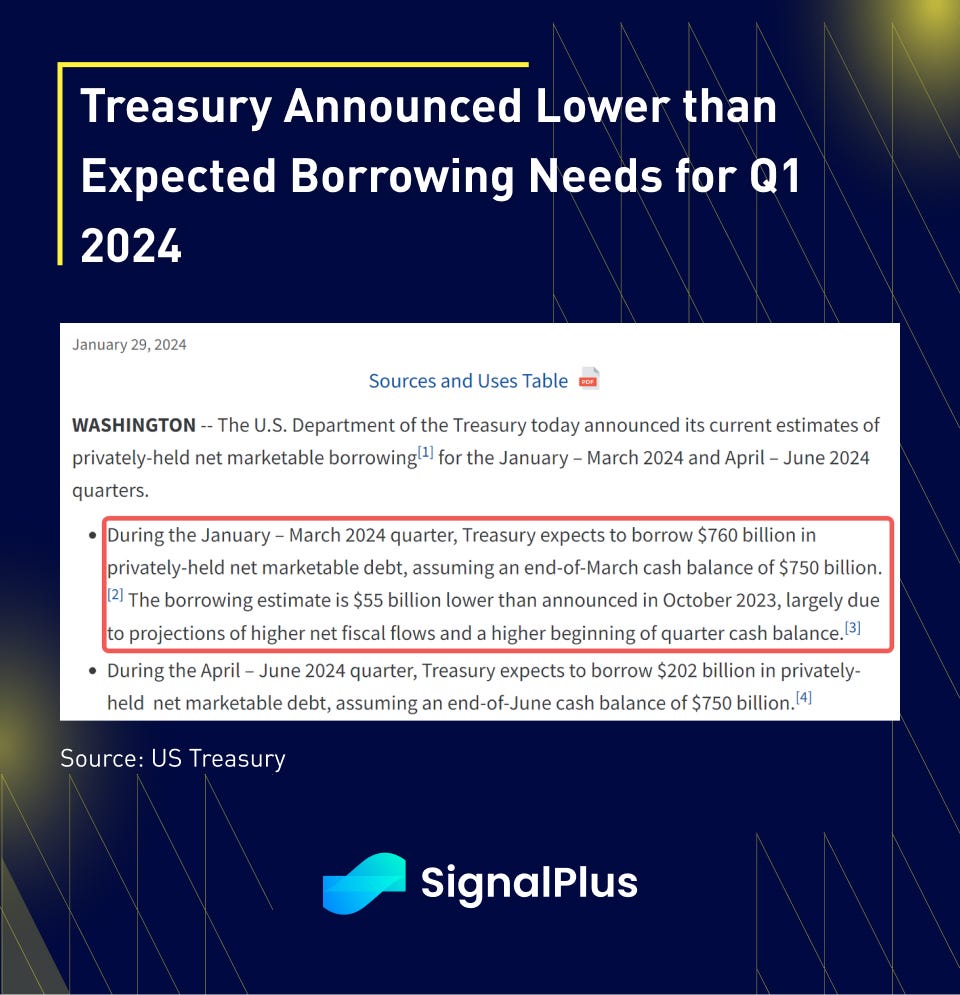

Relatively quiet data day yesterday, with the largest items on the agenda likely being Treasury funding announcement. In short, the Treasury cut its borrowing estimate in Q2 by 6.9% to $760 billion, lower than market expectations and helping to spur a small treasury rally with yields around 5–6bp lower across the curve, and SPX breaking to new ATHs.

The lower borrowing needs were spurred by higher projected fiscal flows, and having more cash on hand than anticipated at the start of the new year.

Equity / bond correlations have continued to fall, with stocks continuing to rise despite some repricing in rate cut expectations since the beginning of the year. A combination of decent economic data, coupled with dovish global central banks (cuts are a matter of when, not if) are still driving risk sentiment on, to the frustration of bears. Option markets have reflected this with call skews richening substantially in the SPX over the past 2 weeks, and even small caps are looking like they are about to break out from a 2-year long consolidation. Grinding bull markets are often the hardest to trade.

In crypto, Blackrock’s IBIT is inching ever closer to surpassing GBTC on volumes traded, just as GBTC outflows are finally showing some signs of slowing down, and spot prices have bounced accordingly with BTC back above $43.5k.

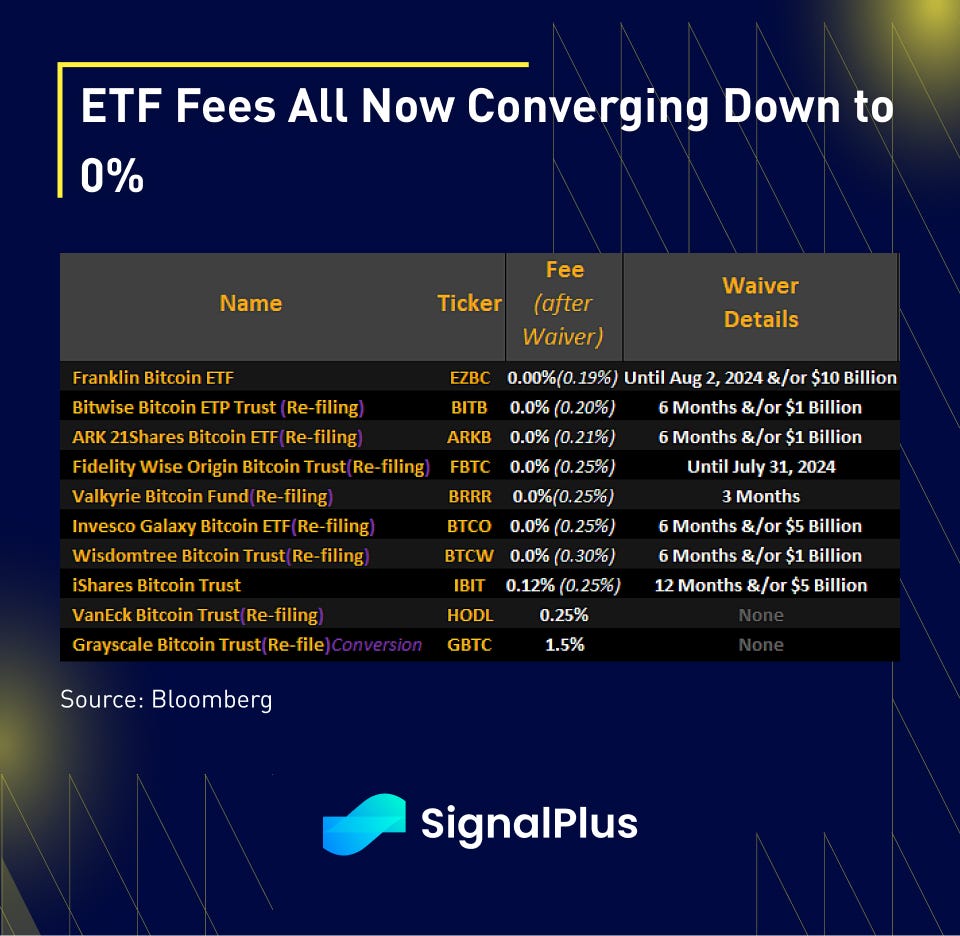

On the fees side, the price war continues with Invesco/Galaxy agreeing to cut their ETF fees from 39bp down to 25bp, inline with the rest of the providers and substantially below Greyscale’s 1.5% in fees. TradFi entries mean lower fees, lower spreads, and eventually lower alpha (increased competition)… Let’s just that the window doesn’t close too fast on us.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments