We start the Asia morning with a much hotter than expected labour cash earnings release out of Japan, which been a recent of interest as local media reported that one of the BoJ members has suggested that the Bank should end its NIRP as early as March, instead of waiting for April. Japan’s biggest trade union will announce the results of its annual wage negotiations out of March 15, which will no doubt factor into the BOJ rate decision to come just a few days later.

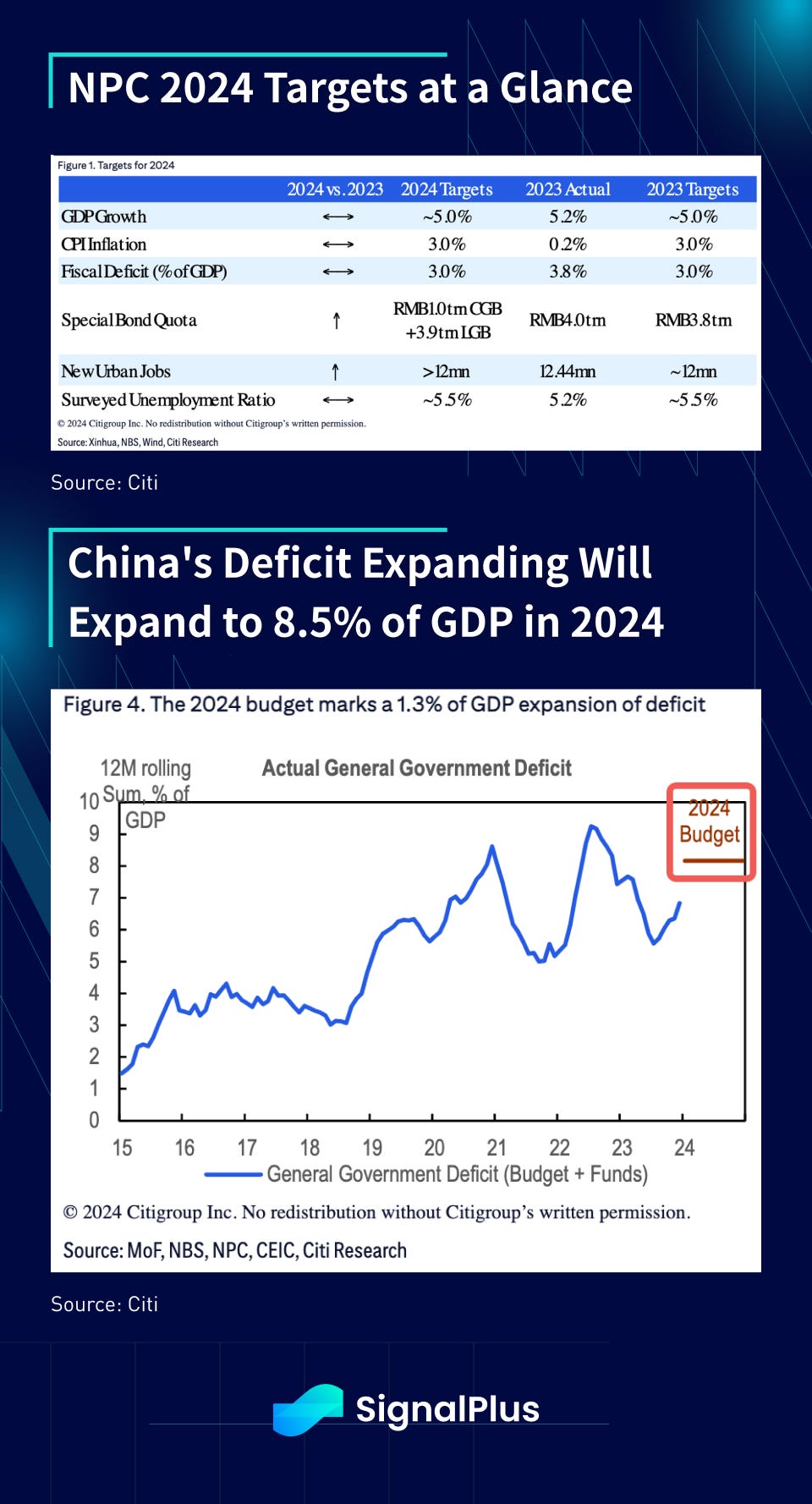

In China, the National People’s Congress is in progress this year, though the focus was on the Government Work Report out of the first day, which announced a growth target of~5% but with a stimulus package that underwhelmed market expectations. While the 5% GDP target was unchanged from last year, the absence of base effect benefits implies a 2yr CAGR of 4%+ in growth, which appears unlikely to be achievable without additional policy boosts. Policymakers announced a fiscal budget at 3% of GDP (RMB $4T), with an extra RMB$1T of ultra-long special government bonds (CGBs) as an extra stimulus, taking the total government deficit spending to 8.2% of GDP.

The CGB proceeds will continue to be earmarked for investment projects, rather than being any type of consumption handouts, disappointing market participants who were hoping for more robust measures to support the economic recovery.

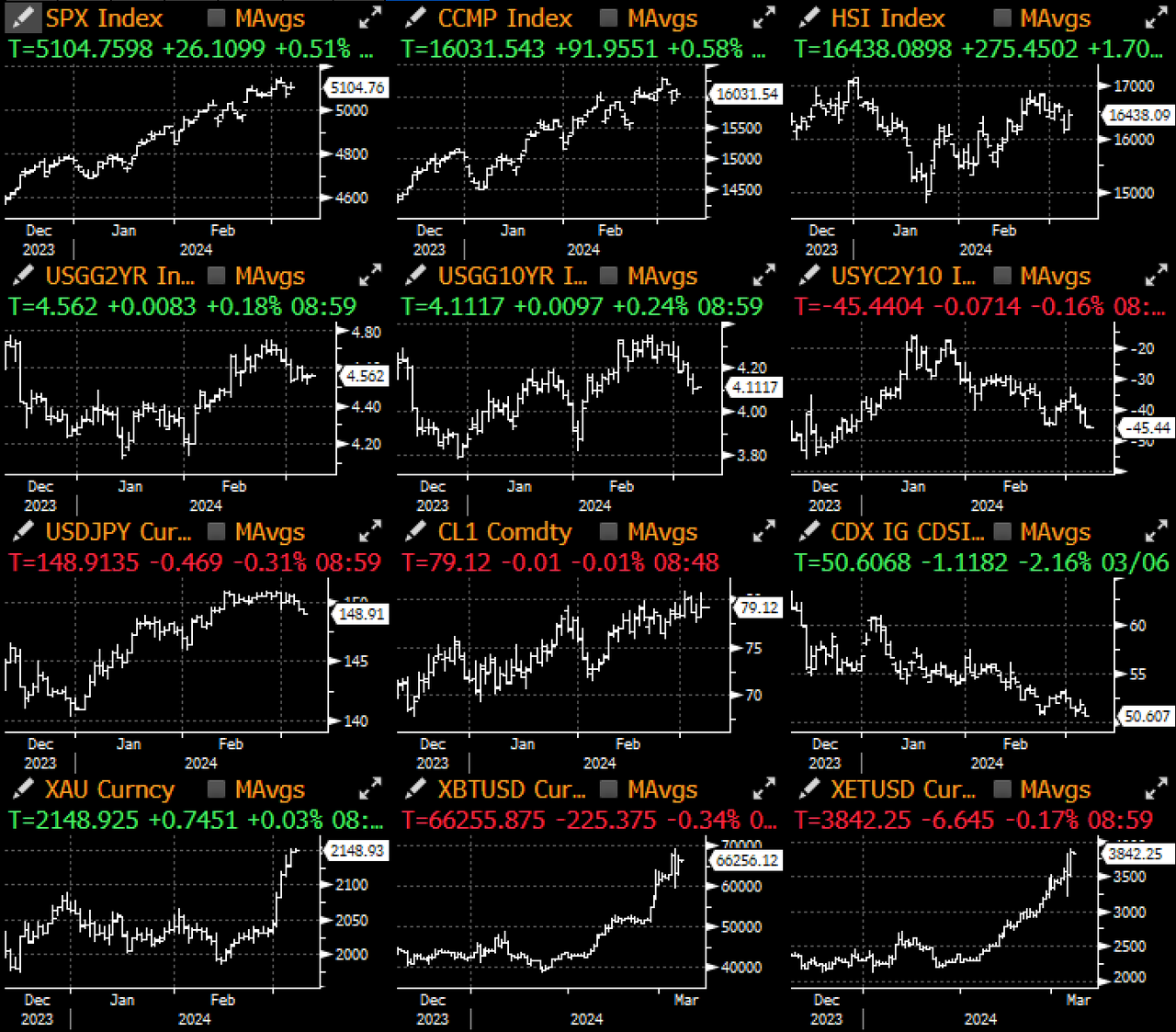

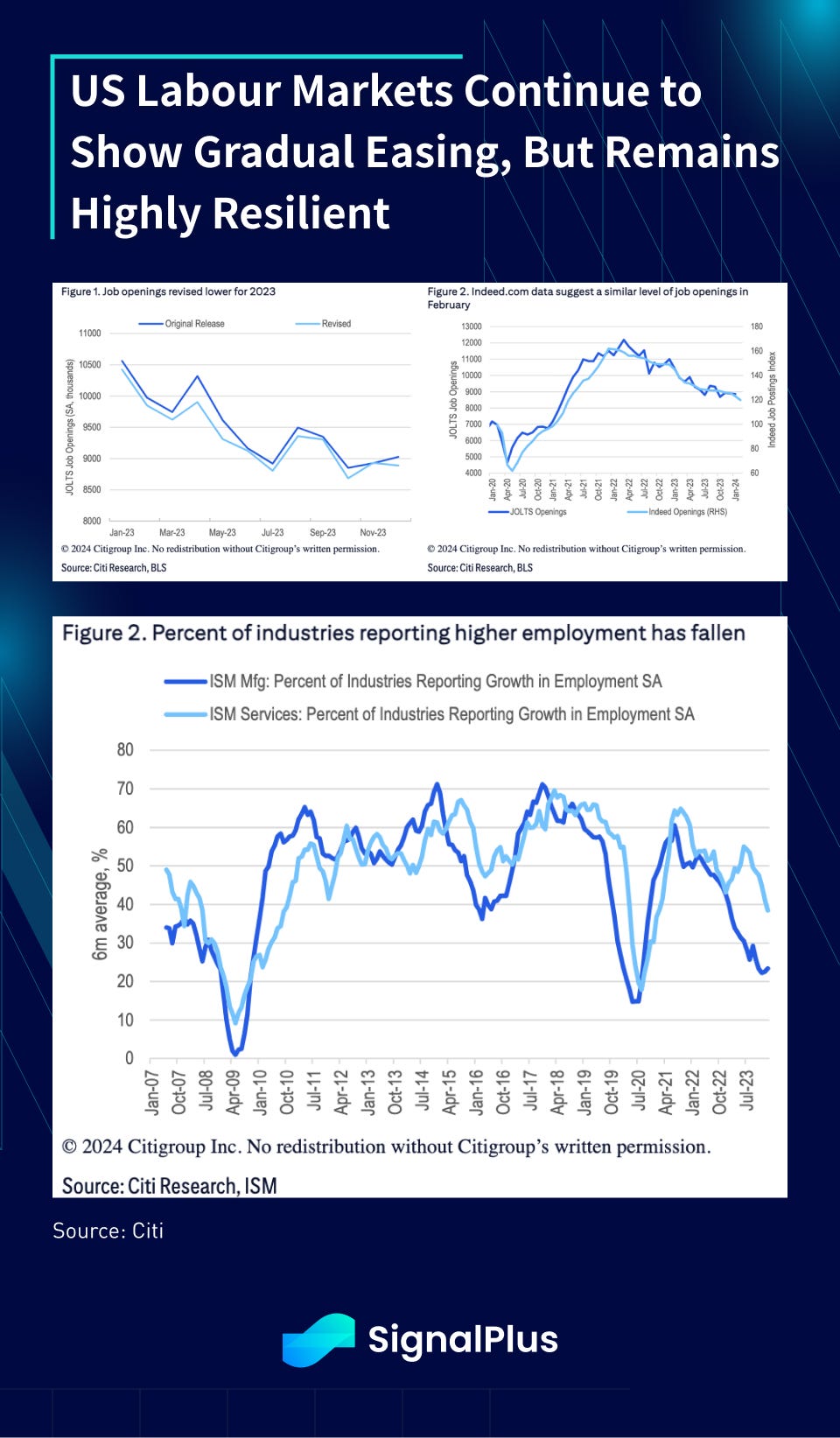

Over in the US, economic data continues to show a slightly softening but still highly resilient labour market, with ADP increasing by +140k in February (vs +111k in January), with private payrolls still adding an average of >200k jobs per month since 2023, compared to merely +50k per month pre-pandemic. JOLTS job openings declined by -26k in January after a -42k fall in December, with total job openings now dropping below 9mm since October, reflecting some easing in labour market tightness. However, layoff rates remain at a very low 1%, while the jobs-to-unemployed ratio still stands at around 1.4x, suggesting a still healthy but perhaps somewhat unimpressive NFP print this Friday.

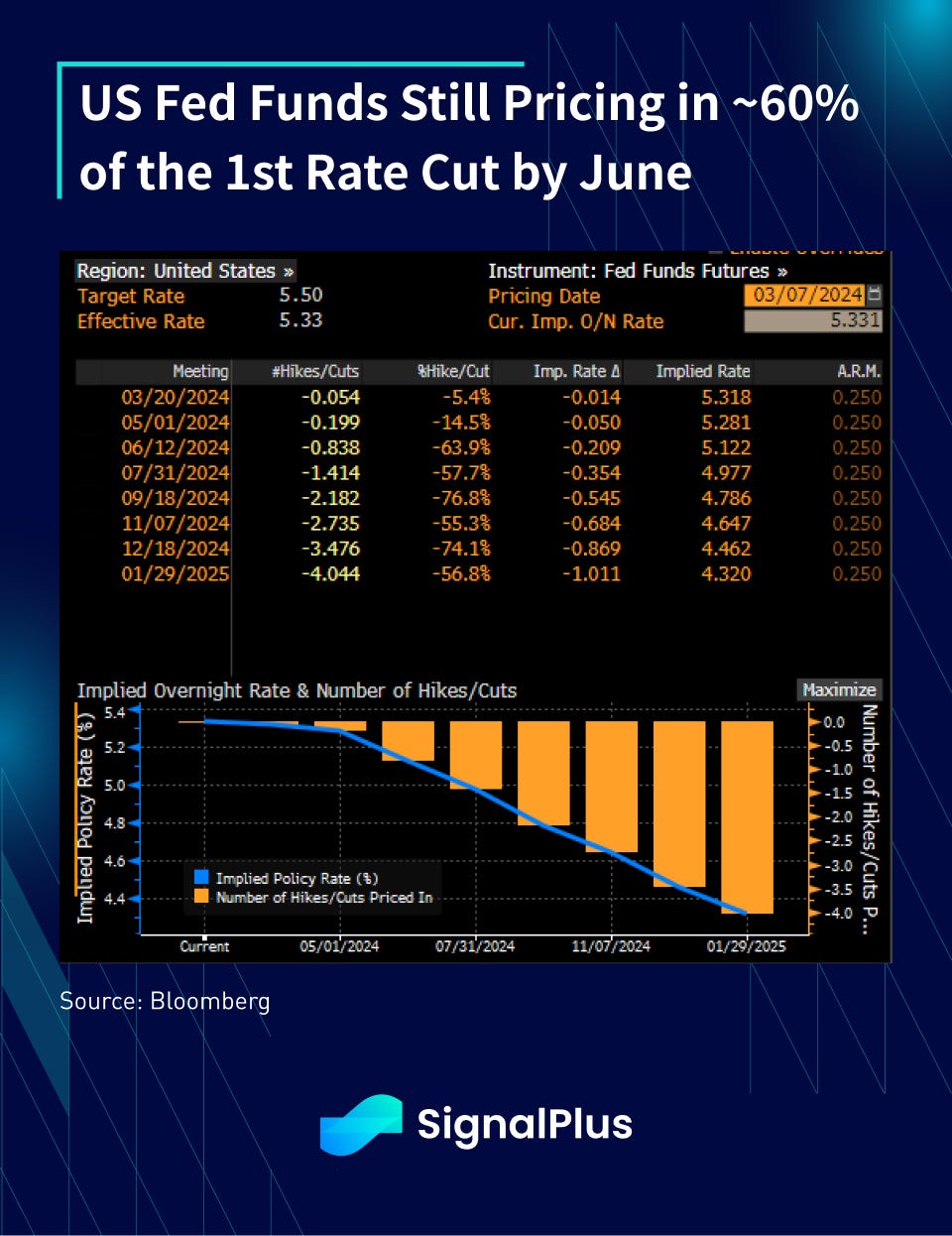

Chairman Powell testified to the US House yesterday, though his delivery was largely in-line with mostly non-reaction from markets. He reiterated the Fed’s January comments that “policy rate is like at its peak”, though that the Fed is still looking for “just a bit more evidence” that inflation is heading sustainably towards 2% before cutting rates. His strongest statement was actually related to capital holding requirements for US commercial banks, where he suggested that the Fed was likely to make “broad and material changes”, including the complete scrapping of the current government plan, scoring yet another win for our TradFi banking friends once again. Fed fund futures are still pricing for the first cut (~60%) at the June meeting, and just over 3 cuts by year-end.

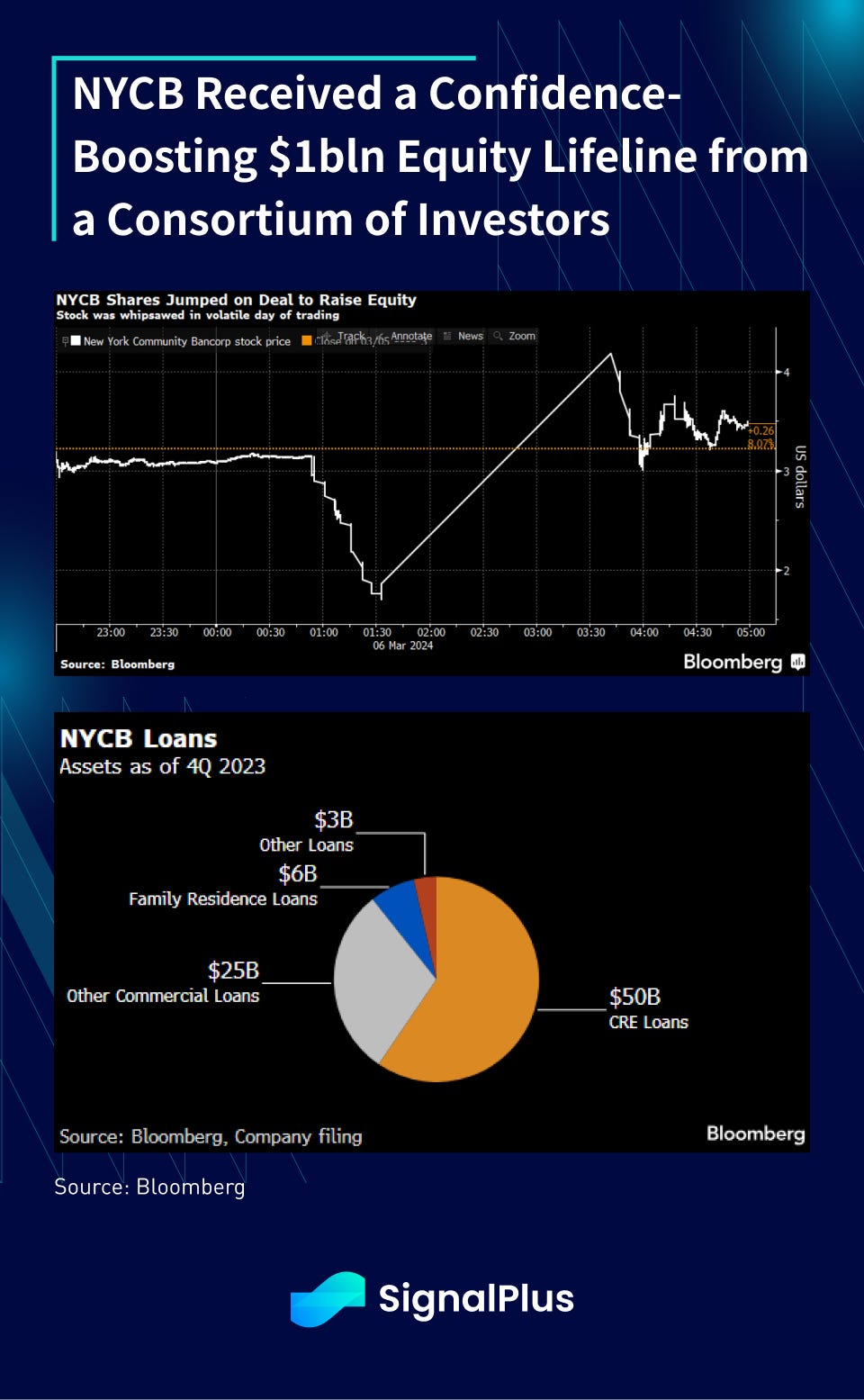

In equities, the beleaguered NYCB received a much needed life-line yesterday, securing a $1bln equity investment from a consortium of investors including an outfit led by former US Treasury Secretary Steven Mnuchin, limiting contagion concerns to prevent a repeat of last spring.

Speaking of optimism, a relic of the ‘good old days’ has returned, as convertible bond yields on AI names such as Super Micro Computer have dropped back to negative territory, where investors are paying companies a yield in order to have a chance to buy well OTM calls on their equity. SMCI has surged 1000%(!) in the past year and is due to be added to the SPX later in March, with their March 2029 convertible bond trading at a -3% yield with an equity conversion price at a 41% premium over the current spot price. Hot hot hot!

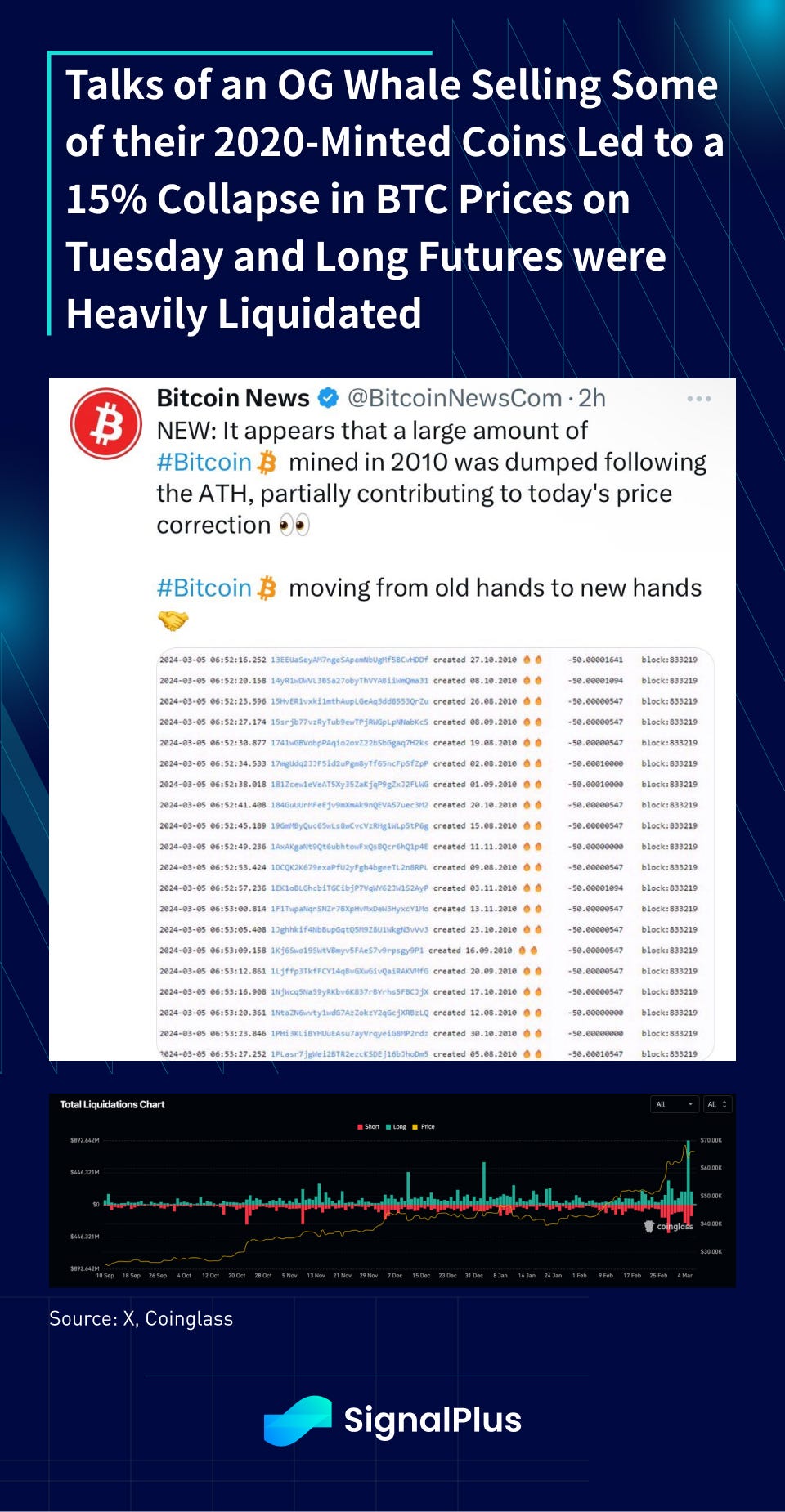

Finally, in crypto, prices have been chopping at BTC cratered after making ATHs of $69k down to $59k in minutes, as talks of a long-dormant wallet had apparently mobilised their holdings to Coinbase to presumably take profits against their $0.28 mining cost (Talk about diamond hands). That led to massive long liquidation in futures, but was met by heavy buying in the spot ETFs, ultimately stabilizing BTC at around $66k, while ETH managed to hold steady at ~$3.8k.

Sentiment remains squarely in the buy-the-dip mode as evident from the rapid recovery in BTC prices yesterday; however, we could see BTC start to underperform other tokens from here on given its idiosyncratic outperformance vs ETH and other altcoins, and a curious chart of BTC vs 3x levered Nasdaq also shows the former looking rather stretched. We wouldn’t be surprised to see a period of choppy consolidation in the near term with some BTC underperformance over that stretch.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments