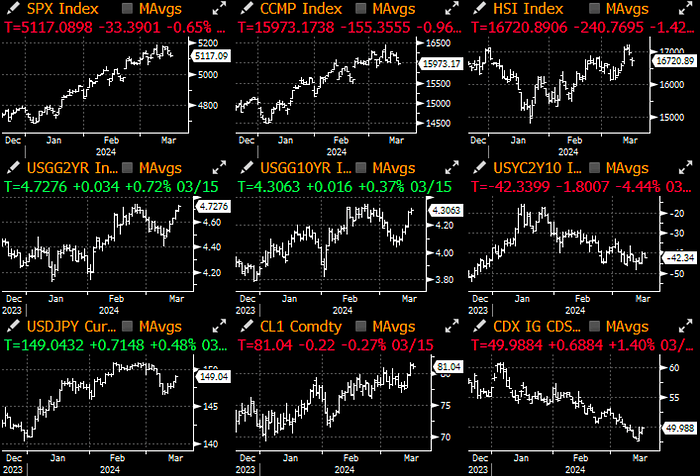

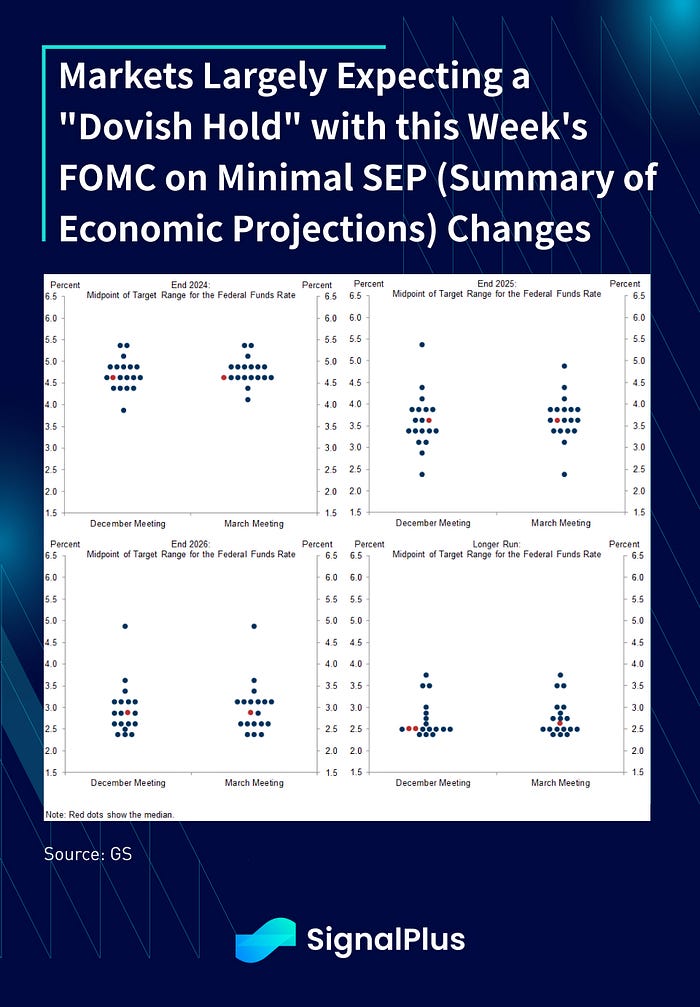

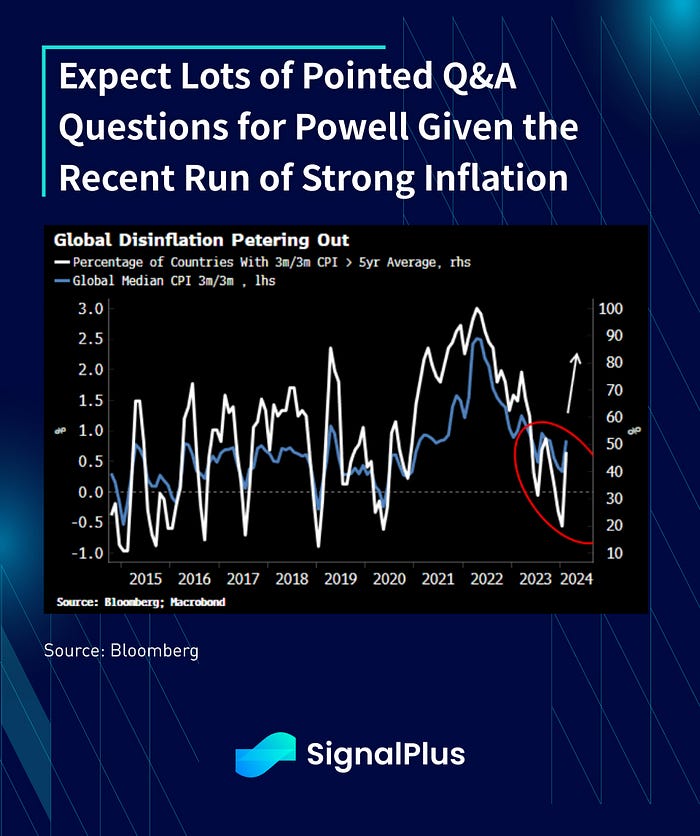

Markets ended last week with a rising tension between divergent growth and inflation surprises as we head into FOMC this week. While Wall Street mostly expects the Fed to execute a ‘dovish hold’ with 3 cuts remaining in the median dot-plot, expect the Q&A to be filled with lots of pressures and questions for the Chairman on the recent run of hotter-than-preferred inflation and easy financial conditions.

Outside of the FOMC, this is going to be a very busy week of central bank meetings, with well over 10+ Central Banks holding monetary decisions, headlined by the BoJ/Fed/BoE/RBA. Overriding consensus is for the majority of policy makers to maintain a dovish stance regardless of their actions, though the BoJ decision is likely going to be the most nuanced given the potential exit from their long-standing NIRP / YCC policy.

Extremely Busy Week of Central Bank Meetings This Week (Credit: Citi)

BoJ | NIRP removal possible, but with dovish risk

FOMC | Hold. Risk in dot plot projections

SNB | 25bp rate cut more live than what’s priced

Norges | Slight dovish risk in MPR projections

BoE | Dovish risk in vote split and guidance

RBA | Slight dovish risk to guidance

BCB | 50bp cut, hawkish forecasts and FG adjustment

CNB | 50bp vs 75bp cut, we lean to former

Banxico | 25bp cut to begin easing cycle

Banrep | Rate cut acceleration to 50bp

CBT | Rate hike risk, not our base case

CBC | Slight hawkish risk in language

PBoC | No change to 1y/5yr LPR Rates

Source: Citi

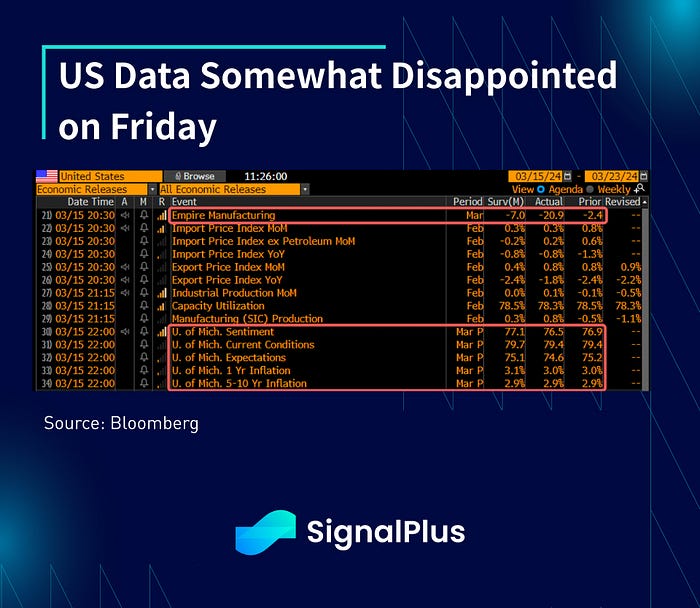

US data was otherwise soft on Friday, with US Empire manufacturing significantly below expectations (-20.9 vs -2.4 last month), with large misses across employment and prices paid components. Consumer sentiment also dipped slightly versus previous months, with inflation expectations steady at ~3% and still well above Fed’s long-term target.

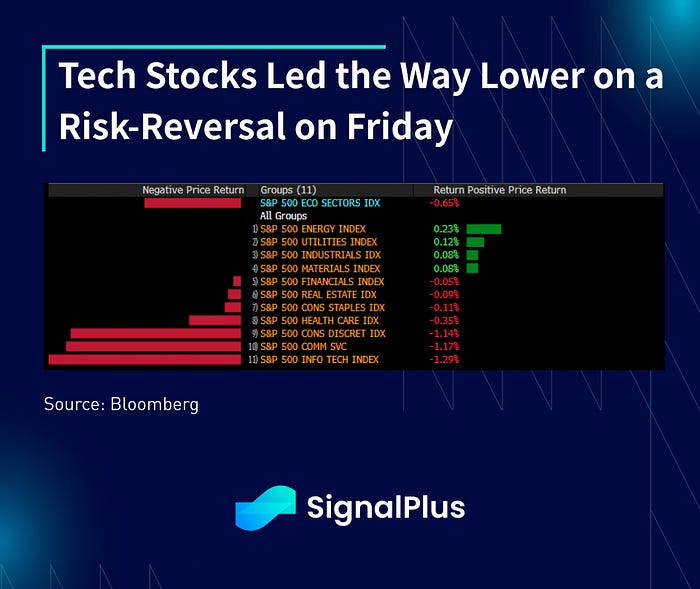

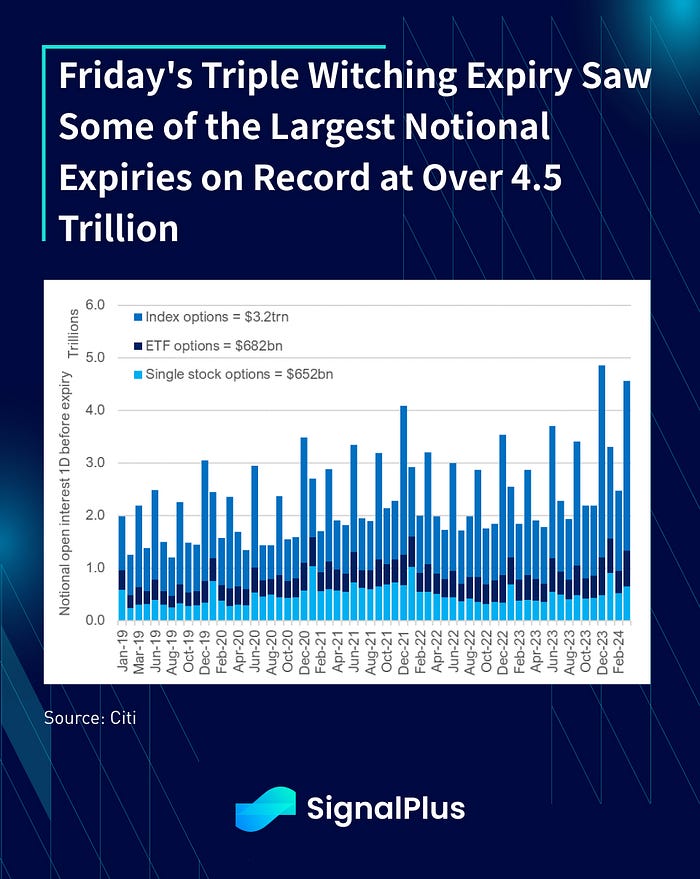

Equities ended the week on the soft side with tech names leading the way down as traders took some chips off the table after a frantic YTD rally. Furthermore, Friday saw some of the largest option expiries on record with over 4.5 trillion in equity notionals rolling off across indices, ETFs, and single name stocks, with the session dominated by risk repositioning and delta hedging ahead of the triple witching close.

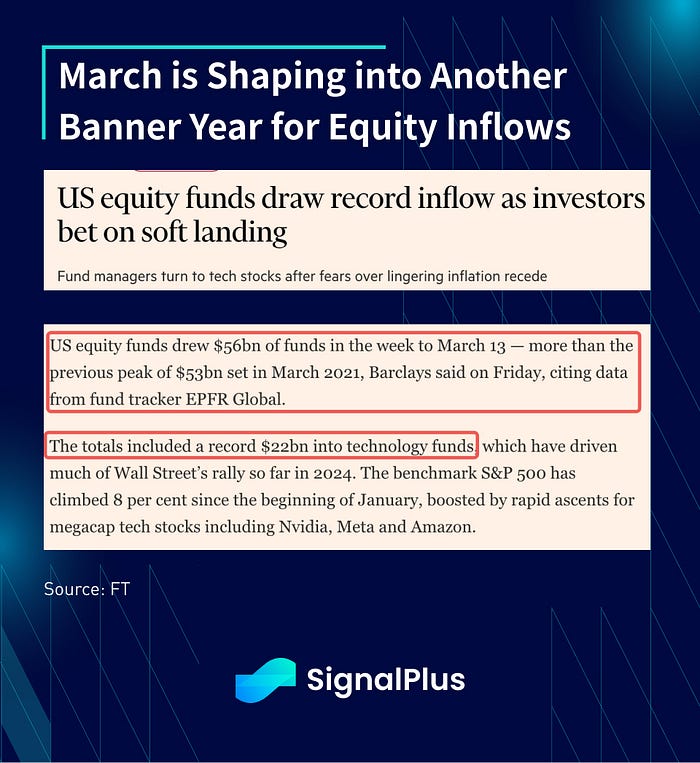

However, despite the small setback, March is still shaping up to be another record month for equities with investors piling in a record $56bln into stocks during the first two weeks of March ($22bln into tech), with market concentration (as measured by market cap) heading to extreme levels last seen in 1932.

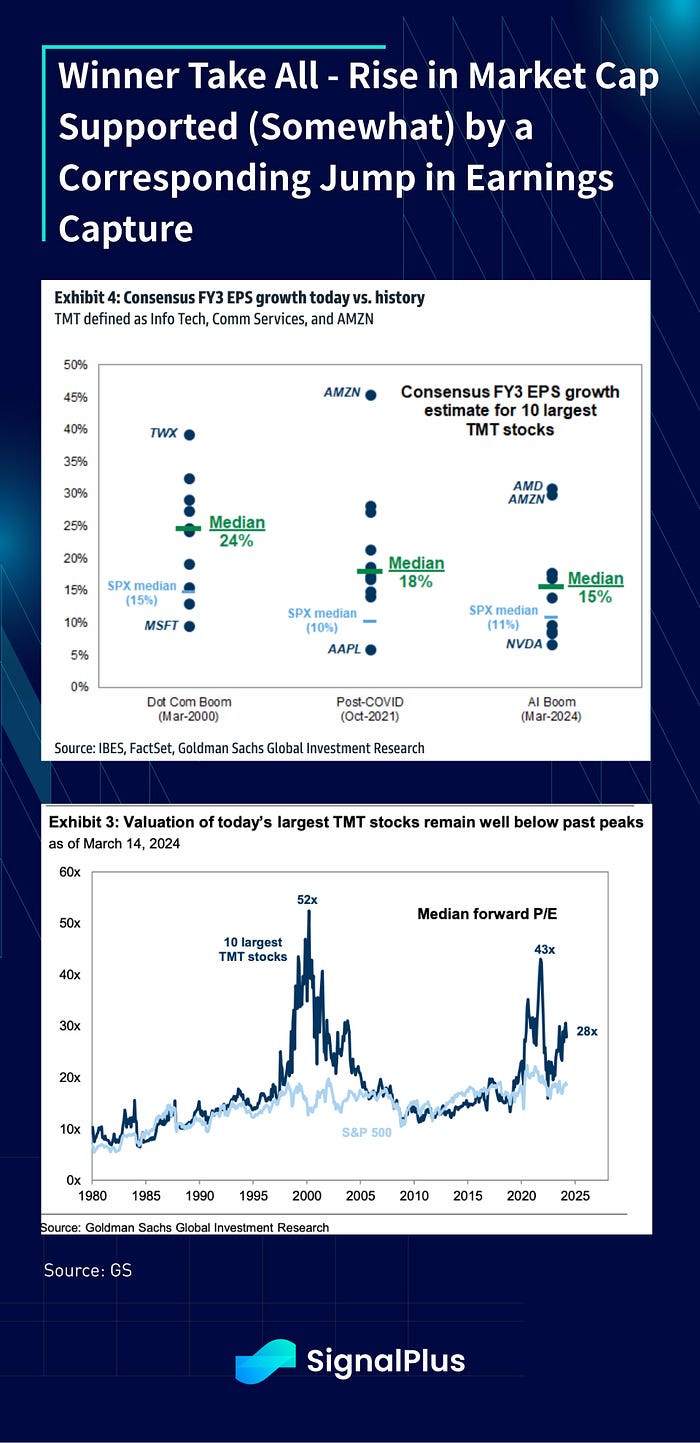

However, investment (and strategiests) remain somewhat sanguine about the concentration risks, given that its rise is matched by a similarly meteoric jump in earnings growth vs the median stock. With tech names responsible for the lion’s share of SPX EPS, the jump in stock prices have ‘merely’ taken the forward PE multiple to 28x, vs previous ‘bubble’ highs of 52x and 43x in 1999 and 2021, respectively. While expensive on an absolute basis, investors feel like they have little choice but to ‘pay-up’ for large-cap exposure to AI, given its omnipresent influence on everything we seem to be doing nowadays.

Over in crypto, prices have had a rough 72 hour adjustment with spot BTC dropping from ~$73k down to ~$65k over the weekend, methodically stopping out a fair number of long-exposures and dip-buyers during that period. As we touched on late last week, near-term euphoria seems to have been over-done with palpable signs of excess across the altcoin / memecoin spaces.

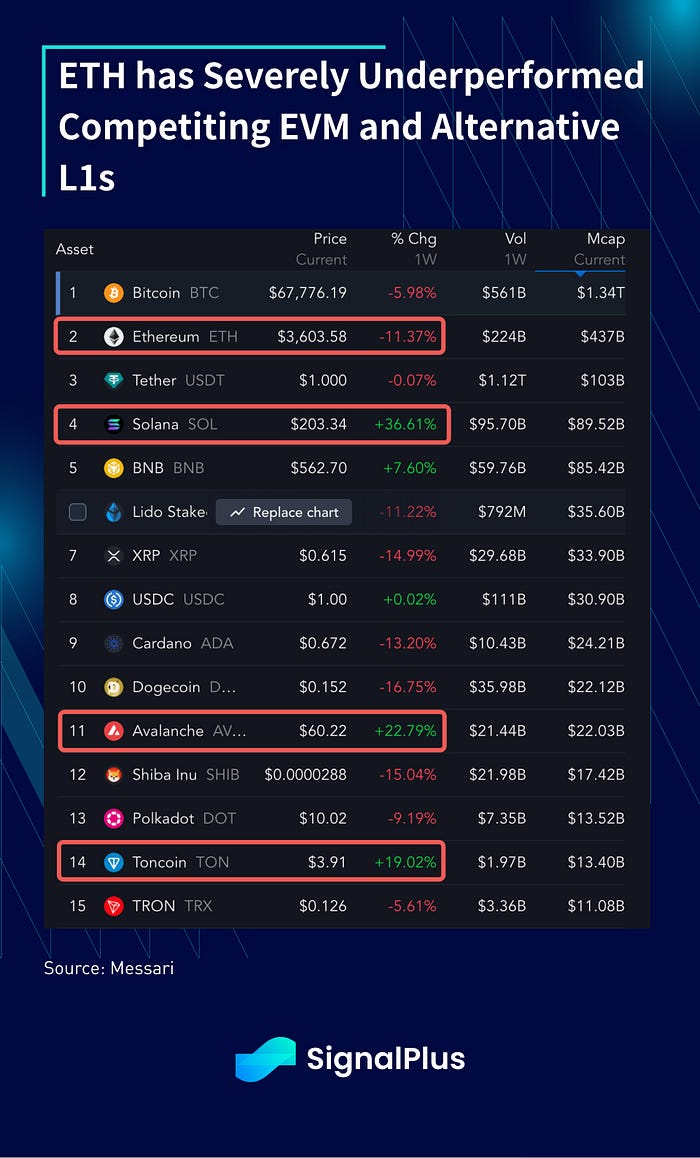

Furthermore, outside of BTC, Ethereum continues to struggle especially against the likes of other major EVM and L1 chains, most notably against Solana / Avalanche / TON. With the base ETH narrative being somewhat crowded out by the focus on the various L2 layers, attention is also diverted to burgeoning network activity of the EVM competitors (via memecoins and non-ETH ETSs) and the upcoming Telegram equity IPO (which supports TON as the native token). A failure for the SEC to approve ETH ETFs is another a non-trivial risk for us ahead, and we remain cautious on the former TradFi favourite in the near future.

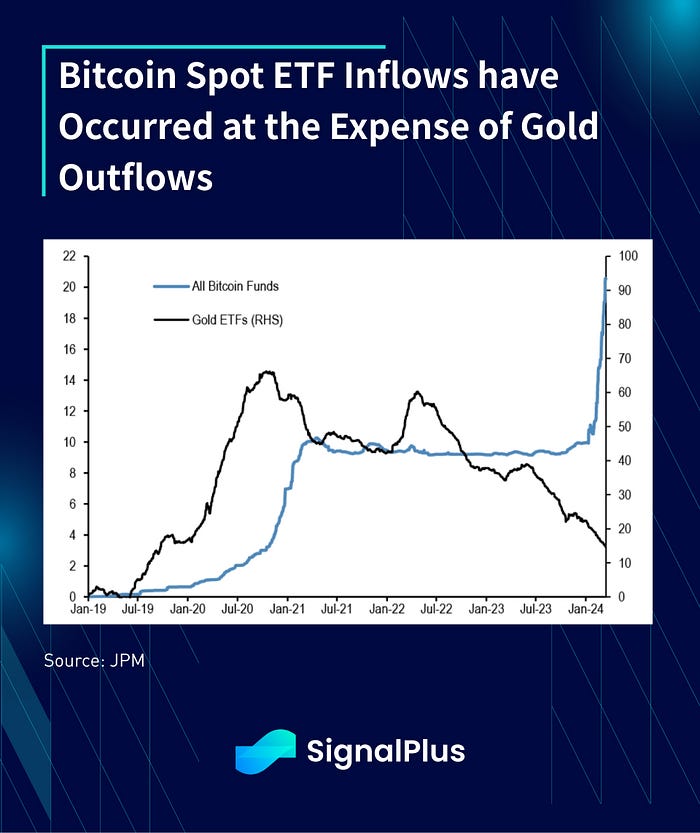

Finally, JPM cited an interesting observation where BTC ETF inflows have been taking place at the expense of Gold ETF outflows, true to Bitcoin’s long-held moniker as ‘digital gold’. Despite that, spot Gold has still managed to trade to all-time-highs in-line with crypto and equities, albeit to a less impressive return. Would spot Gold prove to be a safe haven should both equities and crypto see a risk-off adjustment in the rest of the year head? Furthermore, previous instances where gold and equities htraded to cycle-highs in-tandem have preceded significant risk-off events back in the early 1980s, 2007, and 2020. Will history repeat itself once again? Definitely something to keep an eye on…

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments