Market

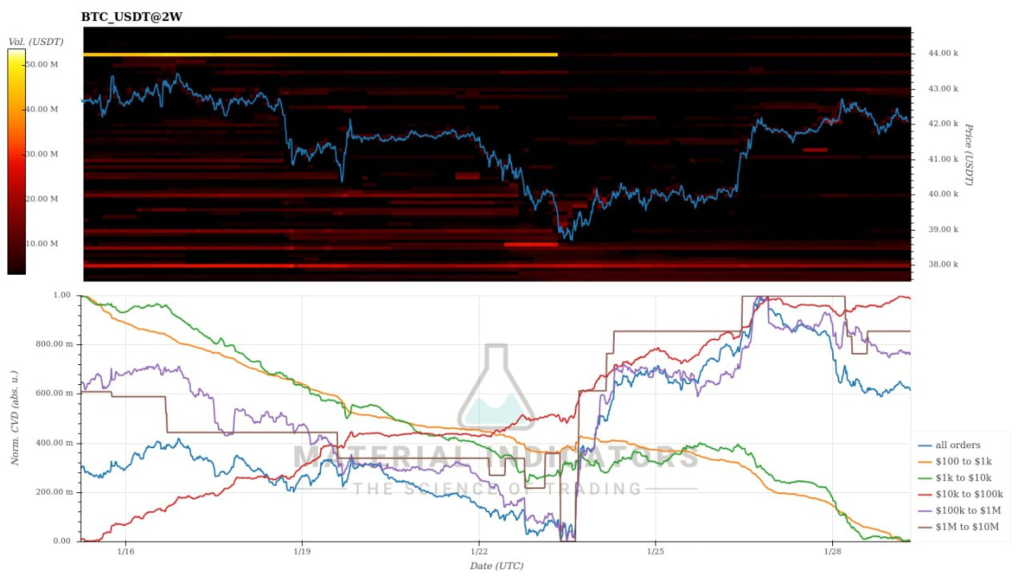

As in last week’s analysis, BTC rebounded nicely from the 38k-39k level! BTC rose to near 43k and then returned to the important level of 42k. Since many important macro events such as QRA and FOMC are scheduled this week, I think it is more likely that the market will move depending on the results of macro events rather than other reasons. I will briefly discuss my thoughts at the end of the article, but I am of the opinion that the market will continue its current upward trend.

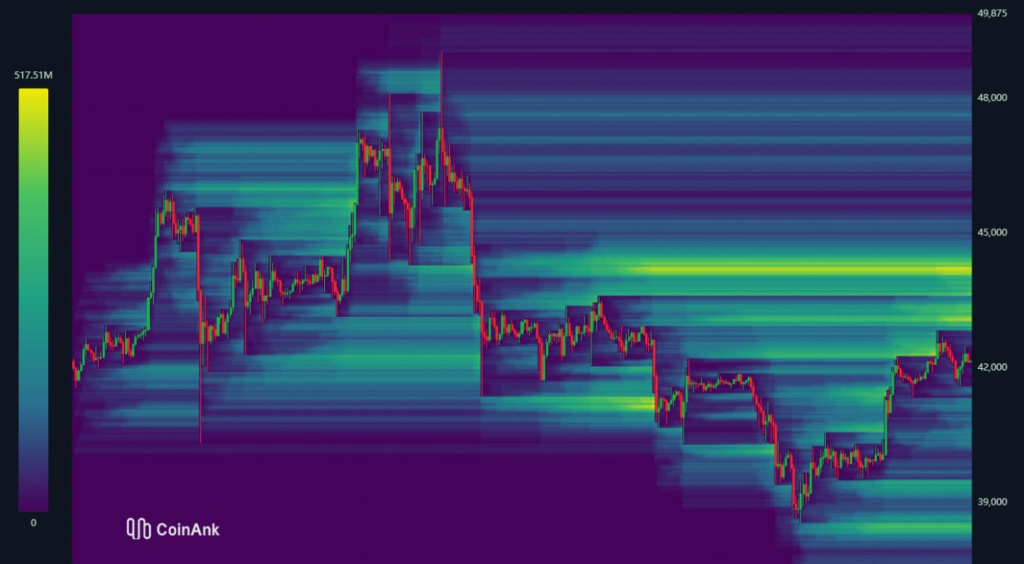

I don’t look at the liquidation map very often, but there is a lot of liquidity around 44-45k and coincidentally, that level is the most important level for BTC. This is also a good level for retesting. I’m not sure how much longer the market will trade sideways as we approach the end of January and wait for macro events, but I expect BTC to eventually reach 44k.

Also, BTC does not have large buy/sell orders at 40-45k range. I don’t know if that was intentional, but a thin order book means BTC can go anywhere. Depending on macro events, any movement, up or down, can occur. It will become clearer next week whether the current movement will end in a dead cat bounce.

ETF Flow

In the BTC ETF market, GBTC outflows are still occurring, but appear to be decreasing. BlackRock and Fidelity recorded inflows of around $2B. There are some opinions that there is no actual capital inflow as the capital outflow from GBTC flows into the remaining ETFs, but I think the market has absorbed the GBTC FUD well. Coinbase premium also recovered mostly this week. I don’t know where the exact bottom for BTC is, but the BTC ETF is clearly off to a good start. There is still a lot of potential supply of GBTC, but I have absolutely no doubts about the ETF from a long-term perspective.

Options Market

As last week, volatility continues to remain low. If ETF options are launched in the future, BTC volatility is likely to become more stable. The crypto market is a market that responds greatly to narratives. Unless there is any special news, I think this trend will continue, but there is a possibility that the short-term options market will react slightly(?) to several macro events this week. However, the current options market expectations do not seem to be high…

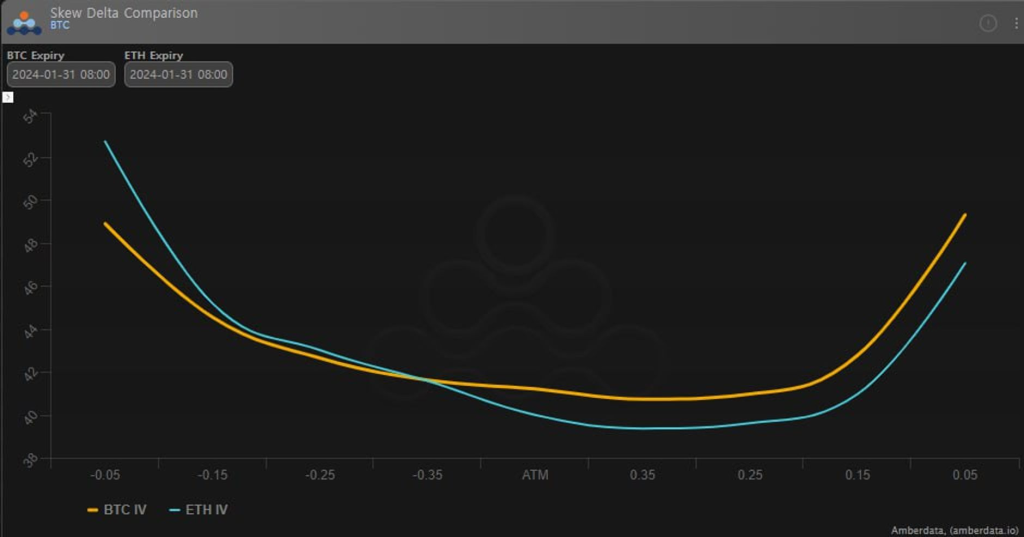

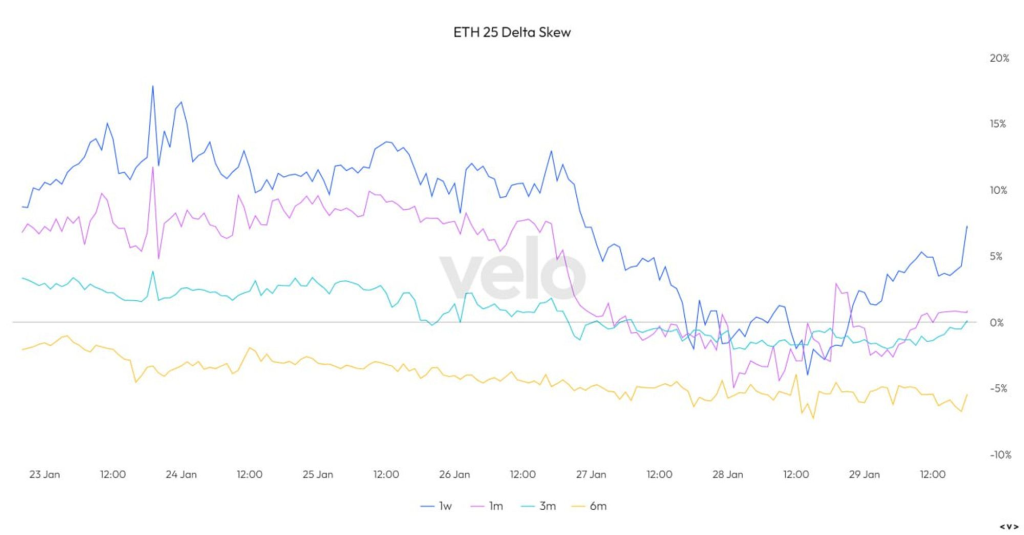

BTC shows a relatively stable overall smile, but ETH’s smile is tilted toward put options. We can see that there is demand for put options from market participants. The market still appears to be bearishly positioned on ETH.

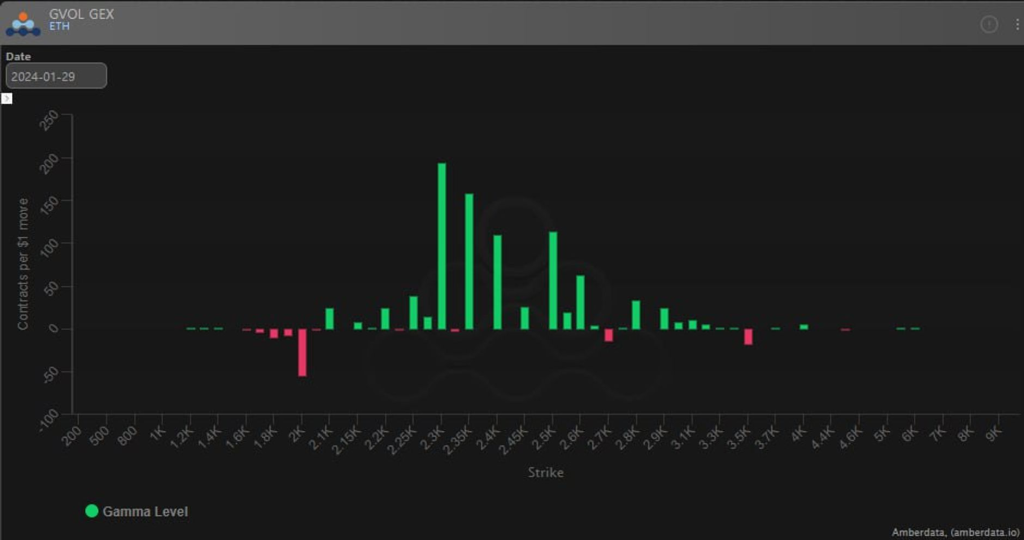

Looking at the Gamma Exposure (GEX) of BTC and ETH, we can see a clear difference in market positioning between the two assets. BTC doesn’t appear to be much different from before the monthly options expired in January. I feel like the market positioning is appropriately mixed rather than biased to one side. MM is long gamma for ETH and traders are short gamma for ETH. Last week, the ETH options market confirmed that there were a lot of call option short positions. The difference from last year is that we did not select options with very long maturities by choosing Feb/Mar options. It’s definitely not a long-term bearish sentiment.

In terms of option valuation, it appears that options are neither cheap nor expensive. The 7D VRP for 1-week to 1-month expiration options is clearly at negative levels, but it doesn’t seem like anything special. It’s hard to 100% recommend buying options, but I’m considering a call option with an expiration of 1-2 weeks.

Macro

Let me introduce the schedule first. An important event is scheduled.

- Stock market big tech earnings

- January 29: QRA (Quarterly Refunding Announcement)

- January 31: TBAC (announcement of QRA’s specific plan)

- February 1: FOMC interest rate decision (no economic outlook announced at this FOMC meeting)

- February 2: US Employment Report

Everyone may have different opinions, but I personally think it will be a very important event. Interest rates will be frozen at this FOMC meeting. There is currently no need for the Fed to raise interest rates further. PCE, announced last Friday, is the Fed’s most important price indicator and is close to the Fed’s target of 2%. What the FOMC will be paying attention to will be the talk about QT.

I consider the results of QRA and TBAC more important than the FOMC. QRA will certainly have an impact, as we are at a point where Yellen at the Treasury is more important than Powell at the Fed. This Treasury bond plan will transform the bond yield market. It is a good idea to pay attention to changes in bond yields. There are two potential scenarios, but I’m weighing scenario number one.

- If short-term bond issuance increases more than expected due to the influence of the US presidential election, the current positive atmosphere will continue and the market will rise.

- If you increase the issuance of long-term bonds, bond yields will rise and the market will fall. Since the current stock market is not properly hedged, there is a possibility of a sharp decline.

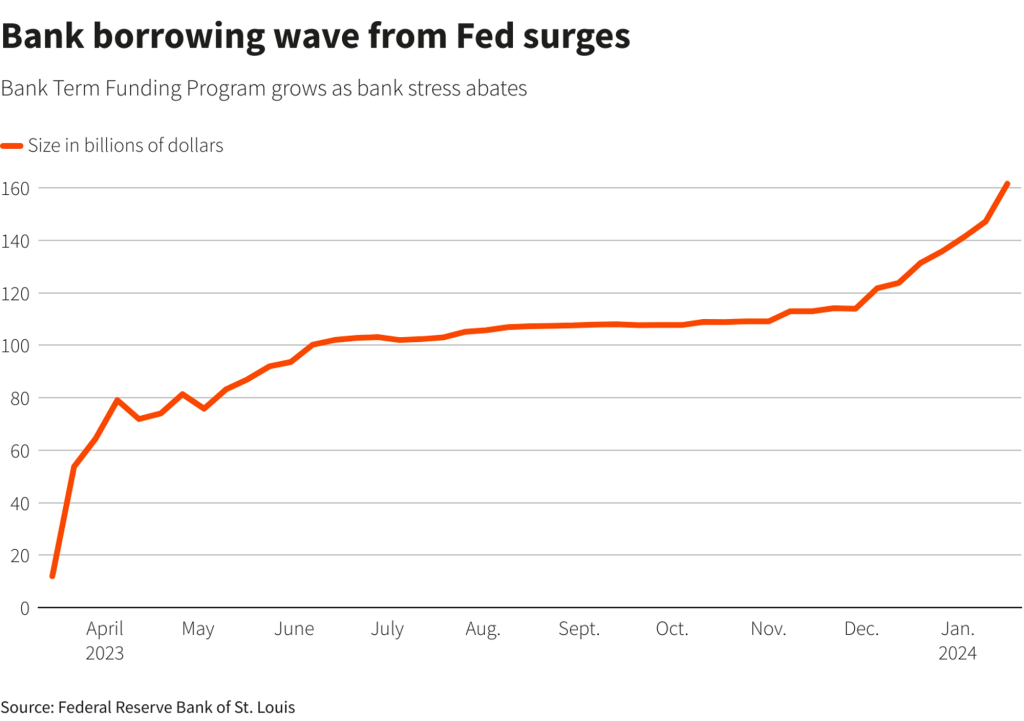

There is a lot of talk about BTFP, but I think it is difficult to say that the end of BTFP is simply a sign of market weakness. Although BTFP loan balances have increased rapidly since December, this phenomenon appears to be an arbitrage on interest rates rather than an increase in the risk of bank failure. The fact that the Federal Reserve announced the end of BTFP as planned can be seen as an intention to prevent such arbitrage. As evidence, the Fed changed the BTFP rate. Additionally, discussions are currently underway to activate the discount window. If the stigma effect is removed and the use of the discount window is activated, it seems likely that the potential bankruptcy risk of banks will be reduced.

Good luck to everyone this week!

Comments