Despite another decent week for risk assets in the past week, there was a palpable disturbance in the disinflationary force last week, with CPI and PPI data both coming significantly above expectations. On the other hand, US data remained robust U-Michigan sentiment rising for a 3rd month in a row to the highest levels since 2021. PPI final demand came in hotter than expected with core printing +0.5% MoM and headline adding +0.3% MoM, driven entirely by services inflation. Furthermore, rises in global shipping prices from ongoing geopolitical conflicts threaten a resurgence in goods prices in the months ahead, adding further challenges to the disinflation narrative.

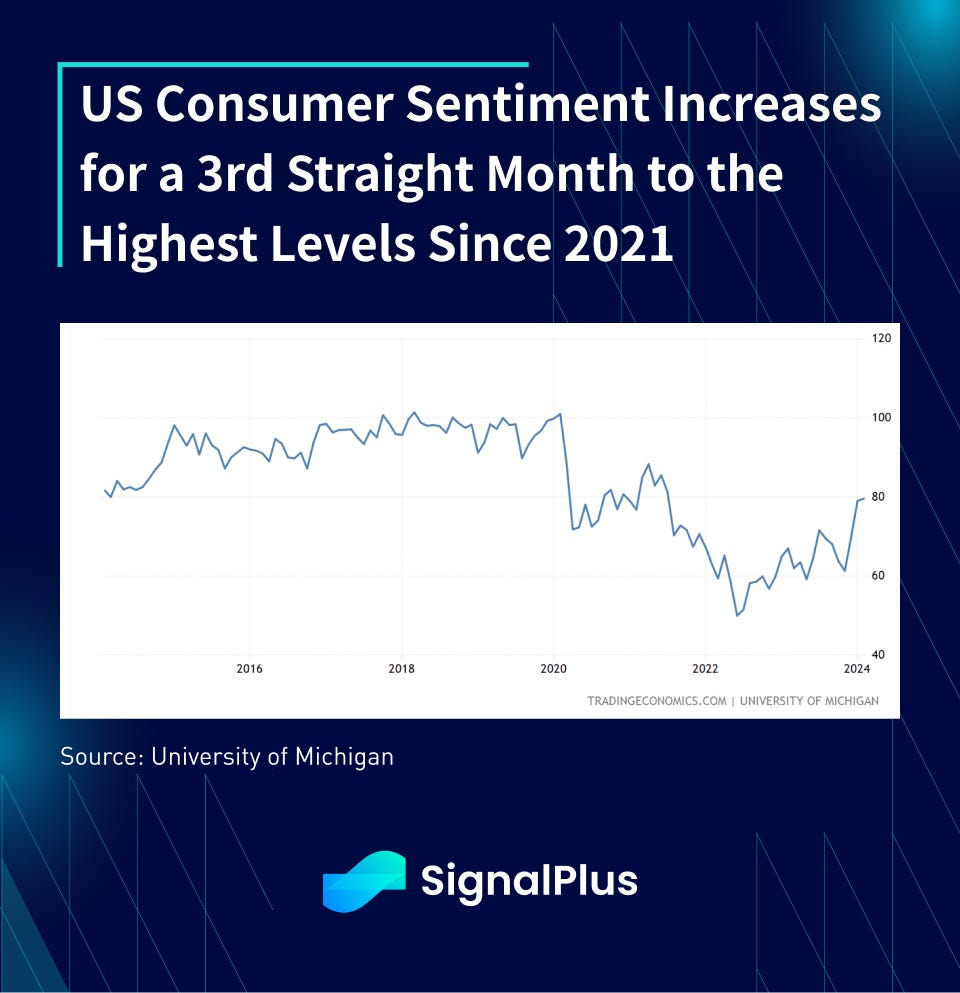

Additionally, U-Michigan consumer sentiment improved to 79.6 for February, the highest levels since July 2021, led by a rise in current expectations. The 12-month price measure ticked up to 3.0% while longer-term gauges held constant at 2.9% for the 4th straight month.

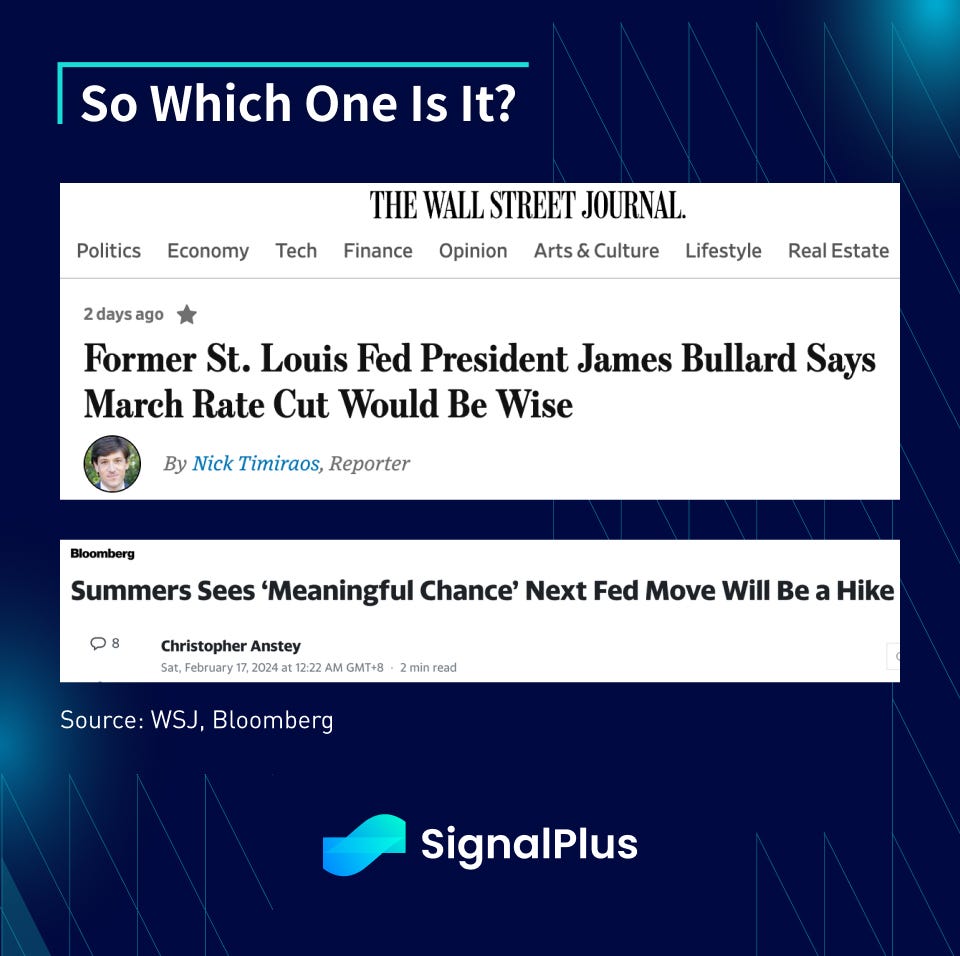

The strong economic prints prompted the outspoken Larry Summer (ex-Treasury Secretary) to declare on Bloomberg TV that there’s a meaningful chance (15%) that the next interest move could be a hike.

There’s a meaningful chance — maybe it’s 15% — that the next move is going to be upwards in rates, not downwards,” Summers said on Bloomberg Television’s Wall Street Week with David Westin. “The Fed is going to have to be very careful.”

Source: Bloomberg TV

He caveated the statement somewhat by agreeing that one shouldn’t over-interpret a single figure, but that there are signs of a “mini-paradigm shift” with rising core service prices and an “explosive” super-core print in January:

“It’s always a mistake to over-interpret one month’s number — and that’s especially true in January, where calculating seasonality is difficult,” said Summers, a Harvard University professor and paid contributor to Bloomberg TV. “But I think we have to recognize the possibility of a mini-paradigm shift.”

“That’s not the only disturbing indication,” he said. Another key concern is core services prices — which leave out food and energy costs — excluding housing, which have been pushed up by higher wages. “It sure looks like super-core was explosive in January,” he said in reference to that measure.

Source: Bloomberg TV

On the other hand, former St. Louis Fed James Bullard (a noted dove in the previous cycles), stated that he thinks the Fed should start cutting rates in March as a preemptive move to prevent a restrictive policy stance from restraining economic activity in the 2H, risking larger and faster cuts later on down the time.

“I think they should get going,” he said after speaking at a conference of the National Association for Business Economics in Washington. “It’s probably wiser to go sooner but slower.”

“I’m worried that you’re going to get into the third quarter, and the policy rate is going to be too high for that situation, so why not go now,” he said. “You don’t have to say you’re going to do six [cuts]. You would say, ‘We’re making one move based on the data that we have in hand, and we’re not guaranteeing anything more.” — — James Bullard via WSJ

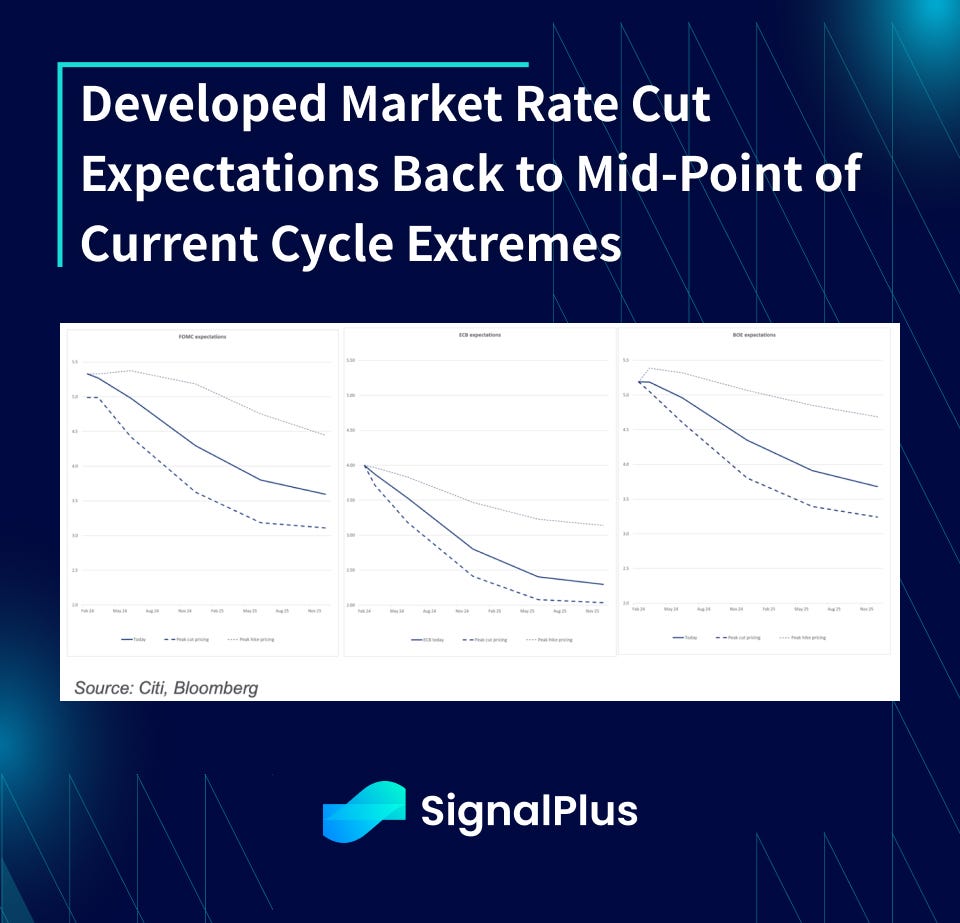

As we noted in our 2024 outlook, our bias is more towards the Summers camp, where we think the risk is for inflation to be stickier than market expects, challenging the current rate cut narratives and putting a “No-Landing” scenario (ie. economy is too strong) back in the realm of possibilities. Indeed, we have already started to see an unwound of ~50bp of easing expectations from the January extremes for the Fed and BoE, and 25bp for the ECB since the January lows.

Furthermore, taking a few steps back, the global economy does continue to look very robust with global PMI basing around 50bp and showing recent signs of a nascent recovery, while global labour market continues to defy all nay-sayers with record strength across most developed economies.

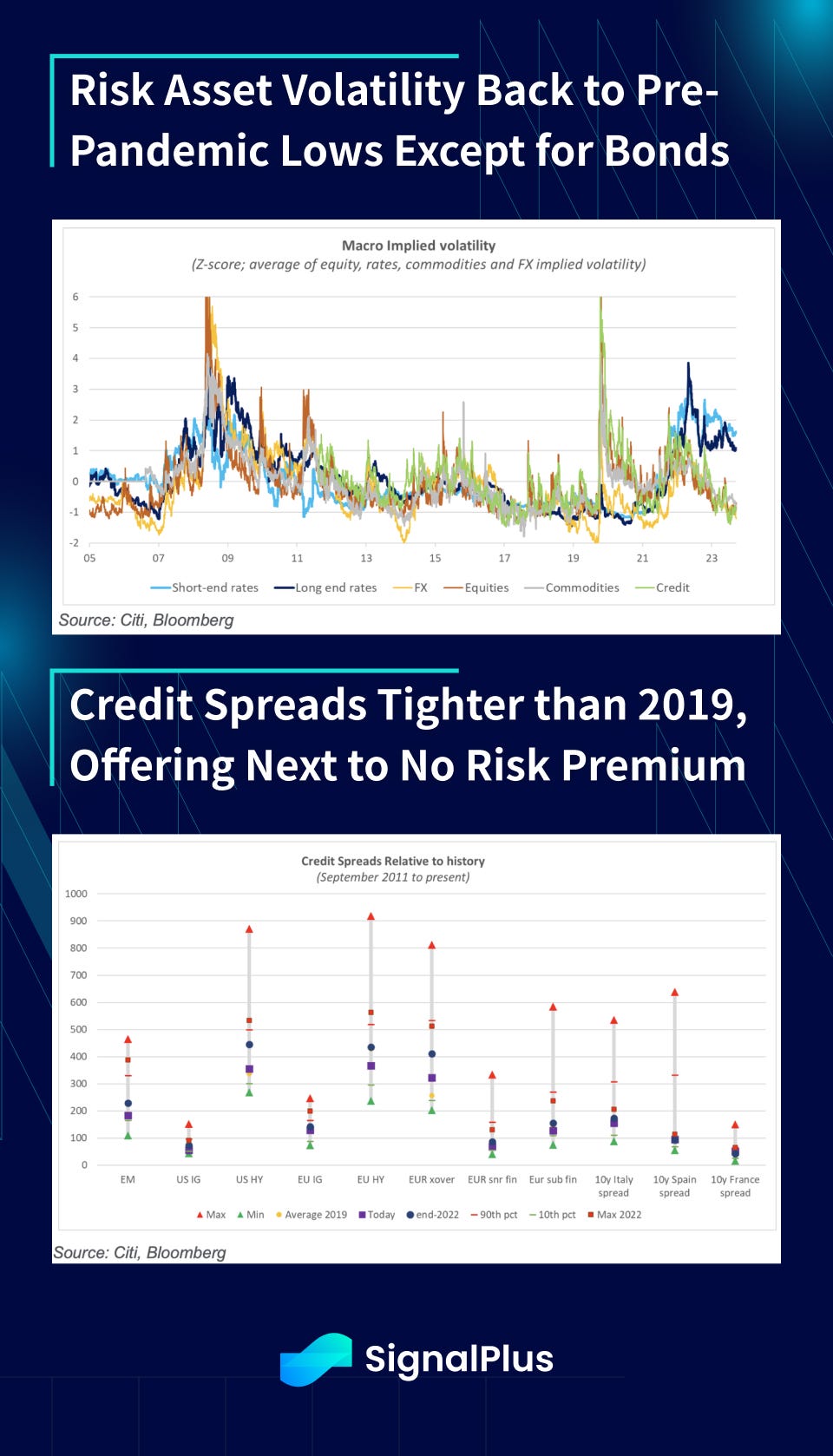

At the same time, risk pricing remains immaculate with macro asset vol back to pre-pandemic lows except for fixed income, while credit spreads are tighter than 2019 levels as there is very little risk premium being priced into macro asset classes across the board.

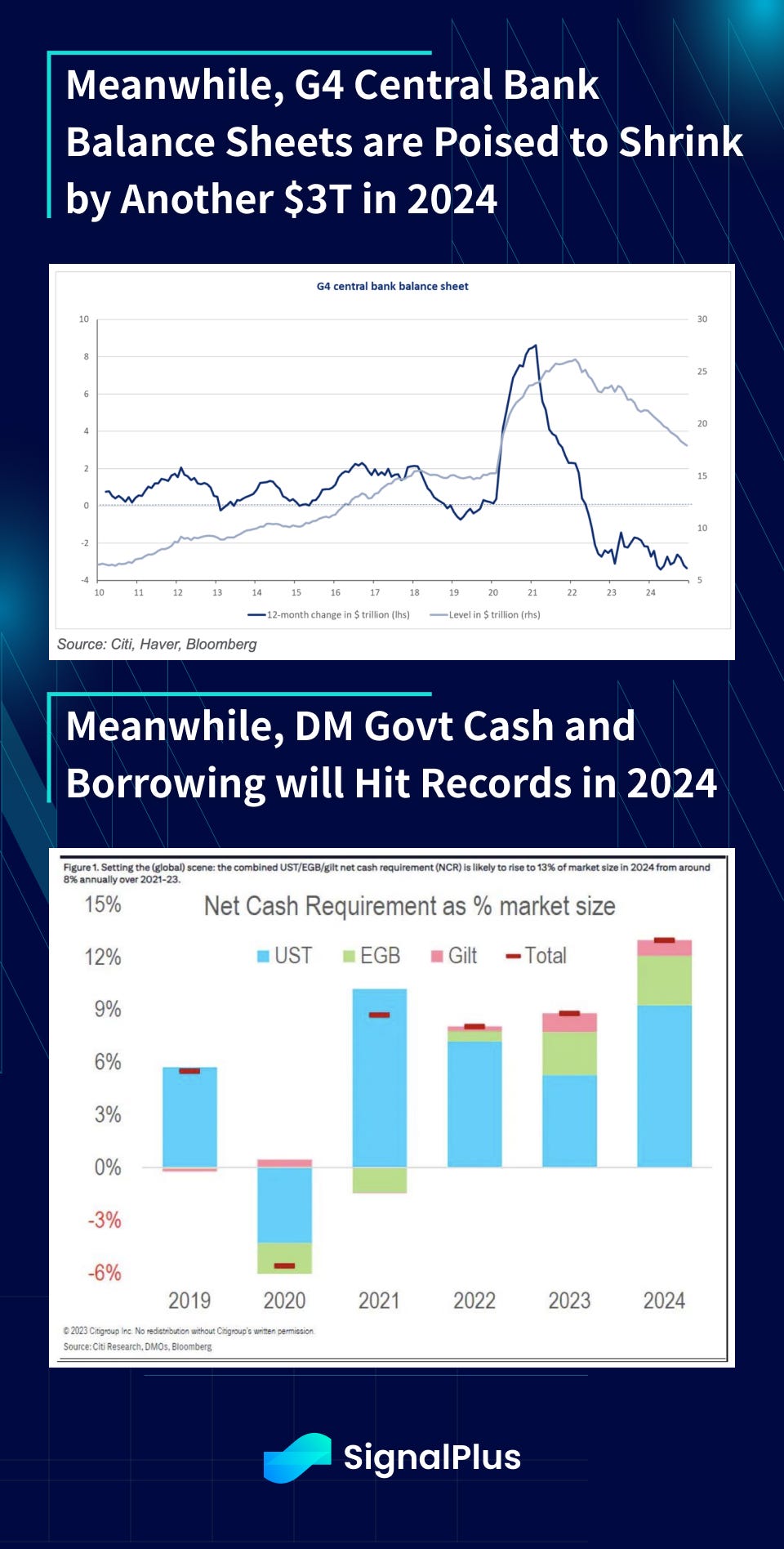

Furthermore, while investors are the most bullish on fixed income as they have been for years, this is happening against the tailwind of the G4 Central Bank shrinking their balance sheet (QT) by yet another $3T in 2024, unwinding ~80% of the post-pandemic pump. Meanwhile, cash borrowing needs as a % of bond market cap is at record highs in 2024 across the US, Europe, and UK, even with our economies remaining in expansion stage, and this % will only further should we (finally) witness any economic slowdown later this year.

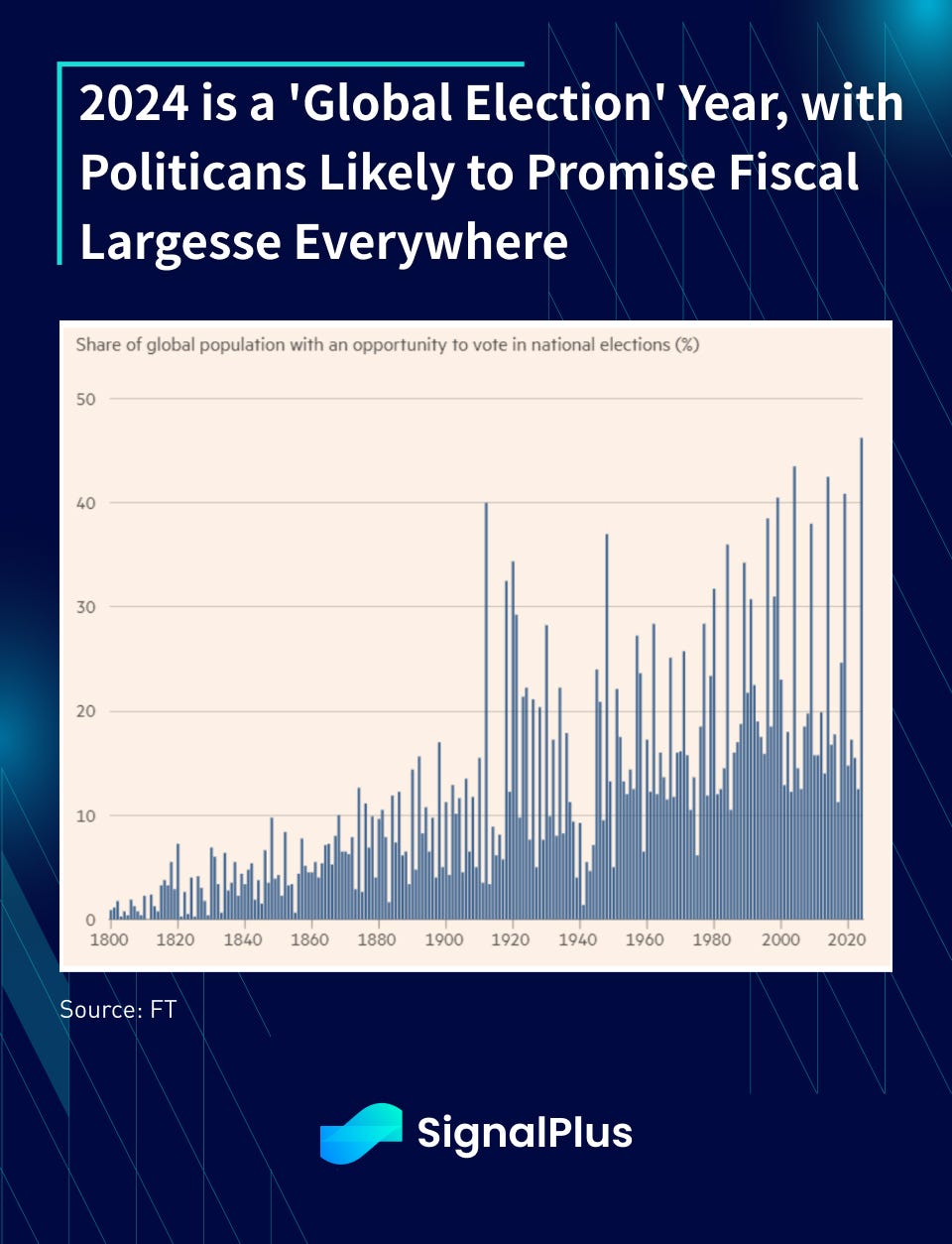

Speaking of fiscal largesse, FT has an interest stat showing that 2024 will see a record %-share of the global population voting in national elections, with political candidates likely promising spending campaigns and putting fiscal spending pressures on their respective treasuries.

Anyway, the main takeaway is — there’s going to be a lot of bonds being issued in 2024 and beyond, thereby likely keeping a floor on interest rates.

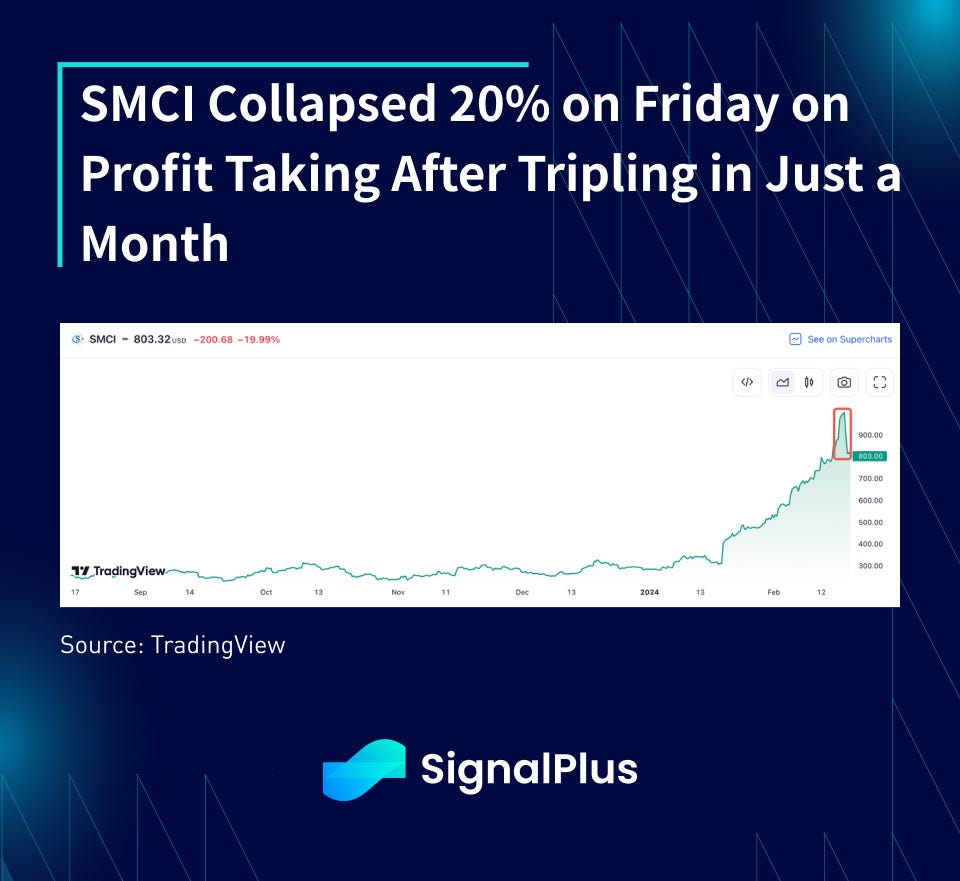

US Equity markets saw a small reversal from its ATHs after initially brushing off the high CPI and weak retail sales prints, with SMCI (semi chip manufacturing) collapsing 20% intraday after tripling in 4 weeks. Nvidia will be the elephant earnings release this week (Feb 21st) with expectations of riding high on the AI boom, and likely to dictate overall equity risk sentiment for the month ahead.

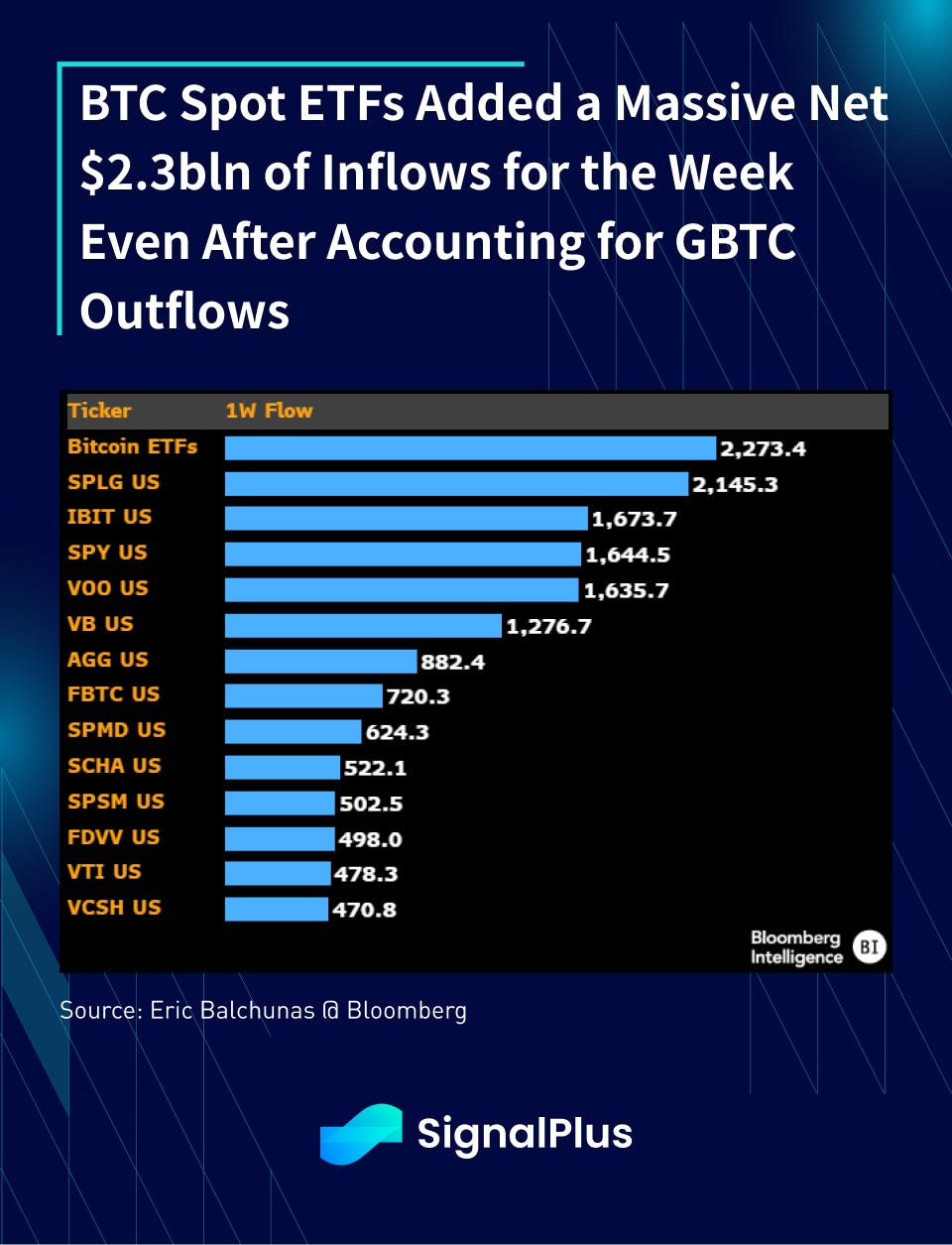

In crypto, spot ETFs added a net of +$2.3bln last week, and $5bln in total LTD, after netting for GBTC outflows. This is collectively larger than the net in-take out of bellwether ETFs such as SPY (SPX ETF), which is an impressive feat for sure.

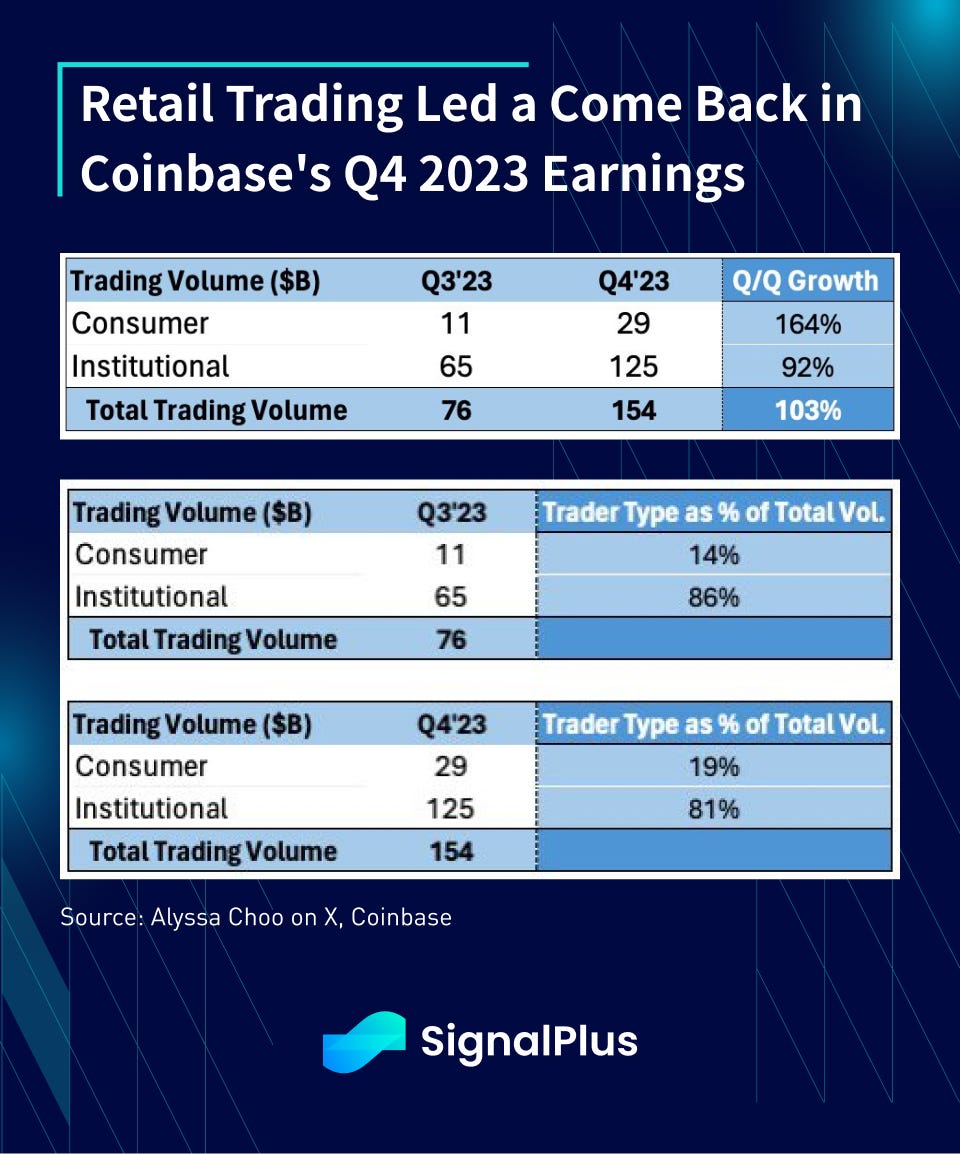

A further positive canary in the coalmine came out of Coinbase’s earnings report, which showed that retail trading volume jumped +164% vs last Q, vs total trading volume growth of +103%. There’s still some ways to go before retail participation can retake the peaks saw in late 2021, but it’s encouraging to see a return of some mainstream interest as we emerge out of a very long winter.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments