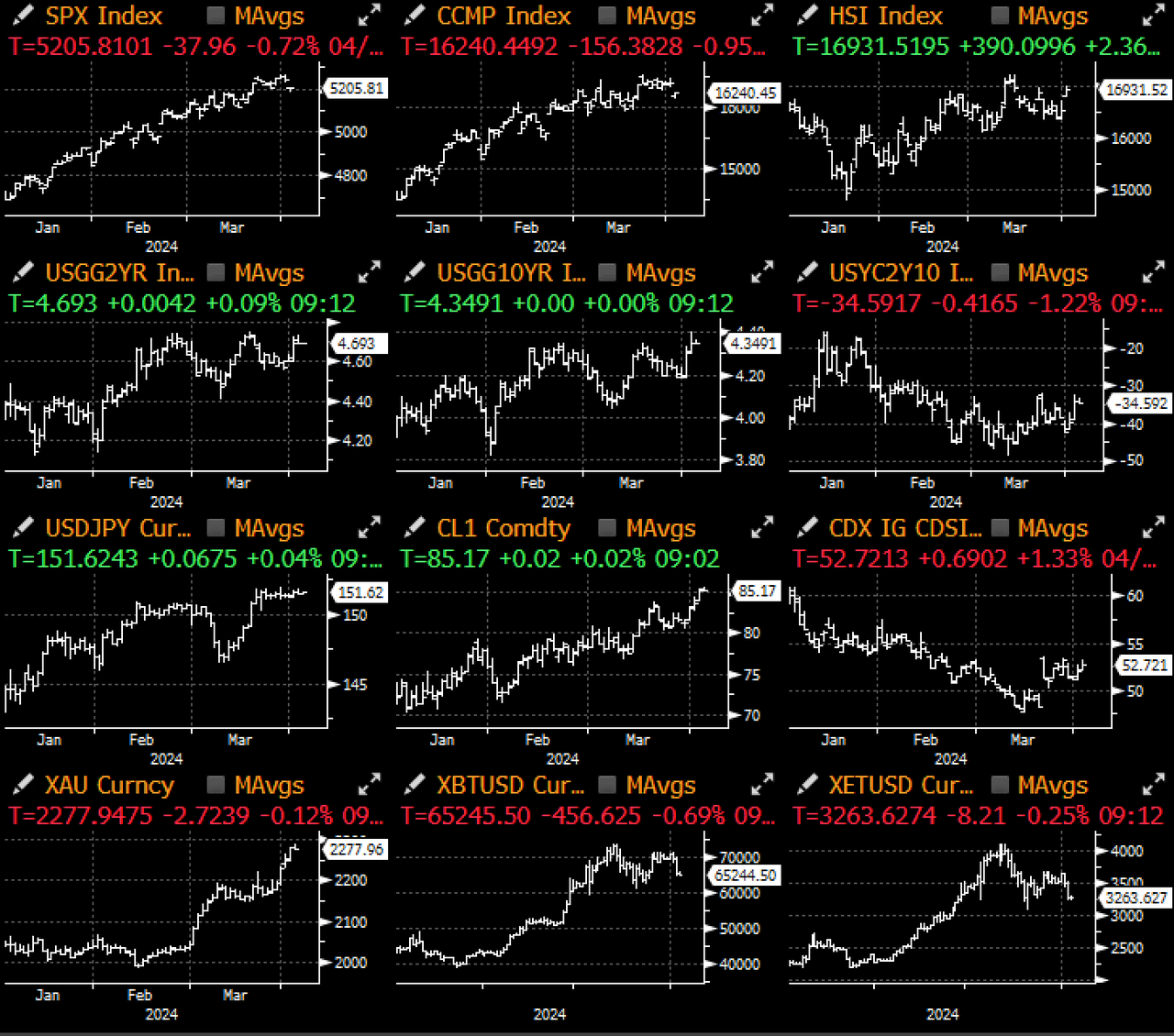

The risk-off breeze that began yesterday gathered strength, leading to a simultaneous drop in equities, bond prices, and crypto. Starting from the policy side, Fed speakers continued to backtrack the (irresponsibly) dovish comments out of Powell’s March FOMC, with Loretta, Mester, and Daly all walking back expectations of any imminent rate hikes on the horizon.

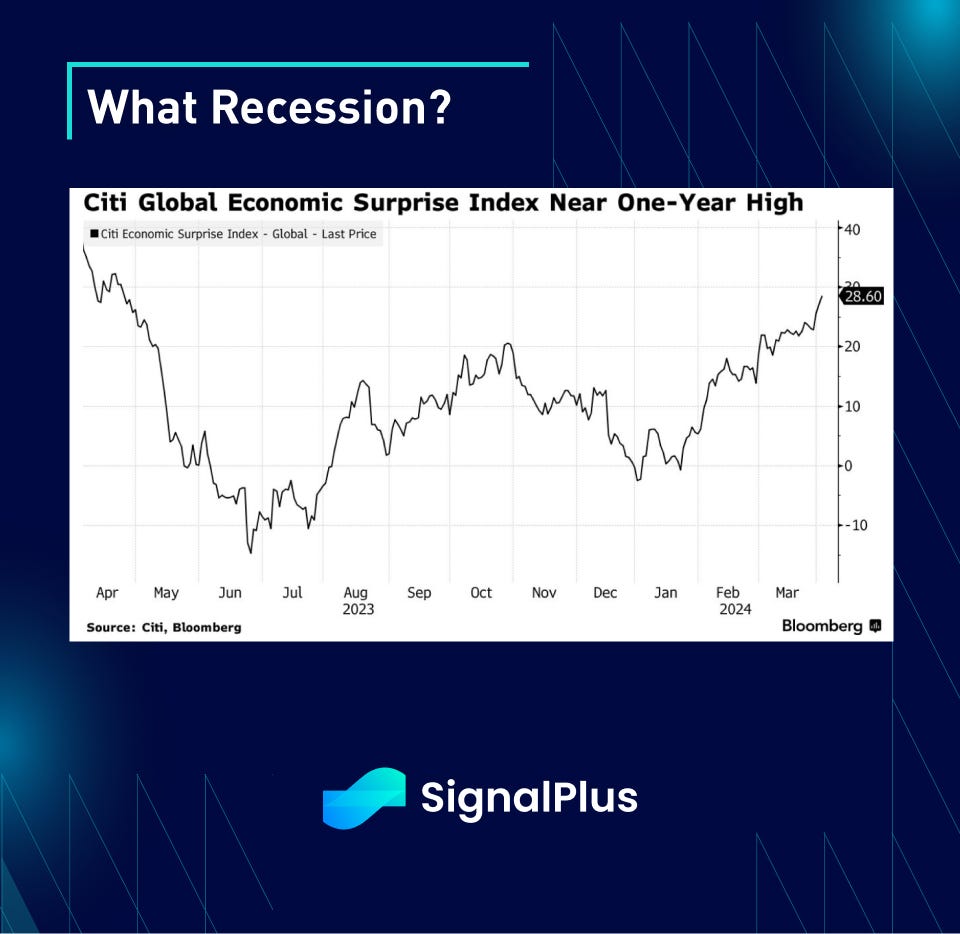

After all, why not right? Outside of the series of sticky inflation surprised we shared in yesterday’s comments, Citi’s global economic surprise index has also been a one-way train, shooting to 1-year highs on continued robust economic performance.

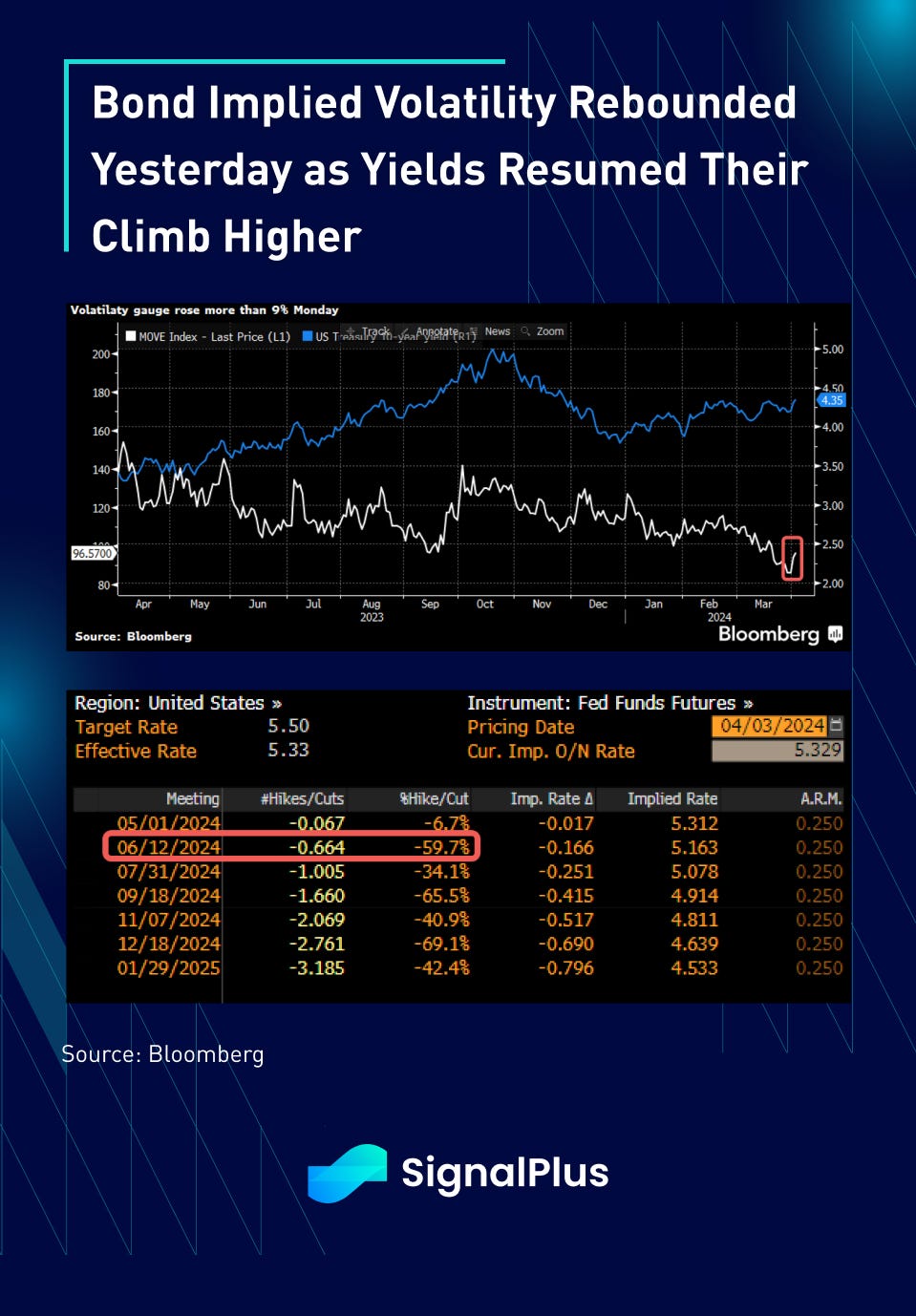

As a potential sign of concern, bond investors might be starting to feel angsty, as the MOVE bond volatility index jumped a fair amount against its interim lows yesterday, as 10yr yields are threatening to head towards 4.50% with the June cutting odds increasing looking like a coin flip. Furthermore, corporate issuers continue to rush to the market to lock in borrowing rates despite market expectations of rate cuts. Wall Street is calling for ~$20bln in new bond supply this week, and up to another $100bln this month, up +50% from a year ago.

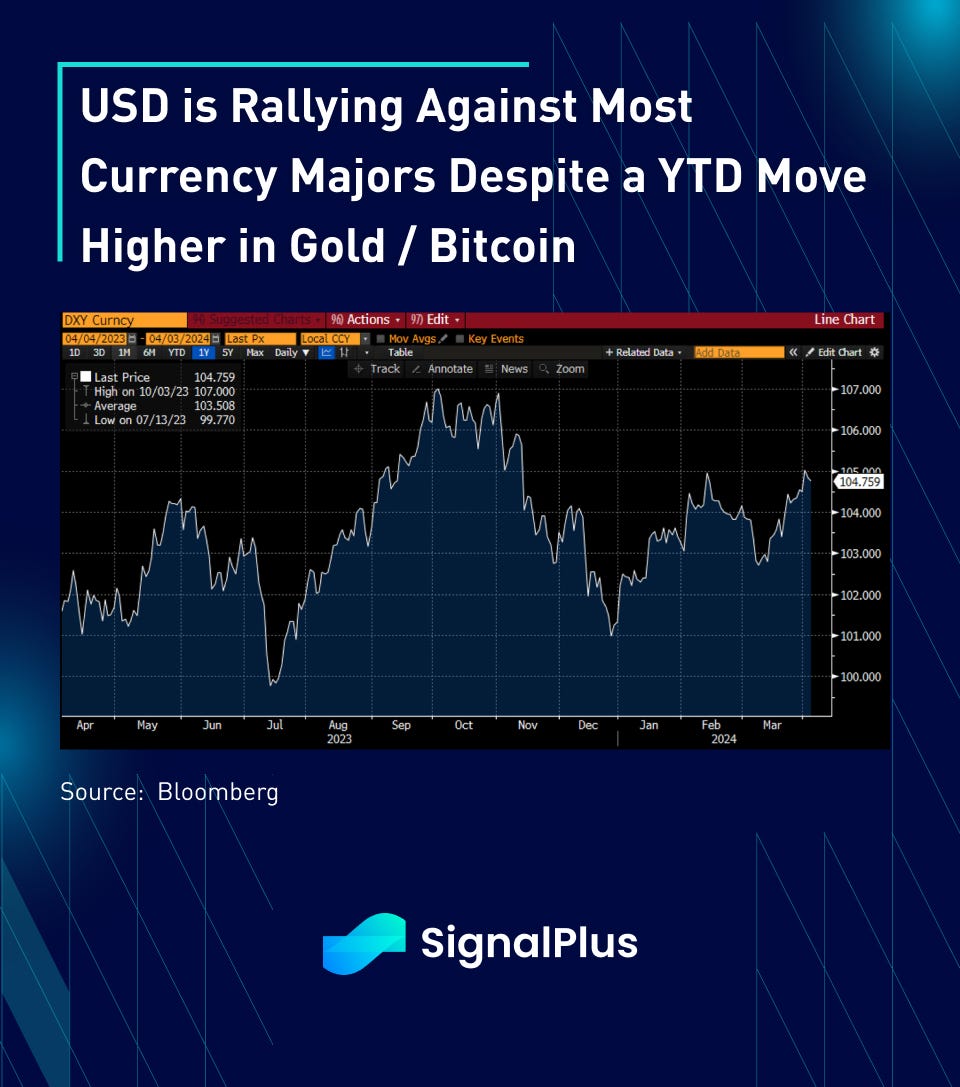

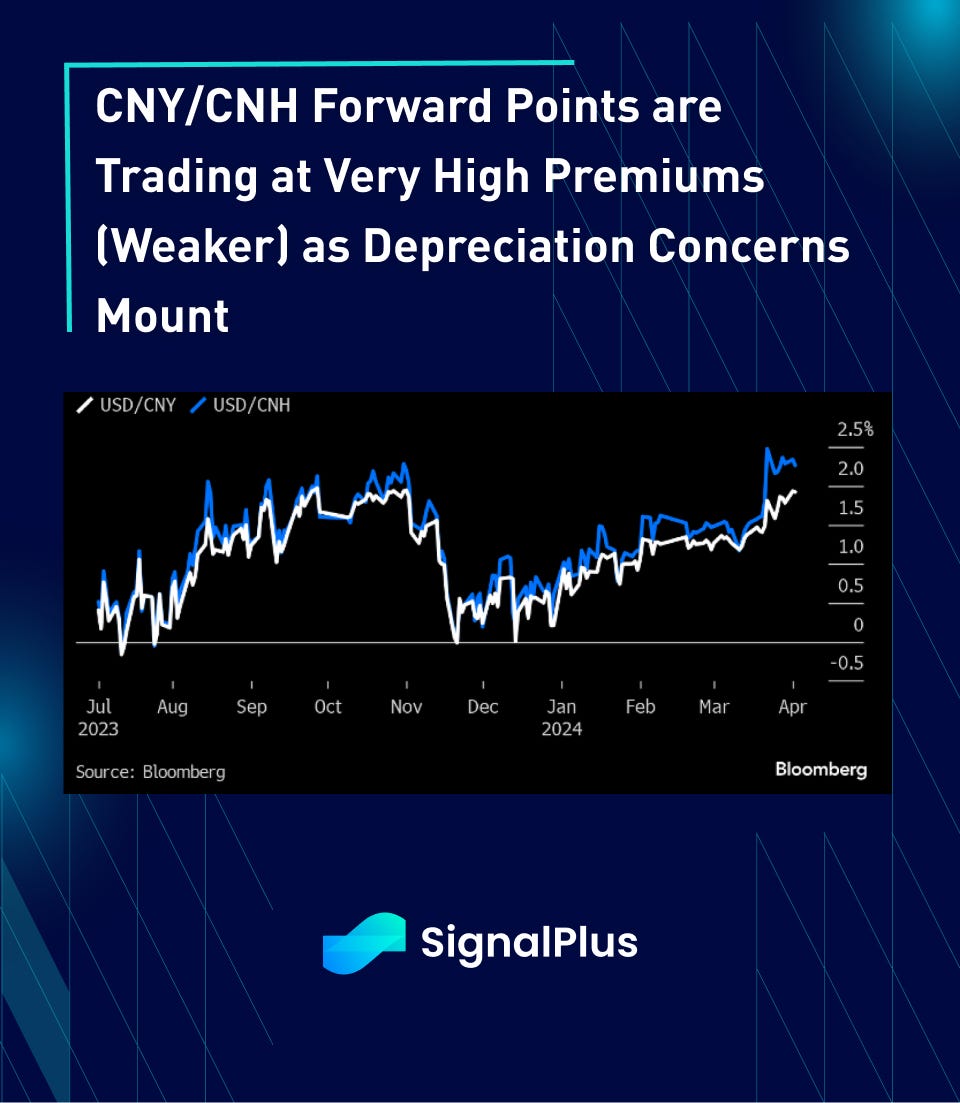

Back on the risk-off sentiment, oil quietly heading back to 2023 highs at around $85 per barrel, rallying by 20% YTD, and is probably the main CPI gauge that actual consumers actually care about. Furthermore, with the USD uncharacteristically rallying against most major currencies (inflation misses in Europe, BoJ’s dovish ZIRP exit, China’s economic woes), even as Powell was pivoting dovish and anti-USD assets such as gold and Bitcoin have been rallying all year. This is putting significant depreciation pressures against the likes of CNY, where FX forward points are trading at a premium above the worst levels seen in 2023, as markets remain concerned over the health and state of the Chinese economy.

Over in equities, outside of fading rate-cut expectations, the index was also dragged down by Tesla (-7%) after it reported pretty terrible Q1 results that drastically missed average estimates. Big misses on car deliveries (-14%), factory shutdown concerns, mounting inventory, and concerns from rising competition from BYD and Chinese car makers all contributed to the negative sentiment. Will we finally see some April underperformance out of SPX stocks as it ‘catches down’ to rate cut expectations? Or will we stay in Goldilocks’ land for another quarter?

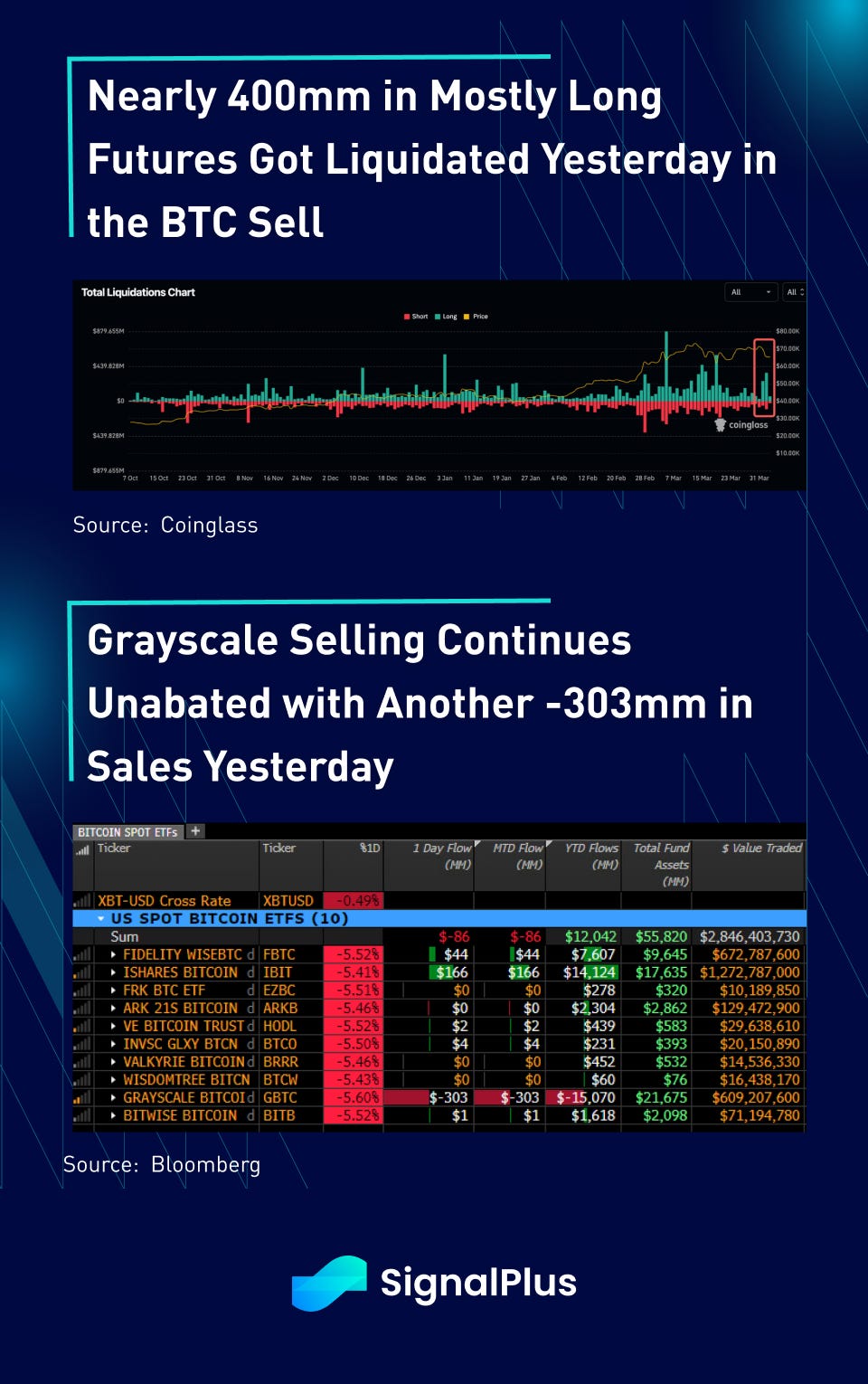

Speaking of risk-off, crypto prices cratered with BTC dropping from 69k down to a low of 64.5k yesterday, with nearly 400mm in futures liquidated within an 18 hour period. As per the recent script, the sell-off has been happening in Asia time, probably in response to the net ETF inflow data we receive after the US close (-86mm yesterday), plus the fact that traders in Asia are predominantly positioned long.

As a result of the recent stop-outs, future positions are likely much cleaner with perpetual funding rates trading down substantially back closer to flat, while short-term put-skews are seeing more bids as spot price momentum has weakened substantially.

The near-term volatility might persist for a while. Arkham, a blockchain analytics company, reported that a wallet tied to Silk Road under the government’s control has awakened and executed a few test transfers to Coinbase. Expectations are for this to be a precursor to a bigger transfer, leading to possible token sales by the US government into fiat. Furthermore, ETF issuer Proshares launched a number of leveraged Bitcoin ETFs (BITU and SBIT) targeted towards retail users. YOLO!

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments