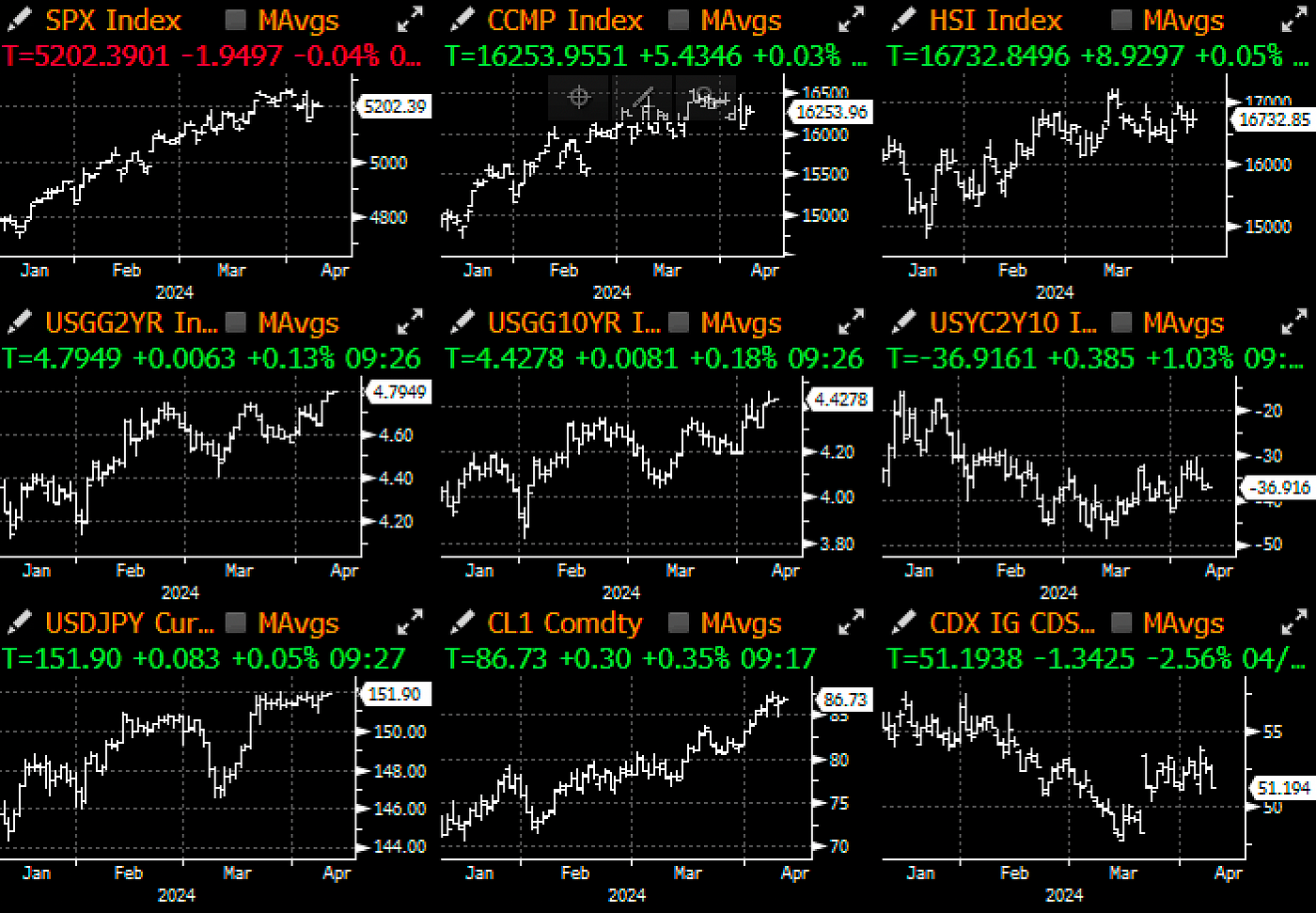

A quiet session yesterday gave markets a short break ahead of what is otherwise a very busy data week ahead. China will see the release of new yuan loans, aggregative financing, and M2 money supply, CPI, PPI, and trade balance. Europe will see the release of German industrial data, lending surveys, Sweden and Norway CPI, and of course the ECB meeting. UK will see the release of labour jobs data, monthly GDP, and industrial production. US data will see a large focus on prices with the release of NY Fed’s 1yr inflation expectations, CPI, PPI, UMich consumer confidence and inflation expectations on the docket. Central bank events will include rate decisions from Singapore, Sweden, New Zealand, Canada, Thailand, ECB, and Korea. We’ll end the week with the start of Q1 earnings reports out of JPM, Citi, Wells Fargo, State Street, and BlackRock. A very busy week indeed!

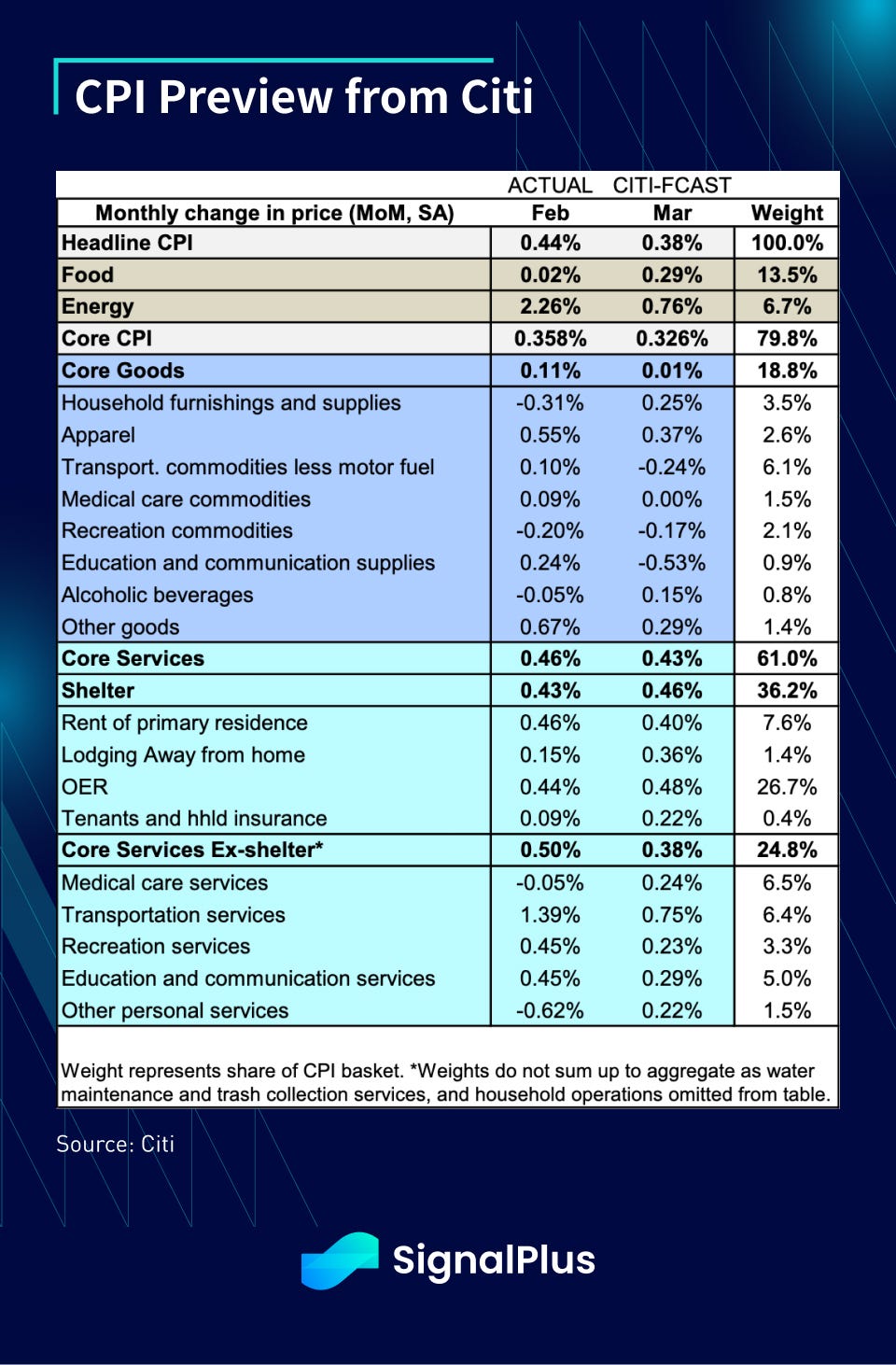

Over in the US, the big focus will be on Wednesday’s CPI where the street expects a slight drop in core CPI from 3.8% YoY back down to 3.7%, with markets likely better hedged for a hawkish surprise judging from the upward move in bond yields over the past few days. Options straddles are implying for the SPX to move around +/- 1% on Wednesday, with the index moving an average of +/- 0.7% on CPI days over the past 12 months. Keep in mind that option implieds have generally overpriced realized moves over the past 2 years, as investors have been paying up for tail protection given the immense focus on inflation over this cycle.

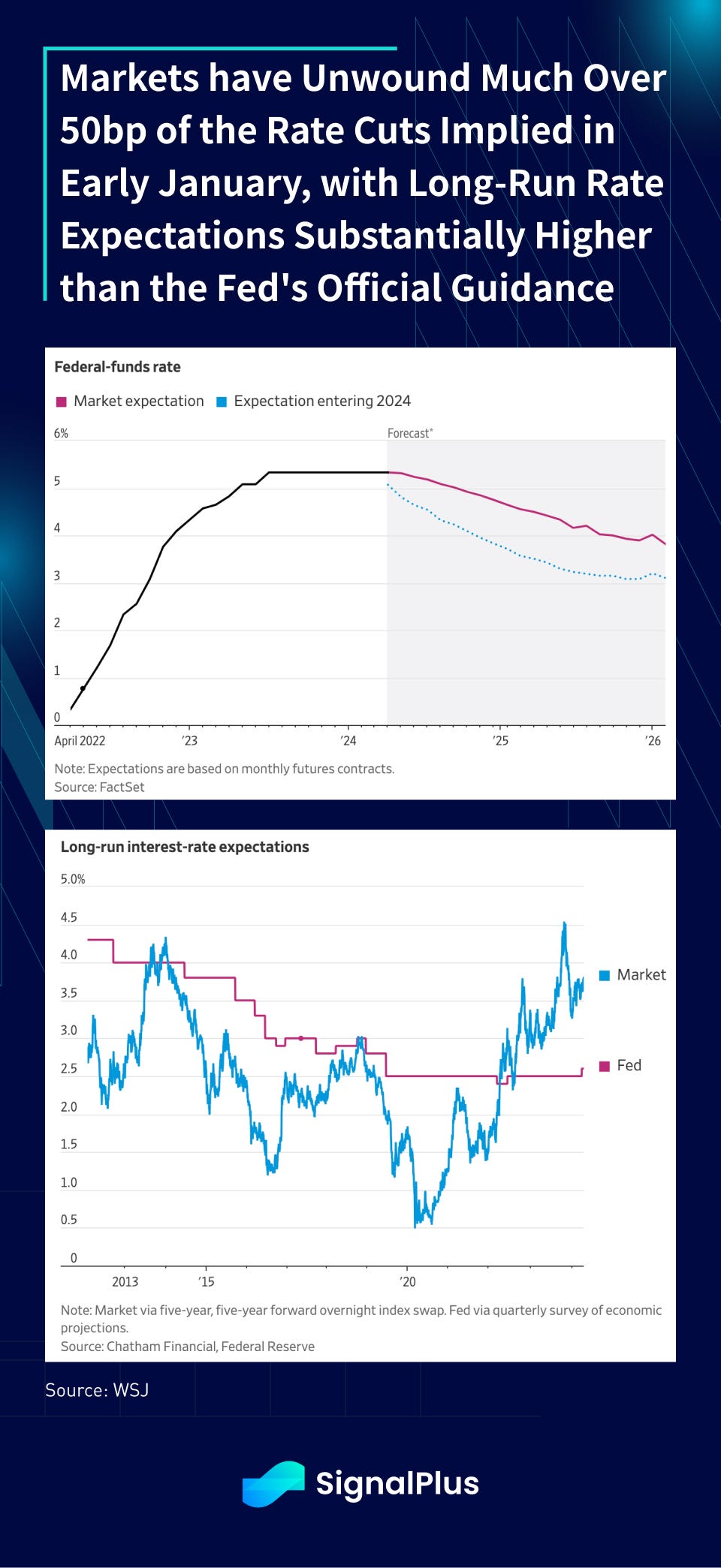

The fixed income market has fully bought back into the “higher for longer” mantra on rates, with markets pricing out well over 50bp of implied rate cuts compared to early January, and both 2yr yields and long-term rates are now pricing substantially higher levels than the Fed’s official guidance.

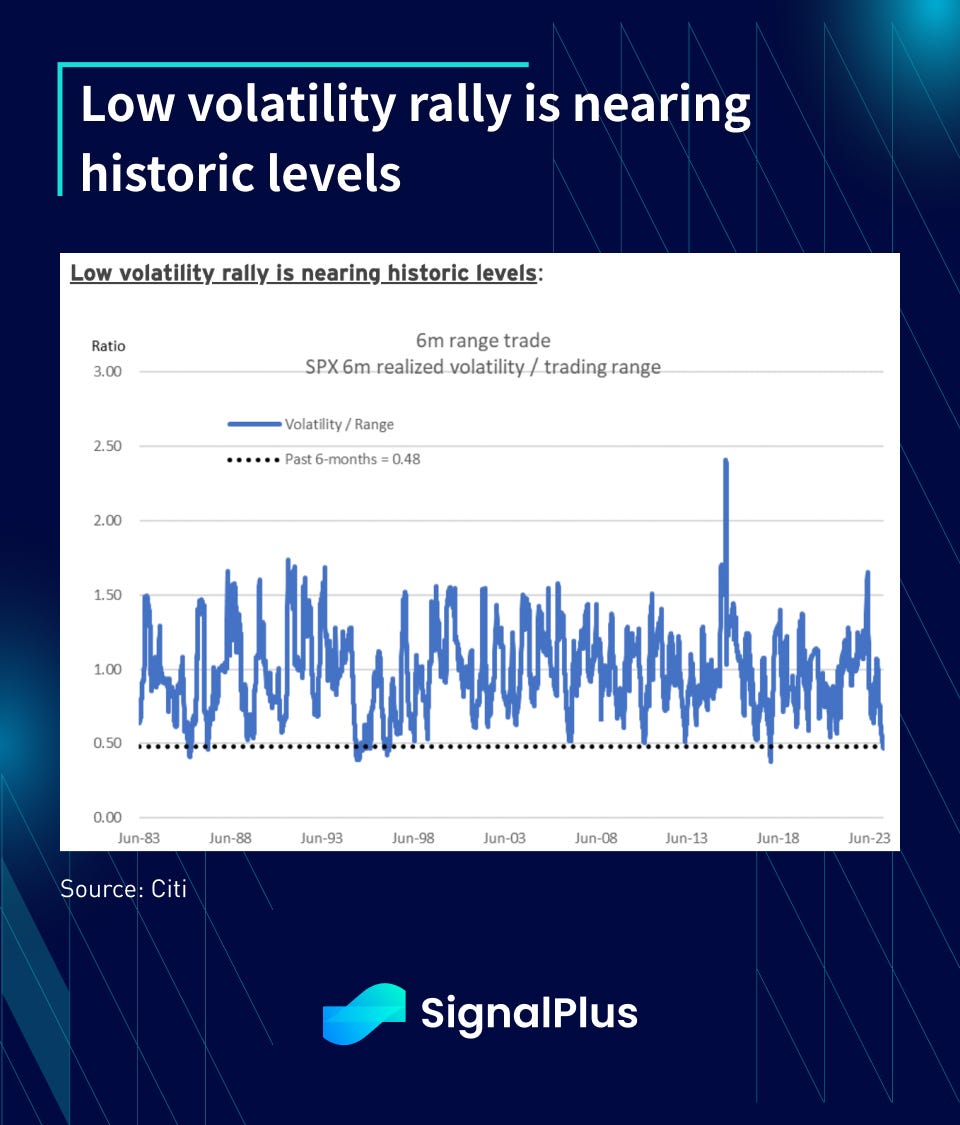

Speaking of volatility, Citi reports that the SPX has rallied 23% in the past 6 months, with a max/min trading range of 24.4%, and realized volatility stuck at trough levels at just 11.7%. The ratio of volatility to trading range is at the lowest level since January, and at the 1st percent-tile since 1983. Implied correlation has also fallen to decade lows as macro event risks have all but dissipated, signaling high (extreme?) levels of risk-complacency, with both economic performance and corporate earnings firing on all cylinders.

Said in another way, the SPX hasn’t had a -2% day since Feb 2023 (whereas BTC appears to have 2% moves every 8 hours these days), the 12th longest streak since 1928 according to data compiled by Citi. In context, the longest streak was >900 days between 2005 and 2008, though the complacency in US equities certainly stands in sharp contrast with current world affairs.

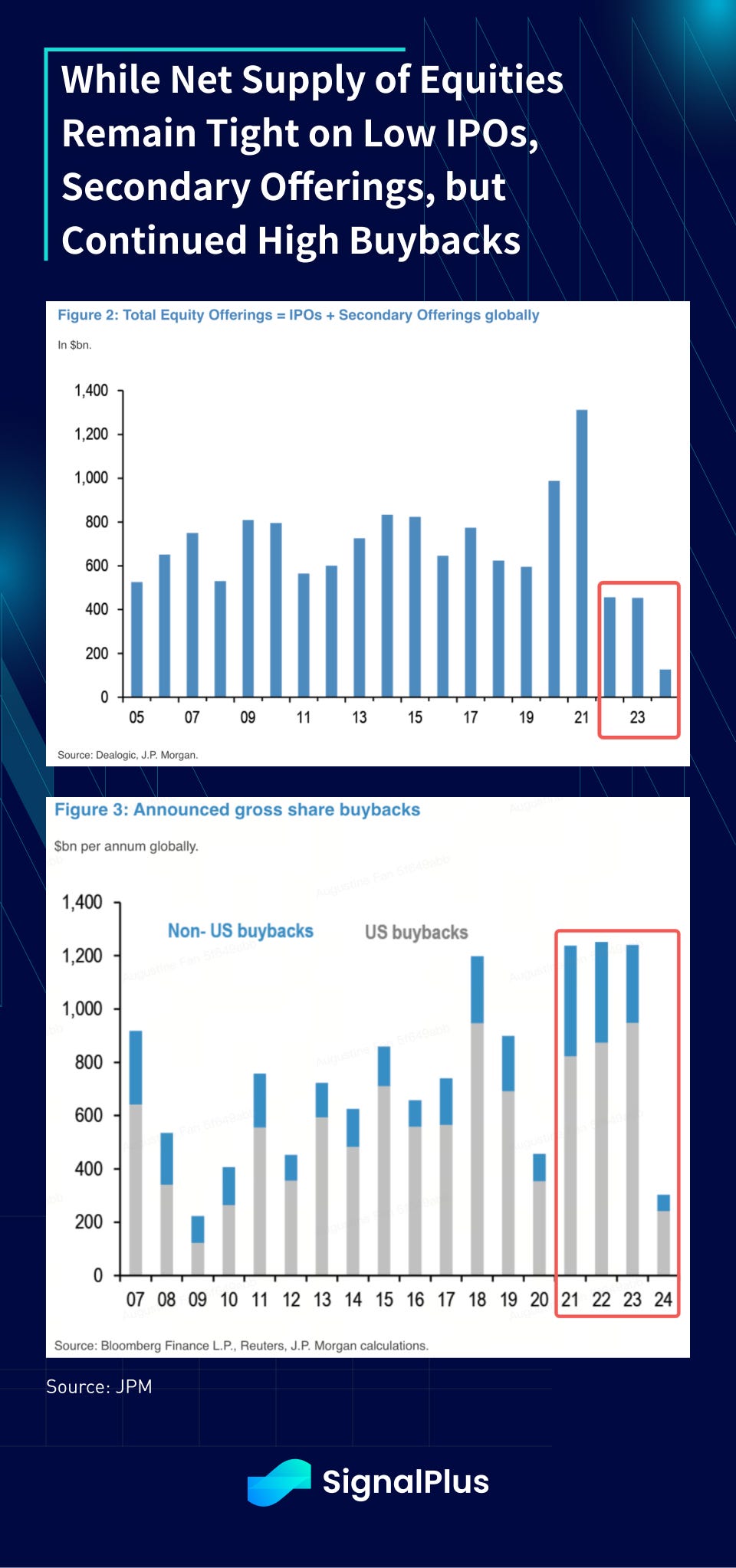

With that being said, from a bottom-up perspective, equities continued to be supported by robust earnings growth and corporate margins staying at historically high levels. Furthermore, the net supply of equity (secondary offerings + IPOs) continues to shrink versus years past, while buybacks have remained strong with 2024 looking to be the 4th consecutive year with ~$1.2 trillion in annual buybacks. It would appear that scarcity doesn’t just apply to Bitcoin only, but the supply of good stocks also appear to be in short-supply against the ever expanding fiat denomination base.

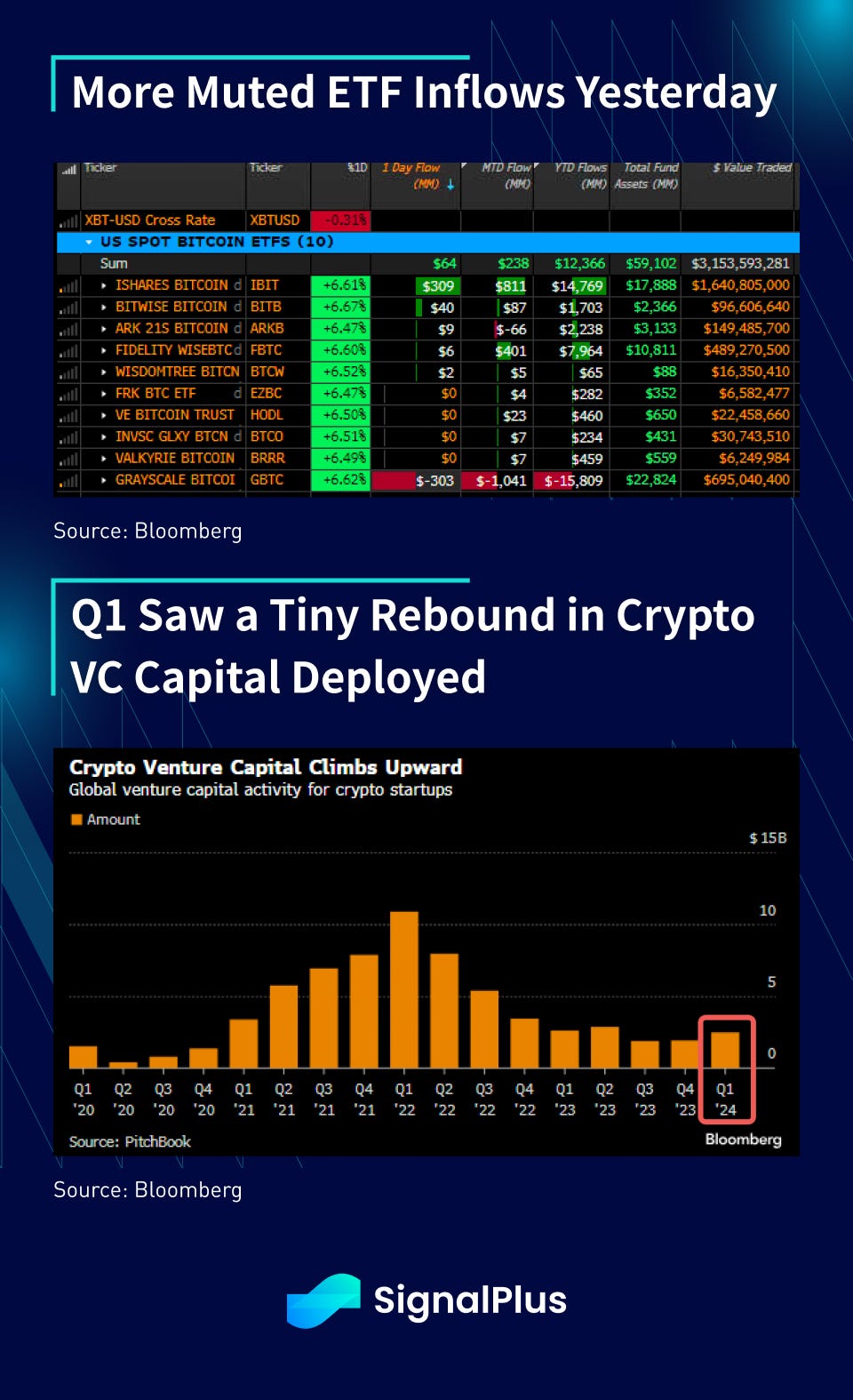

Crypto prices continued their rebound ascent after washing out leveraged longs in the past week. Prices are just a whisker away from all time highs as different altcoins continue to rotate and enjoy their day in the sun. ETF inflows were more modest at $64M yesterday, with BlackRock inflows basically matching GBTC outflows. Finally, Bloomberg reported a small rebound in crypto VC capital deployed in 1Q24, a good sign to see but still a far cry from 2022 despite Bitcoin prices having retraced back all its losses.

What will it take to FOMO VC capital back into the crypto space in the next quarters? SignalPlus is working hard with the other crypto builders to hopefully develop that killer use-case to bring the investment excitement back. Stay tuned!

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments