(Today’s commentary will be an abbreviated version with US markets closed for holidays)

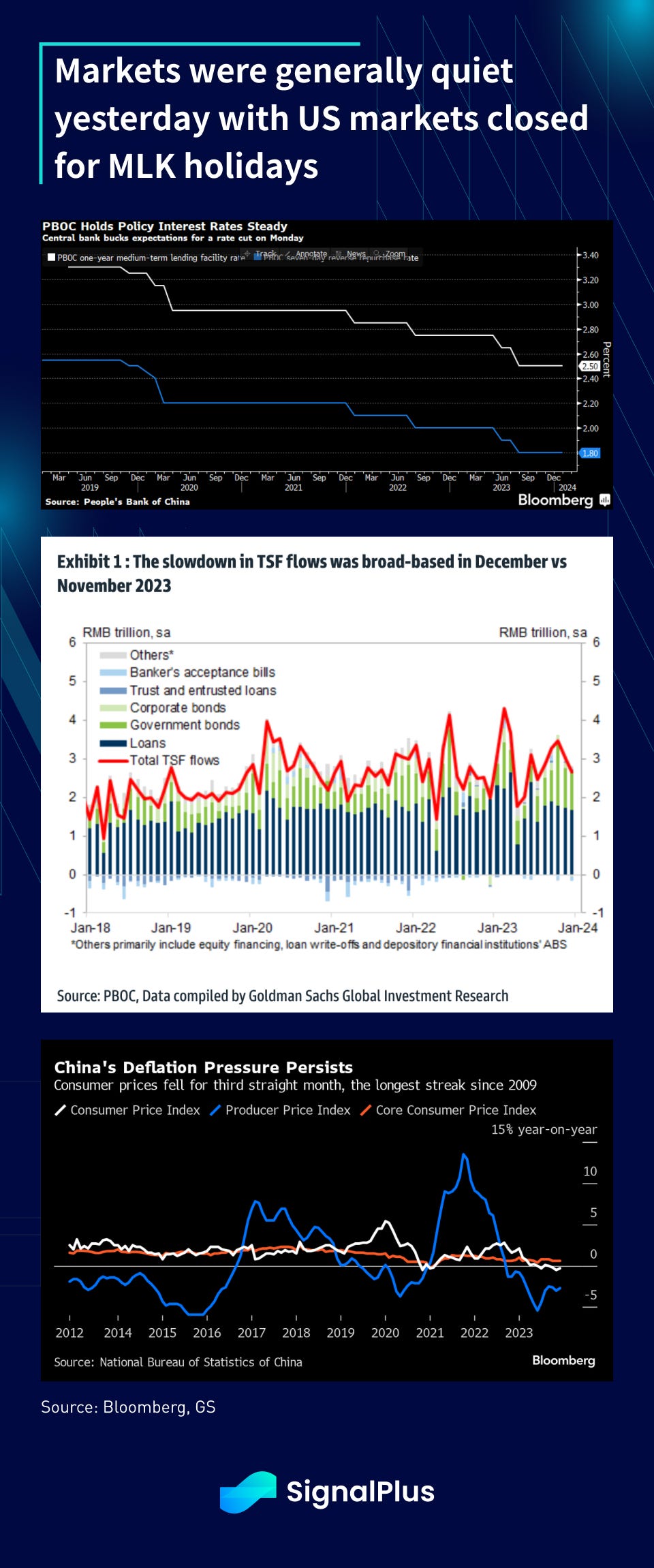

Markets were generally quiet yesterday with US markets closed for MLK holidays. The Asia session started with another China disappointment as PBOC surprisingly kept their MLF rates unchanged this month. Despite a worsening slowdown in TSF led by softer bank loans, and both CPI and PPI now firmly in deflationary territory. China stocks continue to lag world

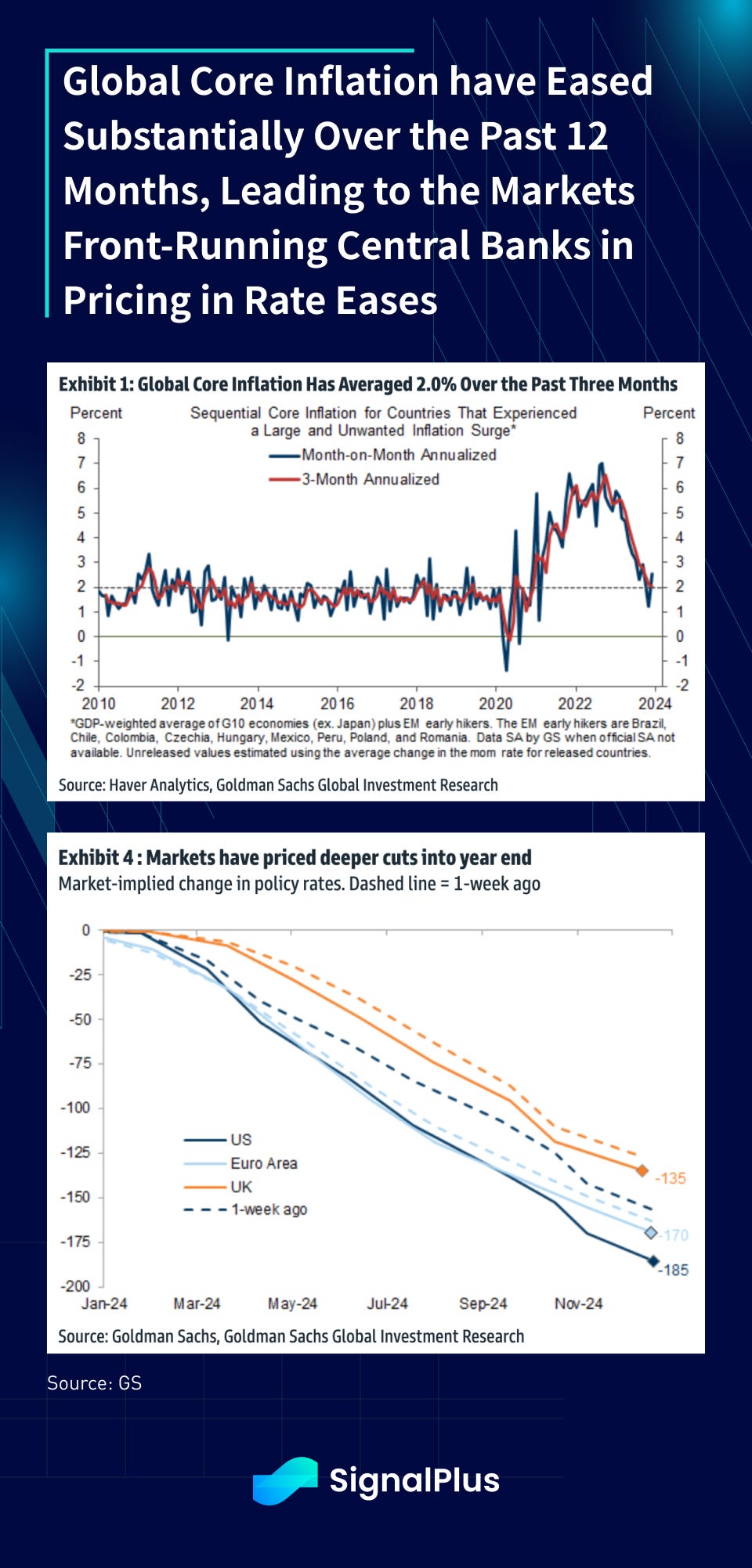

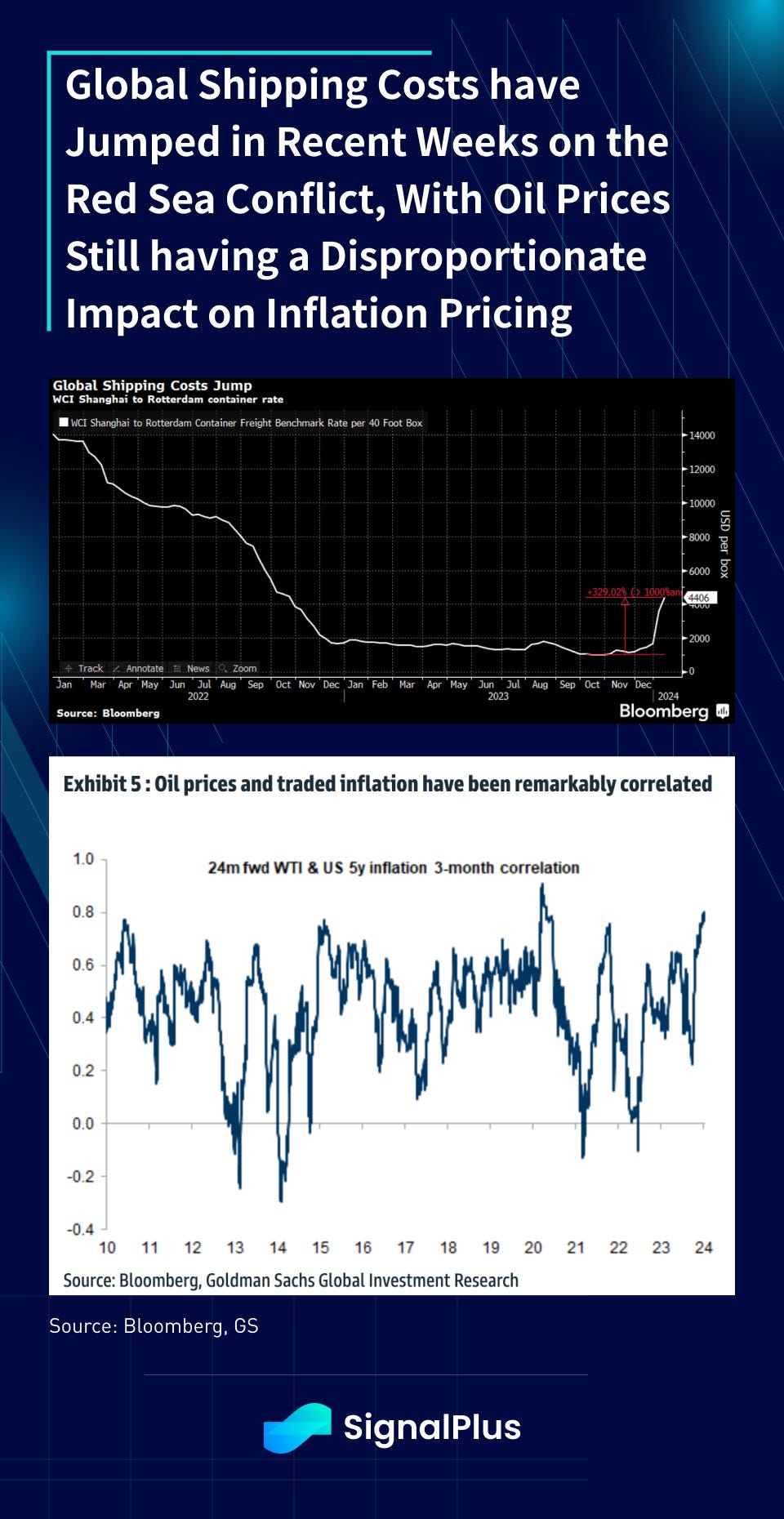

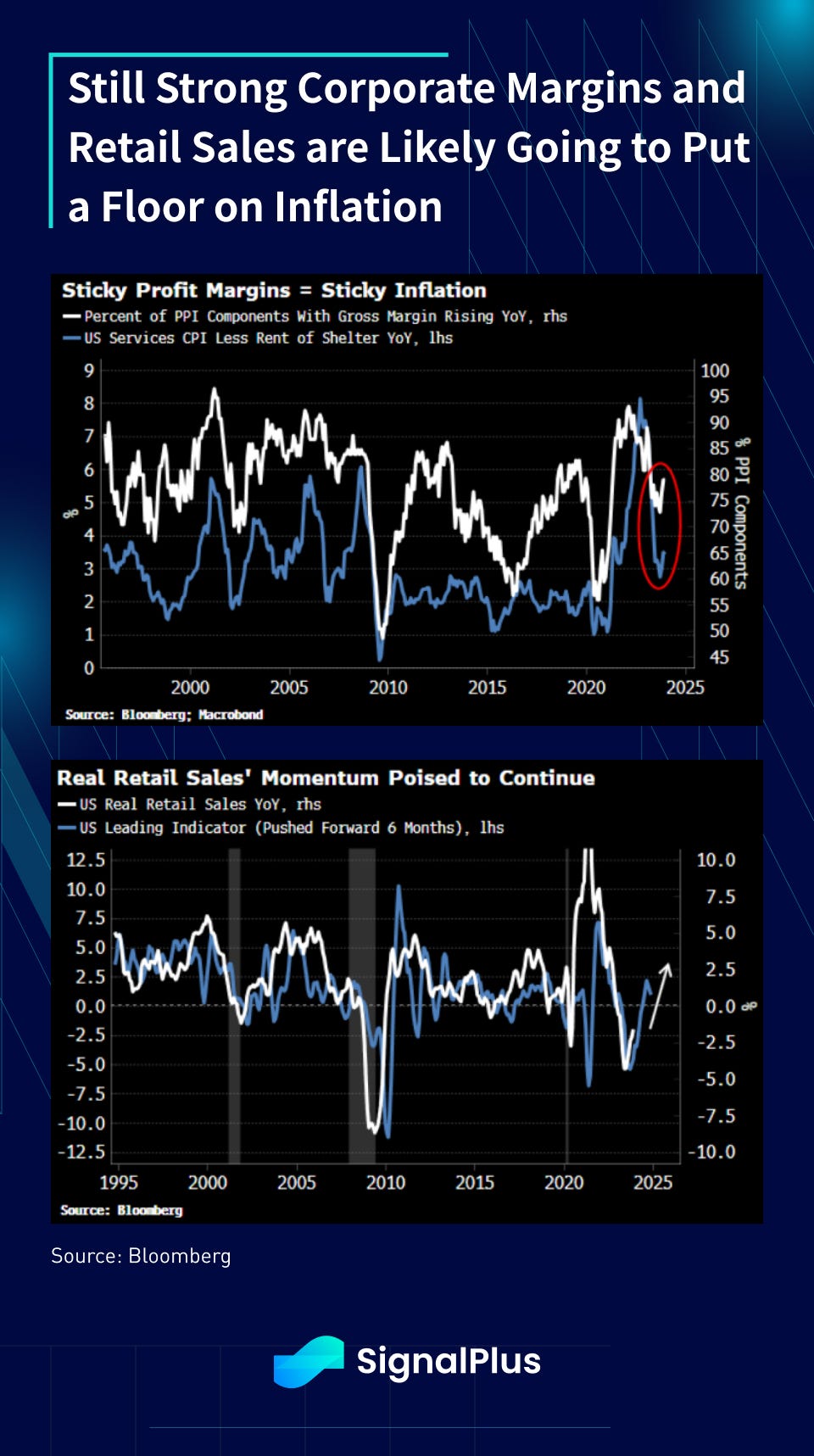

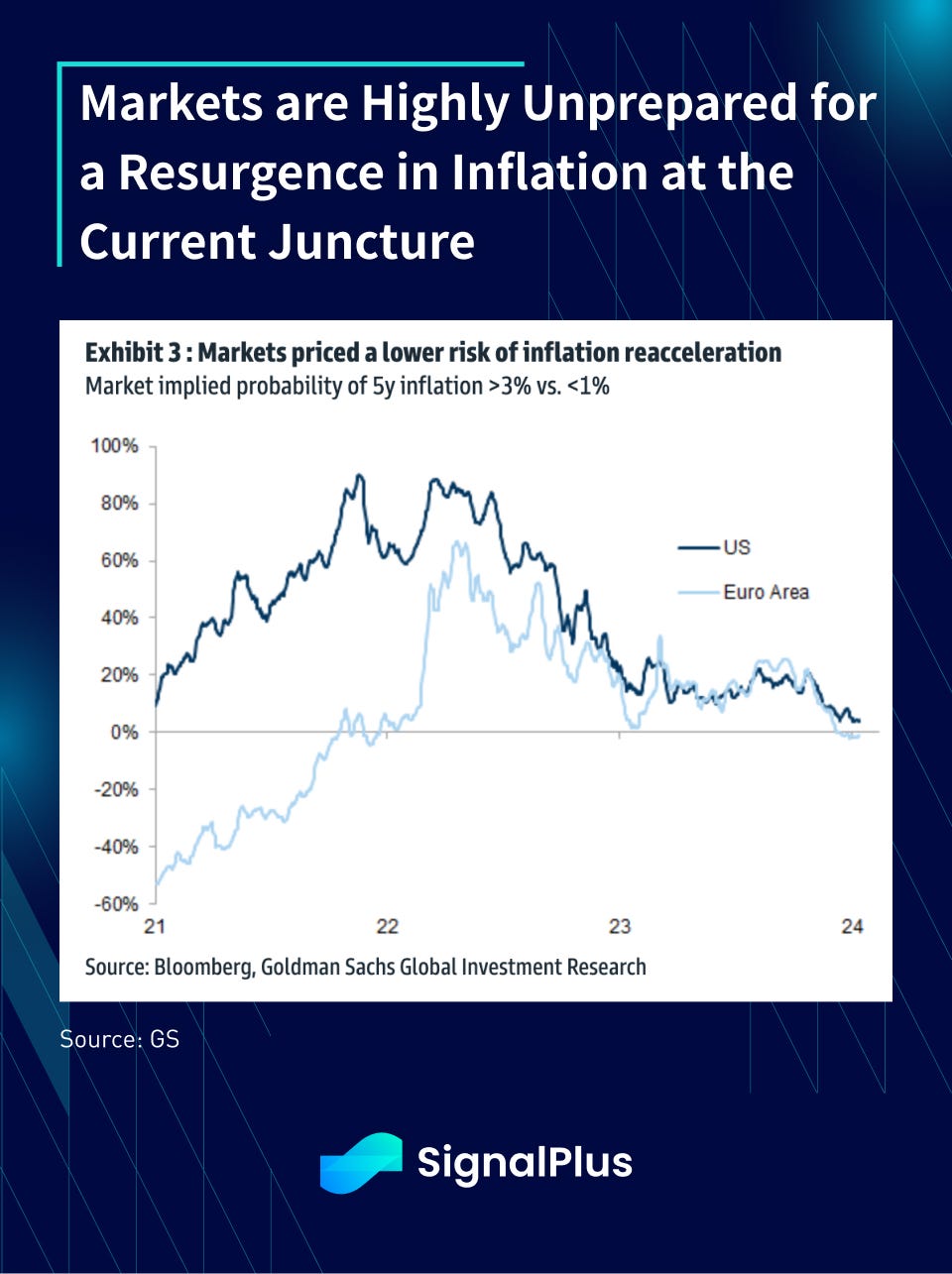

Speaking of disinflation, global core inflation has come down substantially since 2022–2023, averaging 2% based on GS estimates. Markets have not let this go unnoticed, pricing in an increasing amount of rate cuts through 2024 and pushing central banks deeper into a corner to ease. However, this over-zealousness is coming at a time when global shipping costs have started to jump due to the Red Sea conflicts, with oil’s correlation to inflation pricing staying near record highs. Furthermore, sticky corporate profit margins and still healthy retail sales will likely keep a floor on how low price inflation can go, just as markets are the least prepared for an inflation resurgence at this point. Something to keep in mind as we head further into 2024.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments