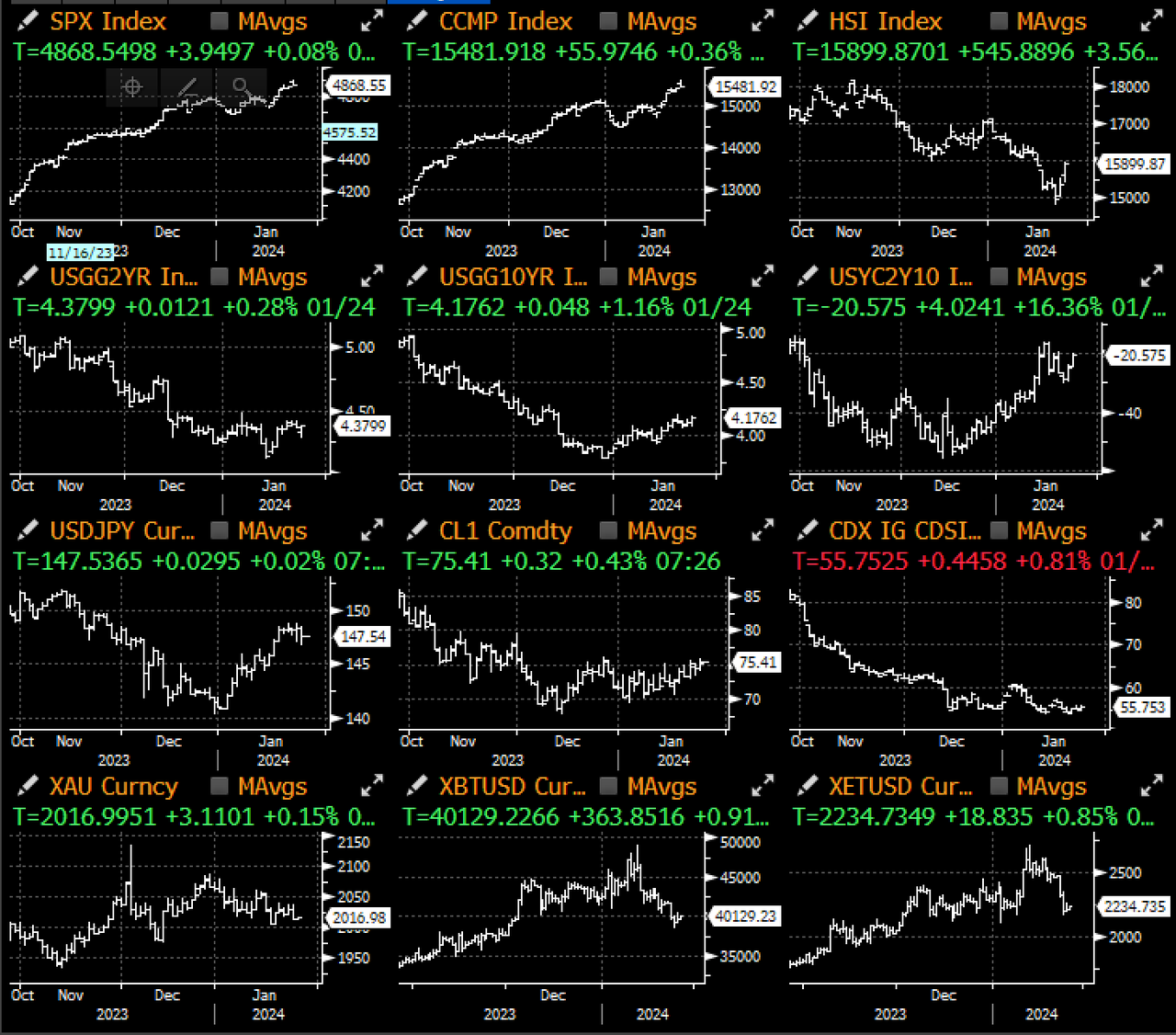

US rates continued its gentle ascension higher, with risk sentiment continuing to improve on the back of the surprise RRR cut from the PBOC, a stronger than expected US PMI, and a terrible 5yr auction with trading volumes.

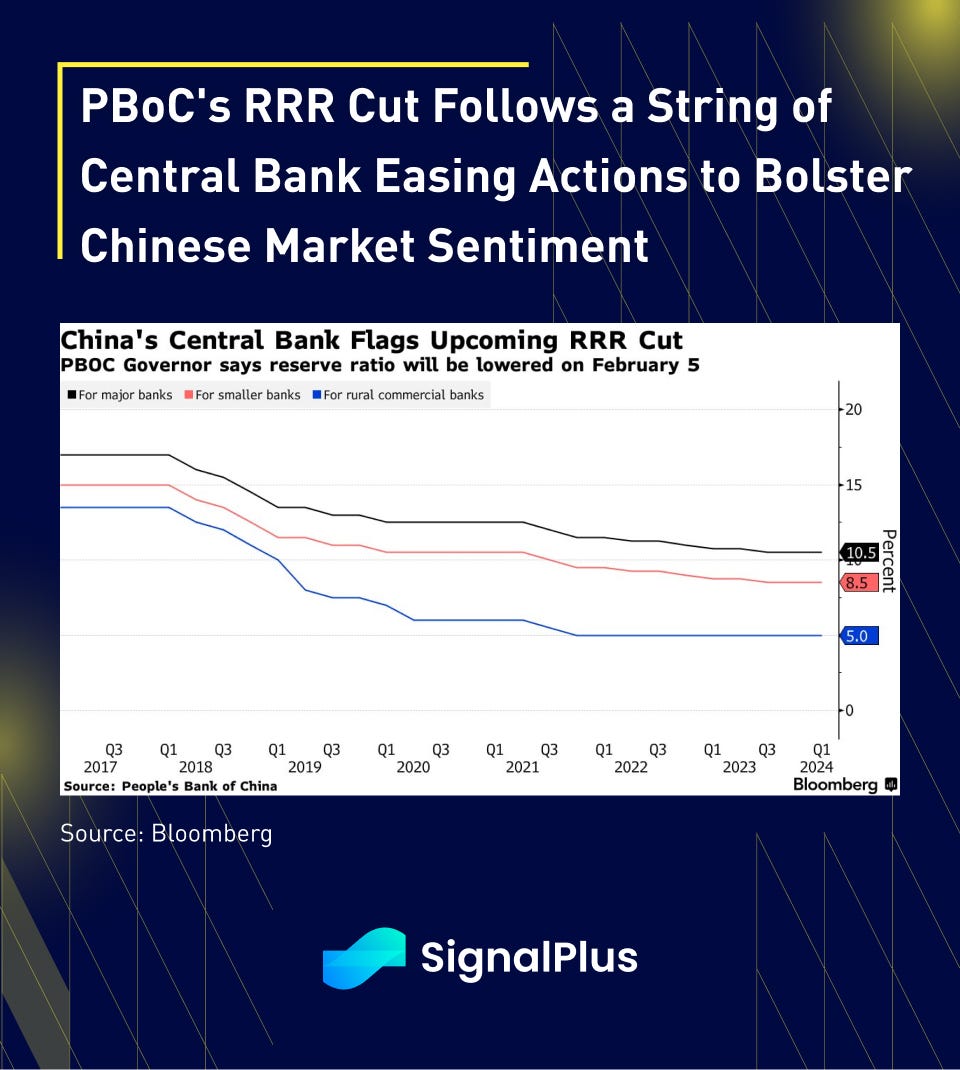

During a Central Economic Work Conference, PBoC Governor Pan Gongsheng announced that the RRR will be cut by 50bp on February 5th, and the gesture will be a part of a broader set of market stabilizing measures that policymakers will be rolling out. The move came as a bit of a surprise to the market not just on its timing, but also in the method of delivery as the Governor chose to deliver the message himself and during market hours. Furthermore, the PBoC announced that they will be setting up a “credit market department” to specifically focus on the 5 major tasks as previously outlined in the areas of technology finance, green finance, inclusive finance, pension finance, and digital finance. Will we be seeing the central bank influence and direct targeted loan growth to specific initiatives going forward? In case any, it would appear that Chinese policymakers are seriously increasing resolve to support market sentiment at this juncture.

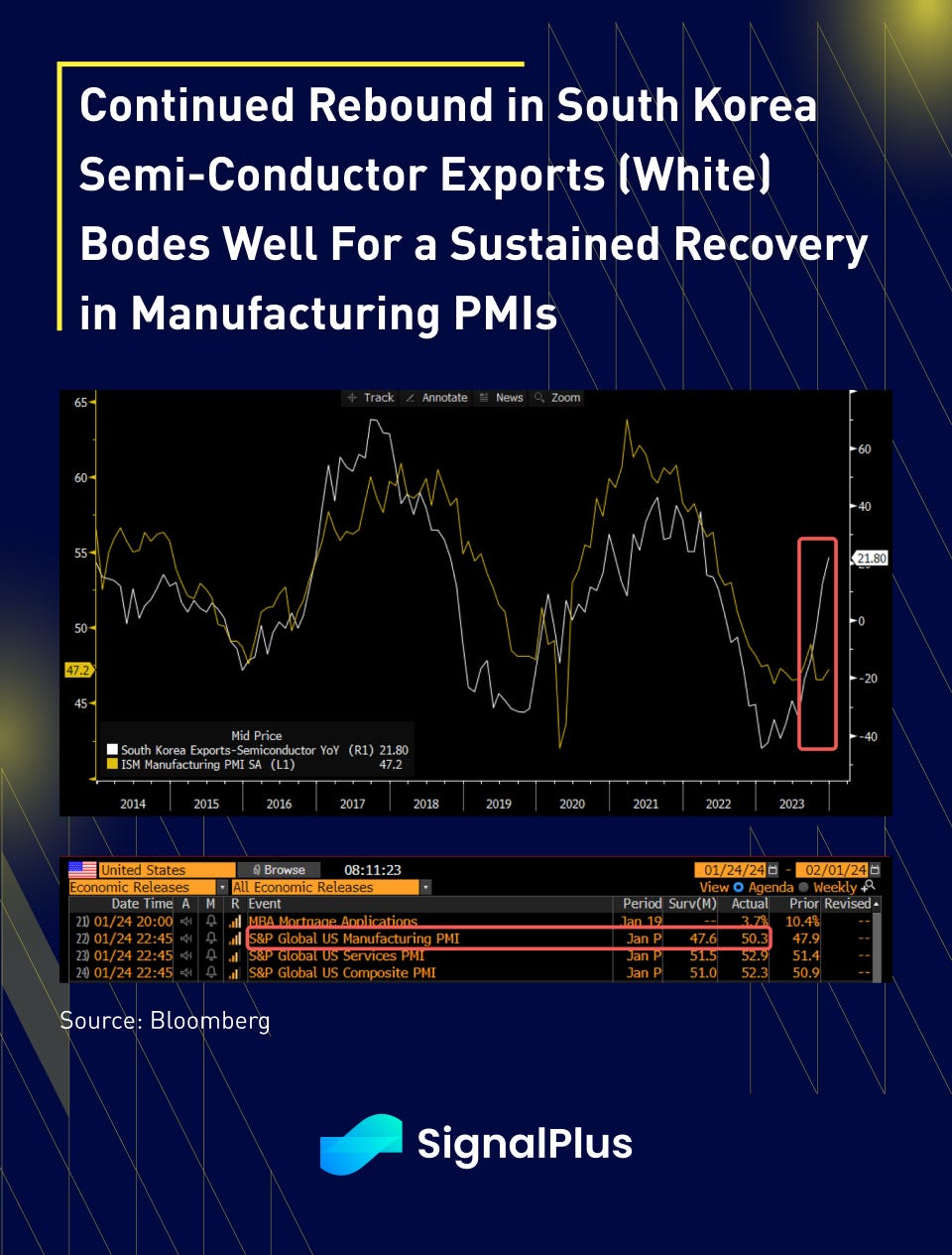

In North American markets, the US PMI release coincided with the Bank of Canada rate decision, which saw continued pressure on bonds as manufacturing data came in stronger, while the BoC left key passages over lingering inflation concerns despite keeping rates on hold. US Manufacturing PMI increased to 50.3 from 47.9, with the majority of improvements coming from new orders (52.3 from 47.1), while Services PMI also surprised higher at +1.5pts versus last month. A continued rebound in South Korean semiconduct exports (YoY%) continues to bode well for a sustained manufacturing recovery, with the former being a statistically significant leading indicator for global PMIs.

For the Bank of Canada decision, while the BoC left rates unchanged and removed the explicit hiking bias from the statement, they added a key passage stating that “the council is still concerned about risks to the outlook for inflation, particularly the persistent in underlying inflation”, giving further upward pressure on rates just ahead of the 5yr treasury auction.

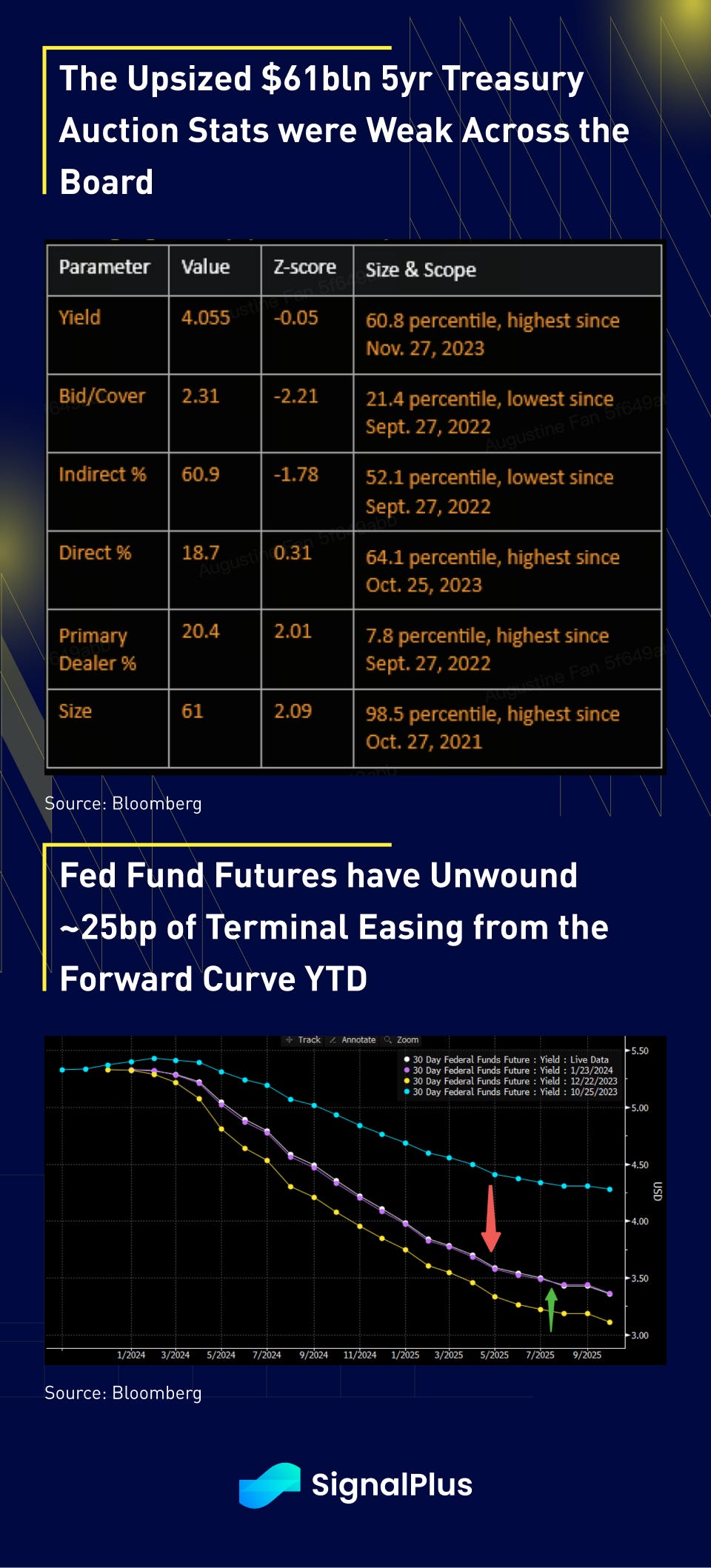

The $61bln 5yr treasury auction proved to be a hard pill for the market to swallow, with the issue coming with a massive tail at +2bp back from market pricing, and the 2.31x bid to cover ratio meaningful below the 2.52x average. Internals were weak across the board, with many metrics sitting at close to 6-month lows, and the weak result pushed yields another 5bp higher on the day. Furthermore, the recent bond sell-off has effectively removed around ~25bp of terminal easing since the beginning of year, with ‘only’ 125bp of easing priced in 2024 instead of 150bp+ earlier in the month.

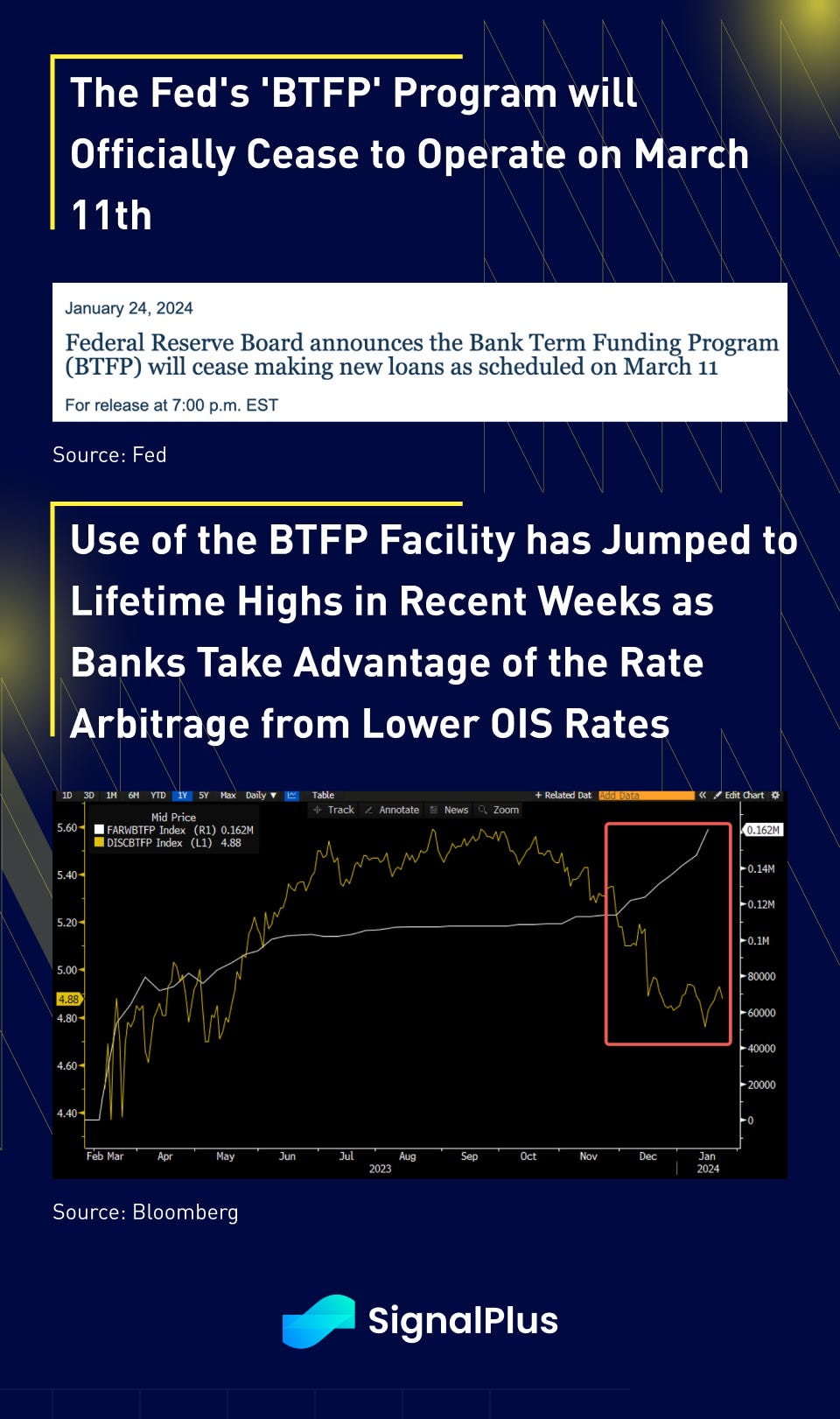

On a separate note, the Fed has announced that the aptly-named ‘BTFP’ (Bank Term Funding Program) will officially cease on March 11, ending the emergency protocol that was created in the wake of the SVB crisis. The program’s uptake has recently jumped to all the highs, as Wall Street banks have taken advantage of (abused) the rate arbitrage available thanks to the drop in implied OIS rates to borrow-and-repark back in the system. As the old saying goes, ‘never let a good crisis go to waste’, and investment banks are surely masters of taking that advice to heart.

Equities closed the day with a small gain, giving back some of the early day strength from the China easing boost. Energy and large-cap tech stocks led the way up once again, despite Tesla reporting disappointing earnings as the 1st of the ‘Magnificient 7’ failed to impress. Earnings, revenue, and gross margin all came in below estimates, and the company warned that volume growth may be “notably” lower in 2024. The next 2 weeks will see a peak in earnings announcements, coming right in time with a slew of important macro indicators around month-end.

In crypto, the first 8 day post spot ETF approvals has seen many records being broken in terms of post-launch trading volumes, though winners are quickly emerging with the Blackrock and Fidelity offerings taking well over 60% of the ex-GBTC market share.

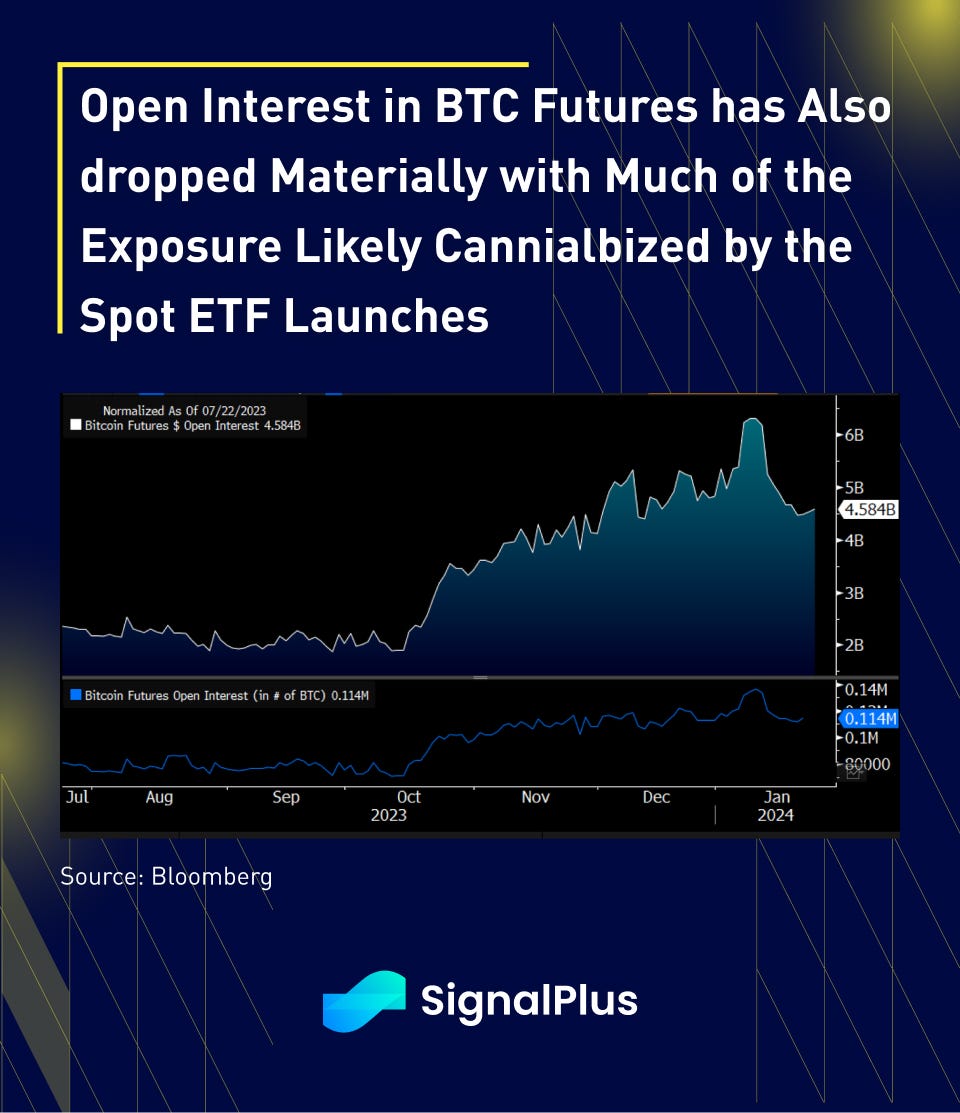

Nevertheless, the market mood remains heavy, with cumulative GBTC outflows almost single-handedly offsetting the collective inflows of the other 9 ETFs. Furthermore, the trading turnover (not pure volume) of GBTC has been shrinking over the past few days, and BTC futures open interest has shrunk materially as some of their activity has been cannibalized by the spot ETFs. All in all, prices will likely continue to normalize and ease off in the near-term, as the market continues to work through the short-term outflow imbalance and lack of immediate positive catalysts.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments