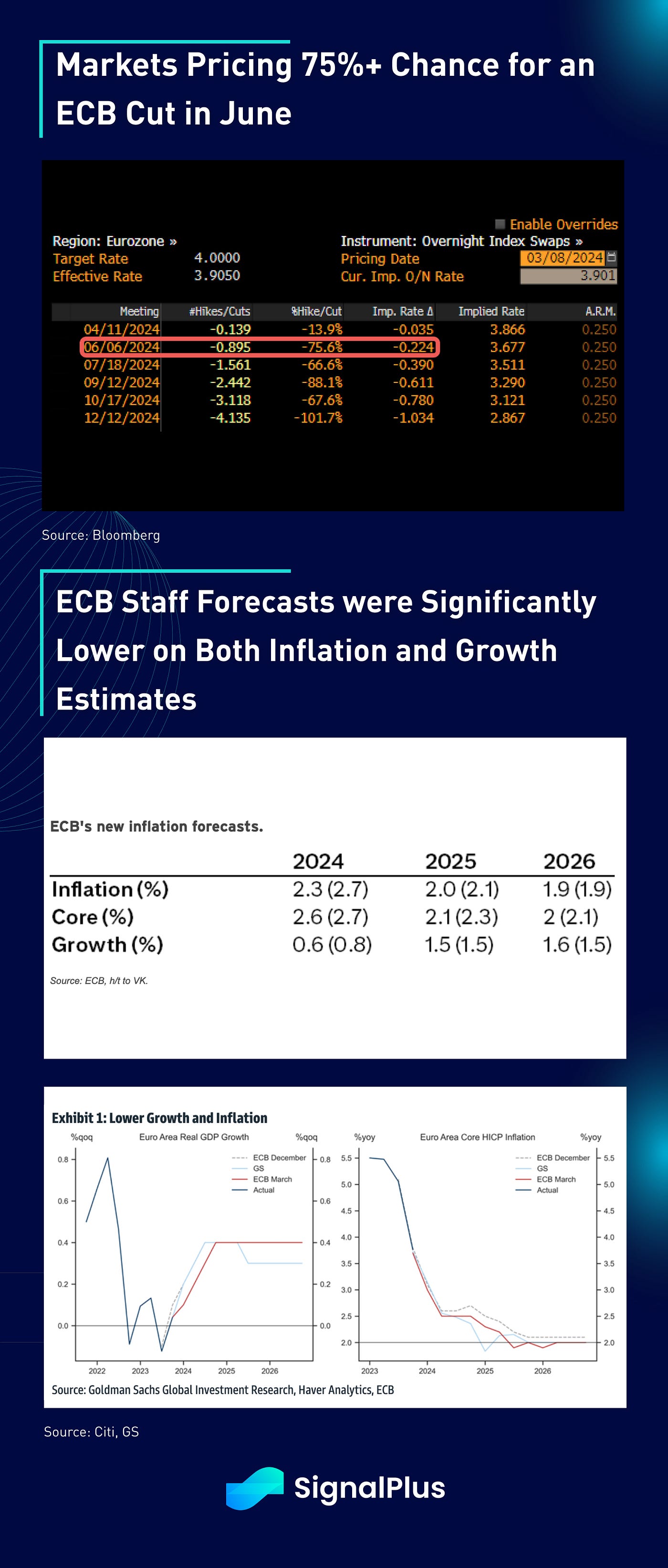

Despite keeping rates on hold, yesterday’s ECB projections showed significant downgrades to both growth and inflation, with 2025 price trends now approaching back to policy targets on both headline (2%) and core inflation (2.1%). While President Lagarde offered little on the upcoming pace of cuts, a healthy buffet of dovish headlines were sprinkled throughout the Q&A:

Some select dovish ECB press conference quotes:

- “Demand for labour is slowing”

- “There are signs that growth in wages is starting to moderate.”

- “Inflation is expected to continue the downward trend in coming months.”

- “Longer-term inflation expectations broadly stable around 2%.”

- “Risks to economic growth remain tilted to the downside.”

- “We’re making progress in disinflationary process.”

- “We’re more confident about hitting goal, but not sufficiently confident.””We will not wait until we are at 2% to make a decision.”

As such, the setup is pretty much for a ‘skip’ in the March ECB meeting, while markets are pricing a >75% chance of a cut in June. As the ECB has rarely cuts rates ahead of the Fed, should we expect yet another synchronized easing as an early summer gift for the markets? It’s certainly shaping up to be that way!

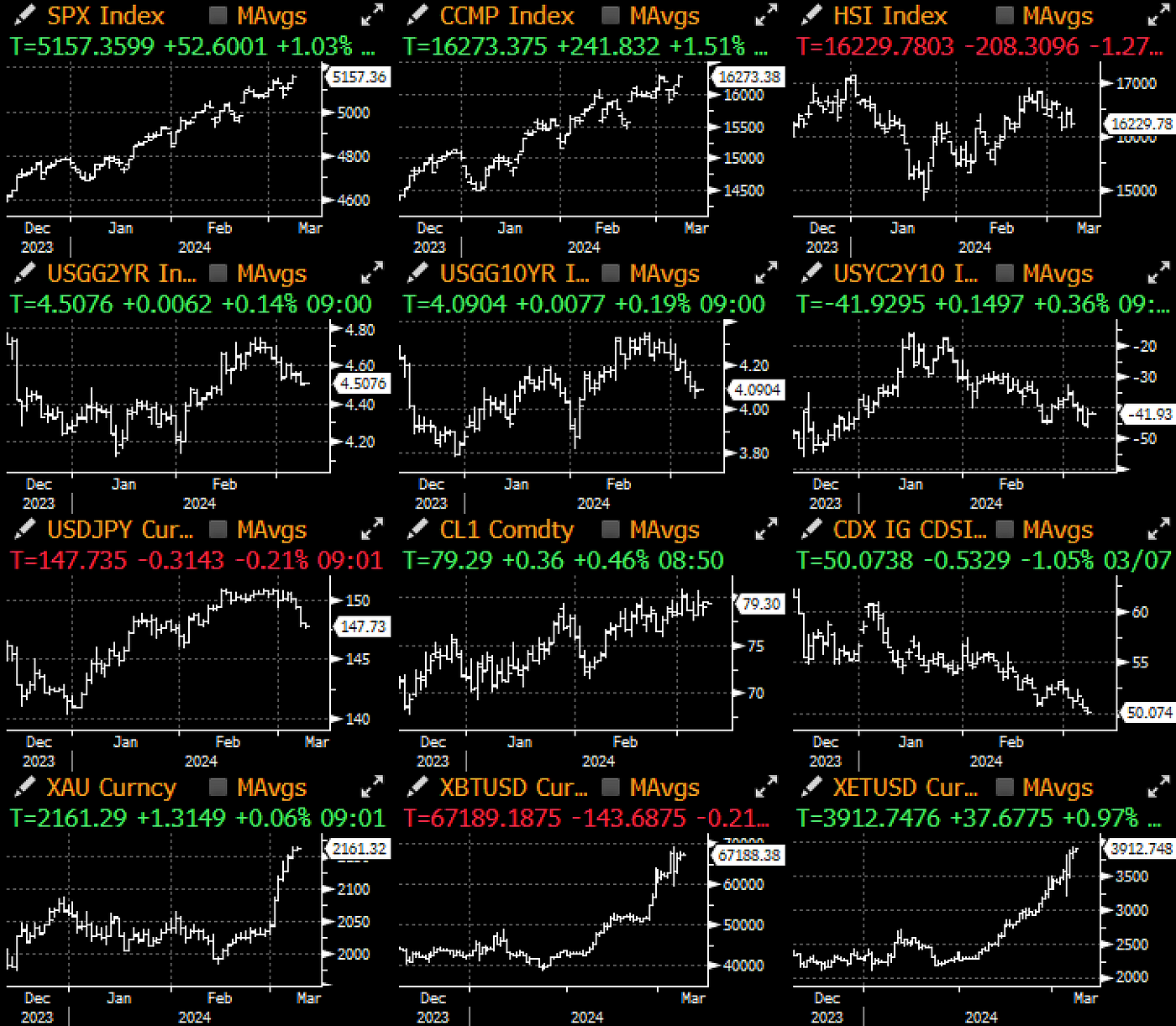

Risk assets certainly wasted no time to stage another rally with global bond yields falling thanks to the dovish ECB conference, while Fed’s Powell and Mester also both stated that it would be ‘appropriate’ to cut rates this year, as long as inflation continues on its current downward trend.

In equities, Euro Stoxx 600 hit a new record high thanks to ECB and chip-equipment manufacturer ASML powering the index with its own record close. In the US, the Nasdaq rallied by 1.5% and the SPX by 1%, driven by the usual culprits. Nvidia’s GTC conference on March 18–21 could be the next event market for AI and tech stocks later this month, though it appears to be a matter of time before the chip giant catches up to Apple on a market cap basis.

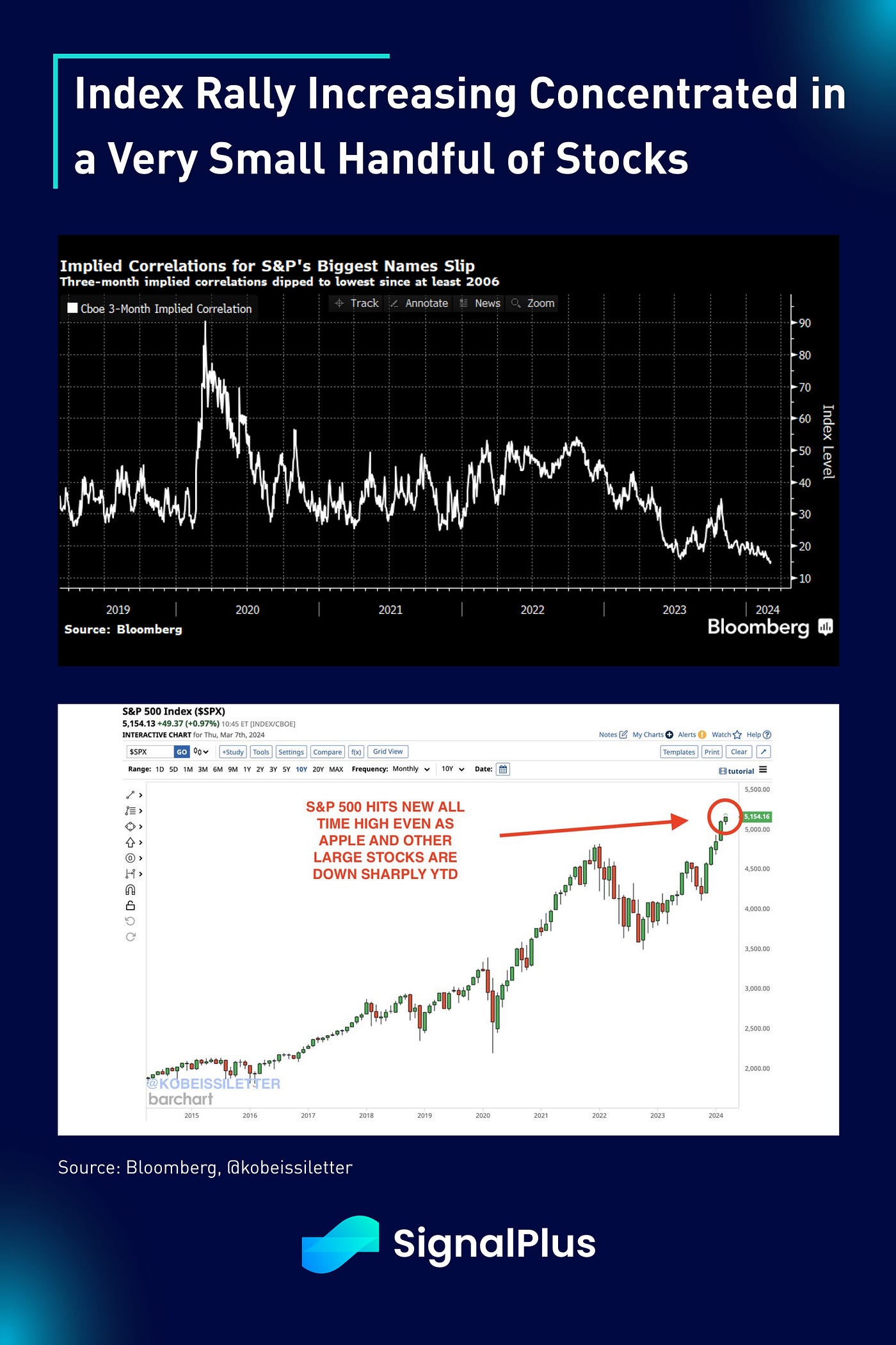

In terms of stock-picking ‘alpha’, implied correlations for the SPX bellweathers have dropped to near record lows, reflecting an index that is increasing depending on a tiny handful (or just one?) of stocks. Said another way, ‘Ride or Die’ with AI? The market isn’t leaving us with a lot of good options.

As risk sentiment heads back into the stratosphere, it’s only fitting Wall Street will be bringing back some of their favourite new toys to allow retail traders to hurt themselves very badly but within the sandbox of a very ‘regulated’ casino. For those of you that have been around, the SVYX ETF was one of the most popular ‘income ETFs’ which allowed investors to benefit from shorting volatility (VIX futures) within the confines of an ETF product. The ‘strategy’ saw a 250% return (with barely any drawdown) in 2017, before meeting its sudden demise over 48 hours (-95%) as volatility spiked suddenly in early 2018 (‘volmageddon’).

Never fear! After a few years of hiatus, Wall Street is back with similar ETF structures but in 0-DTE covered calls (same day options) as income generating strategies. Who wants to take bets on when this extends to out-right 0-DTE vol harvesting or in levered forms?

Speaking of options, the SEC (expectedly) delayed their approvals of the BTC ETF Option filing, which was filed by the likes of Nasdaq and CBOE. The final deadline will be on April 24 for the agency to either approve or deny these crypto ETF options, but we believe that it’ll just be a matter of time before options enter the fray to add another risk dimension to crypto markets. As always, the SignalPlus platform is here and ready for all your crypto options needs, so you can be well ahead of the curve!!!

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments