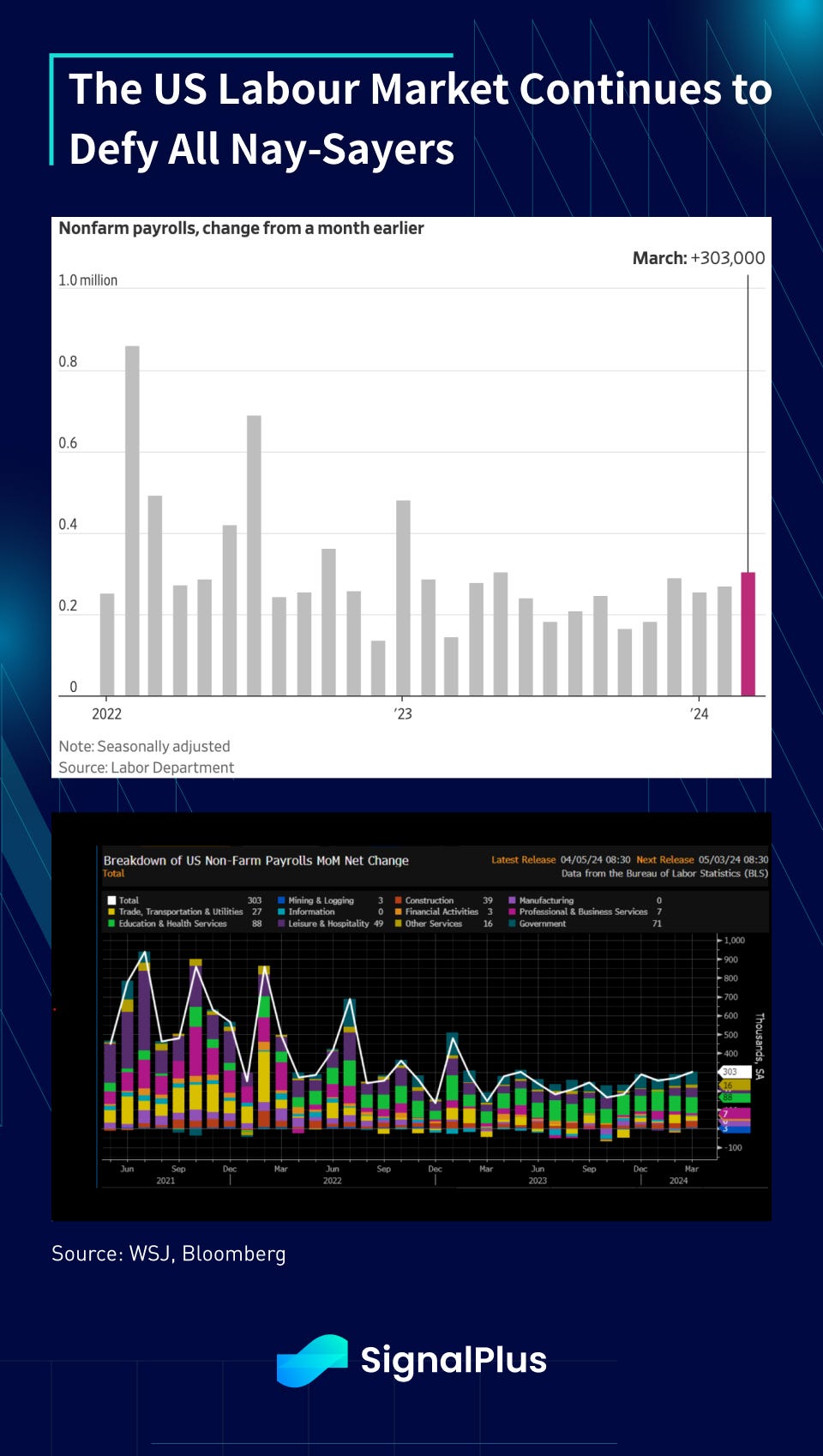

Another strong NFP report on Friday continued to show a US labour market that defies all odds, with a significant beat in headline (303k vs 214k), a 22k upward revision, leading to a 3-month average at a very healthy +276k. The unemployment rate was back down to 3.8% vs a brief rise in February, while average hourly earnings rose to 0.3% vs 0.2%. Wide spread strength was seen across education, health, leisure, hospitality, and goods sectors.

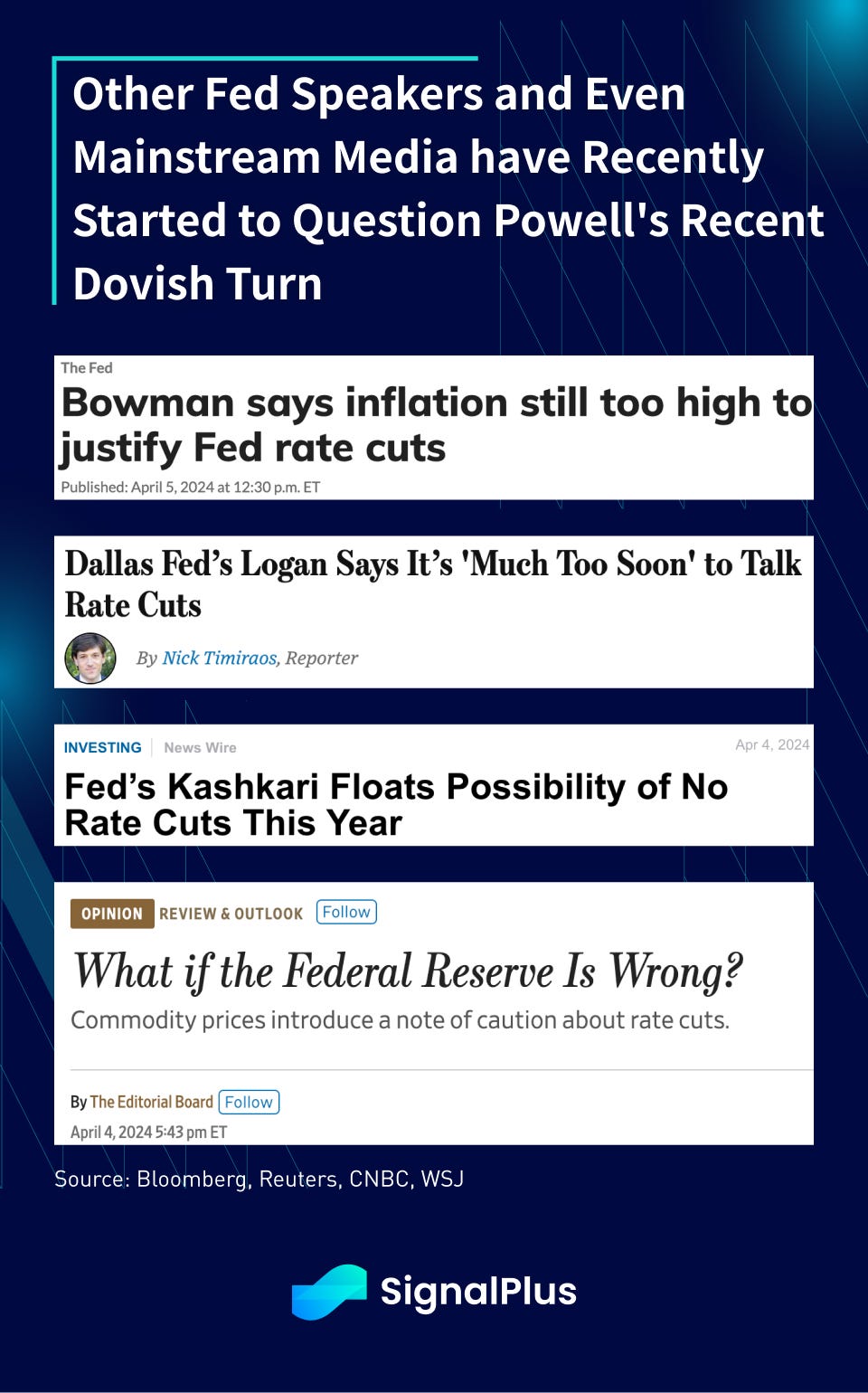

The latest resilience of the jobs data, along with the recent beats in global PMIs and reflation pressures via commodity price jumps, are setting up a rather contentious challenge against Powell’s dovish turn. So perhaps it’s no surprise that the ex-Powell Fed speakers have continued to offer some hawkish pushbacks:

- Richmond Fed Barkin: acknowledges “quite strong job report”, and “allowing time for clouds to clear” before “toggling rates down”

- Governor Bowman: “there’s a number of upside risks to inflation”, and the Fed’s pursuit of their inflation target has seen their progress “stalled”

- Dallas Fed Logan: “much too soon” to be making about rate cuts, due to “meaningful risks” to the inflation process.

- Minneapolis Fed Kashkari: “If we continue to see inflation moving sideways, then that would make me question whether we needed to do those rate cuts (2x) at all” and “if we have a run rate that’s very attractive, people have jobs, businesses are doing well, inflation is coming back down, why do anything?”

Even the WSJ just floated an opinion piece titled “What if the Federal Reserve is Wrong” given the spike in commodity prices. Are we going to see some mutiny and pressure within the Fed’s consensus for the first time in a long while?

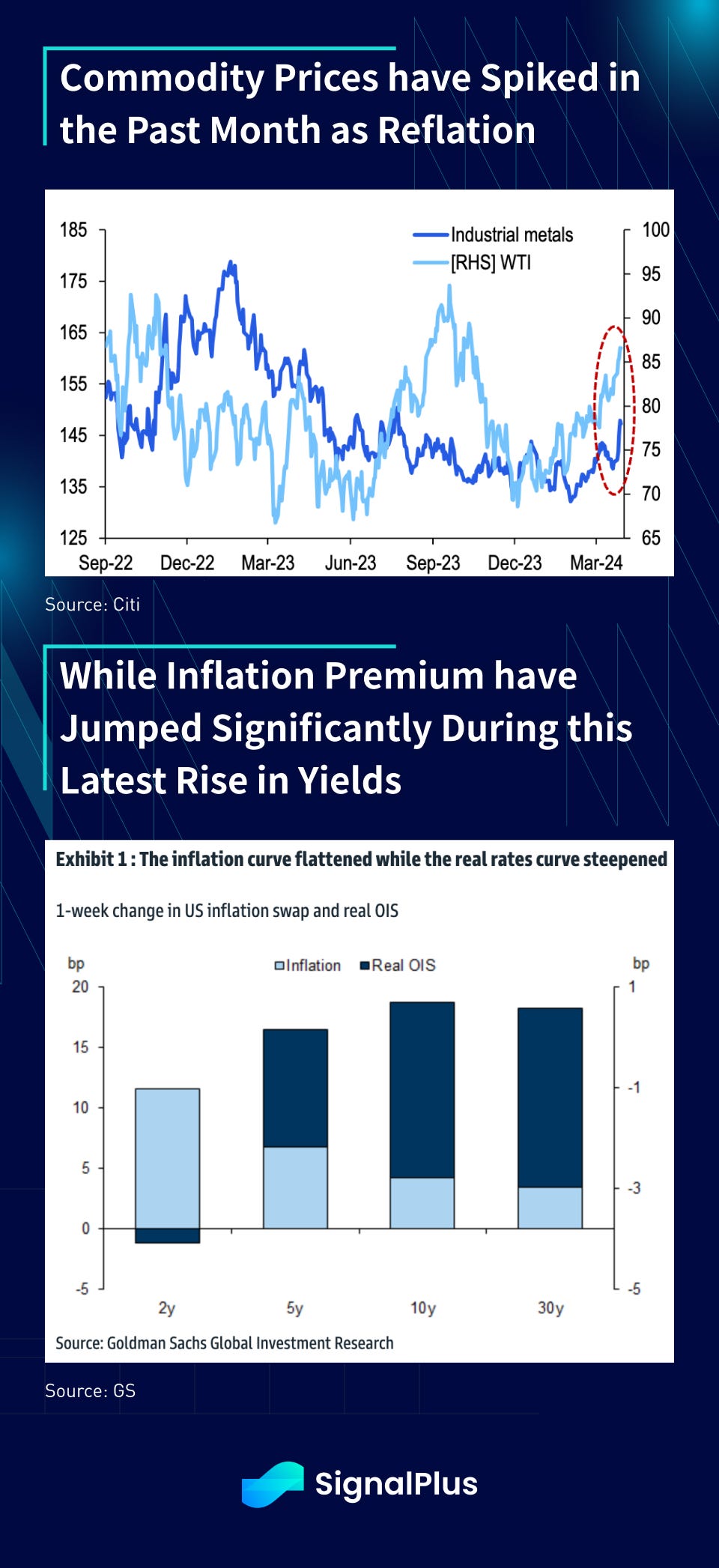

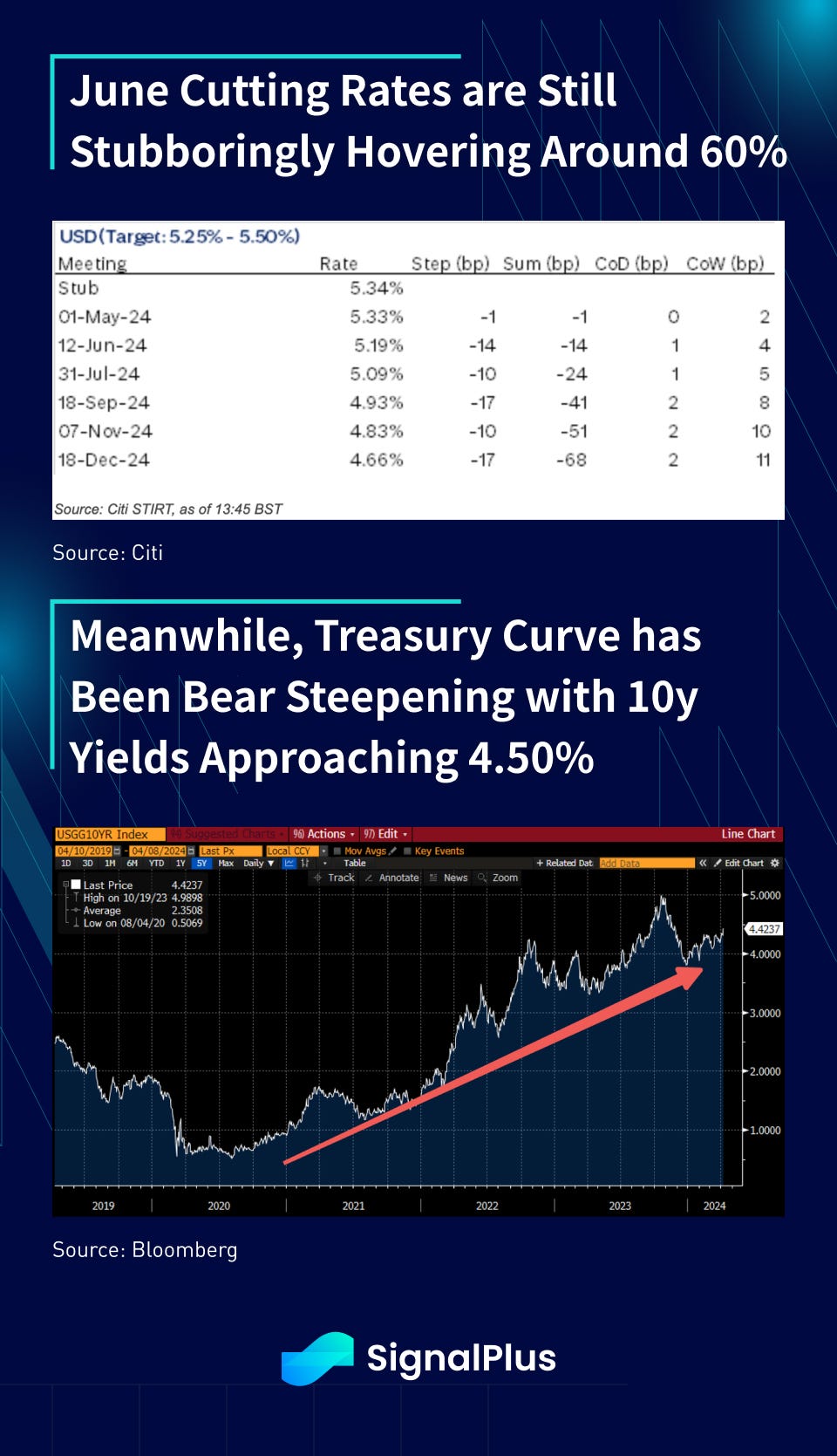

In the meantime, commodity prices have spiked with commodity prices seeing the largest weekly gain since nearly a year ago. Furthermore, long-end inflation premium have risen significantly during this latest rise in yields, as investors are starting to price in the risk of an inflation run-away with a Fed’s that has returned to its old ‘easy-money’ ways.

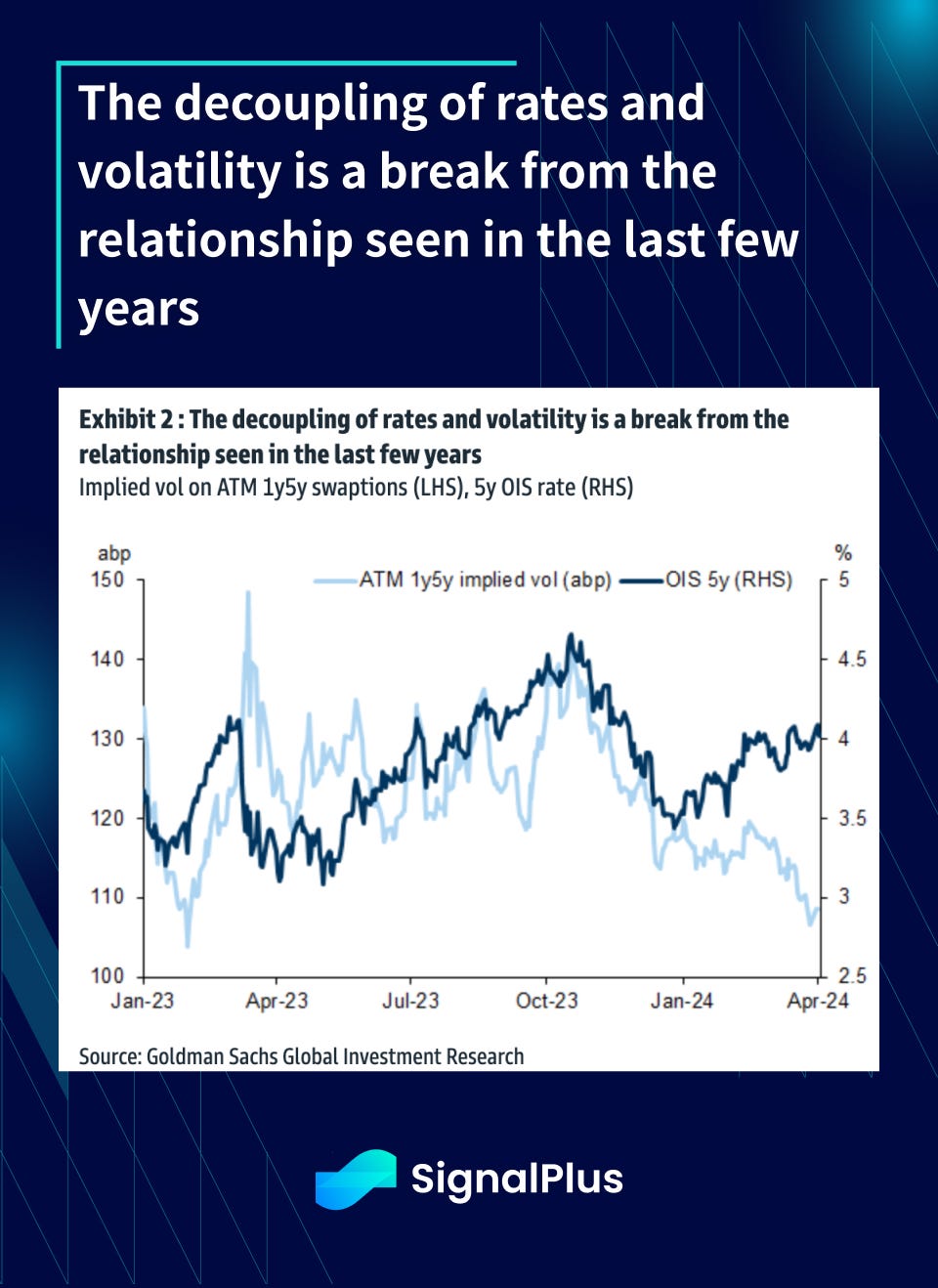

Meanwhile, June rate cuts are still around 60% odds, so the treasury curve has been bear-steepening with 10yr yields inching ever close to 4.50%. However, unlike Q3 of last year, this is happening against a backdrop of significantly lower rate volatility, signalling that investors are less worried about a rate-induced balance sheet accident (SNB blow up, UK-mini budget crisis, HTM portfolio losses etc) that it has been in recent past.

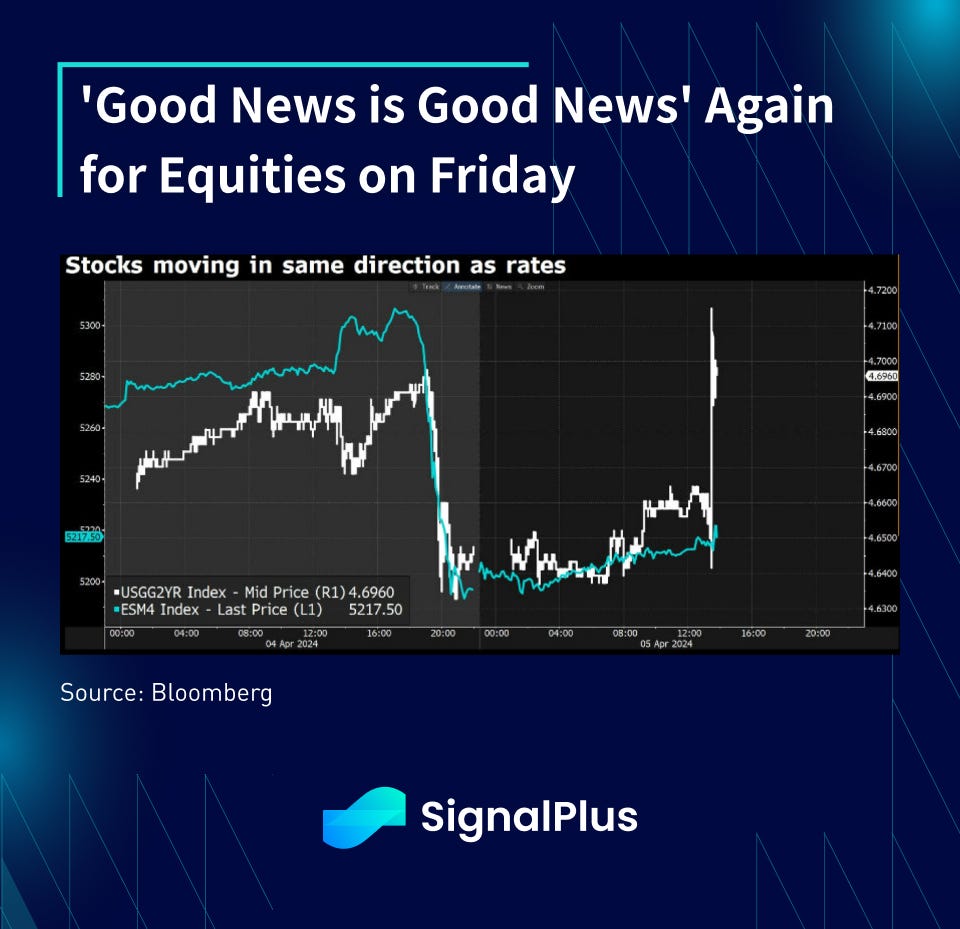

However, Implied Rate Volatility is Coming Down, Showing that Investors are Much More Sanguine About the Risks of a “Balance Sheet Accident’ from High Rates This Time Around

With investors being much more sanguine about rate risks, that has allowed equities to rally along with the rise in yields (+9bp on Friday), once again showing stock investors immaculate bullish adaptability to whatever might transpire (bad news = rate cuts, good news = good news). The risk-on party goes on for another day, at least until CPI later this week.

In crypto, prices have rebounded a fair bit with BTC approaching $70k with a lot of the levered-long futures positions being washed out last week, as evident with funding rates going back to long-term norms.

In the meantime, the dovish Fed and rally in commodities have kept Gold prices close to historical highs, continuing its longer term correlation with BTC. Spot ETFs resumed their inflows, adding 203mm on Friday and a net +12.6bln in inflows YTD.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments