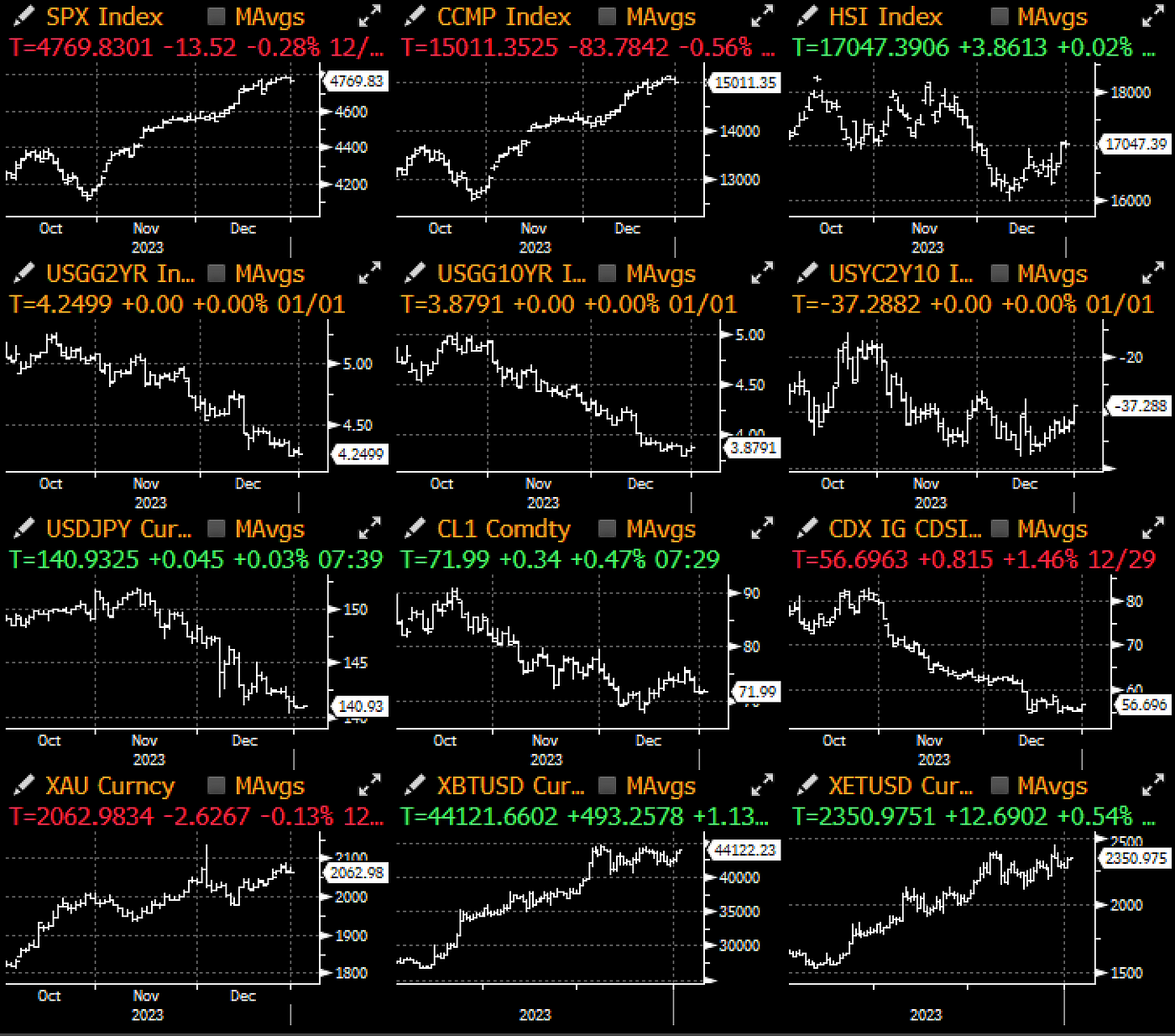

Happy new year! Global asset markets are entering 2024 riding a palpable sense of optimism, with investors bullishly positioned across nearly all asset classes (except the USD) with a wave of interest rate cuts expected across most developed central banks. The past year caught most macro observers off guard as risk assets scaled the wall of worry, with US equities closing at near a record high despite the Fed’s unprecedented hiking campaign, demonstrating once again that macro relationships are complex and constantly evolving.

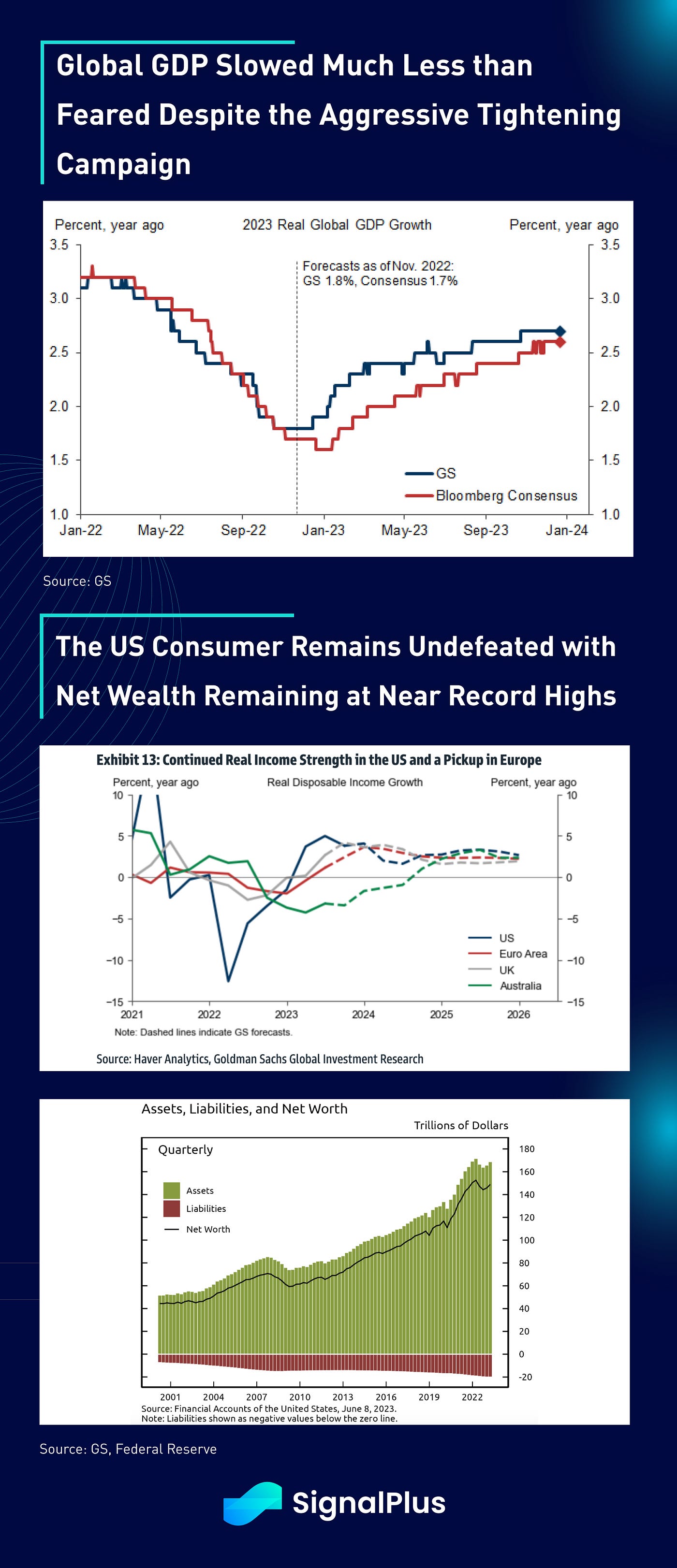

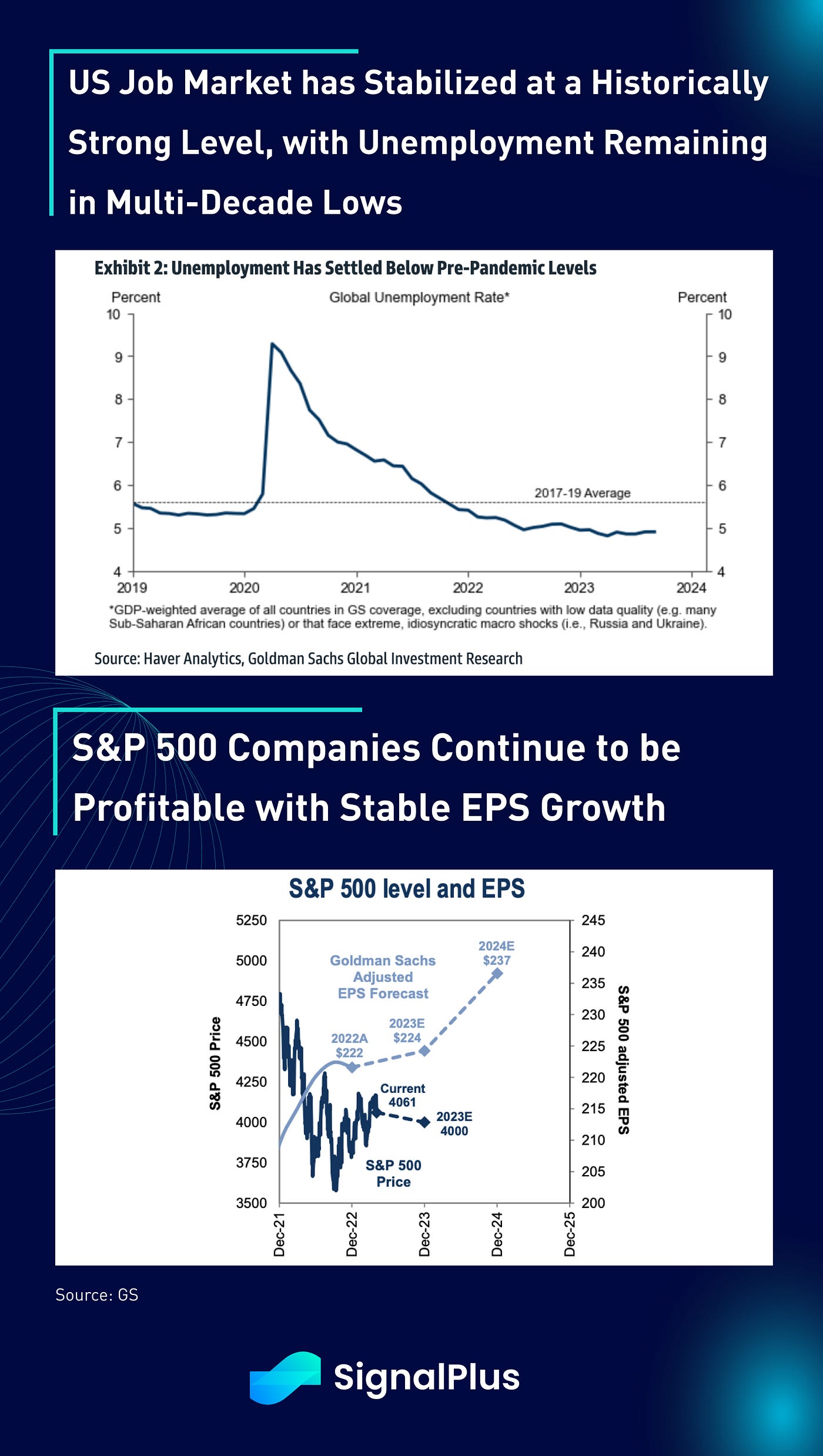

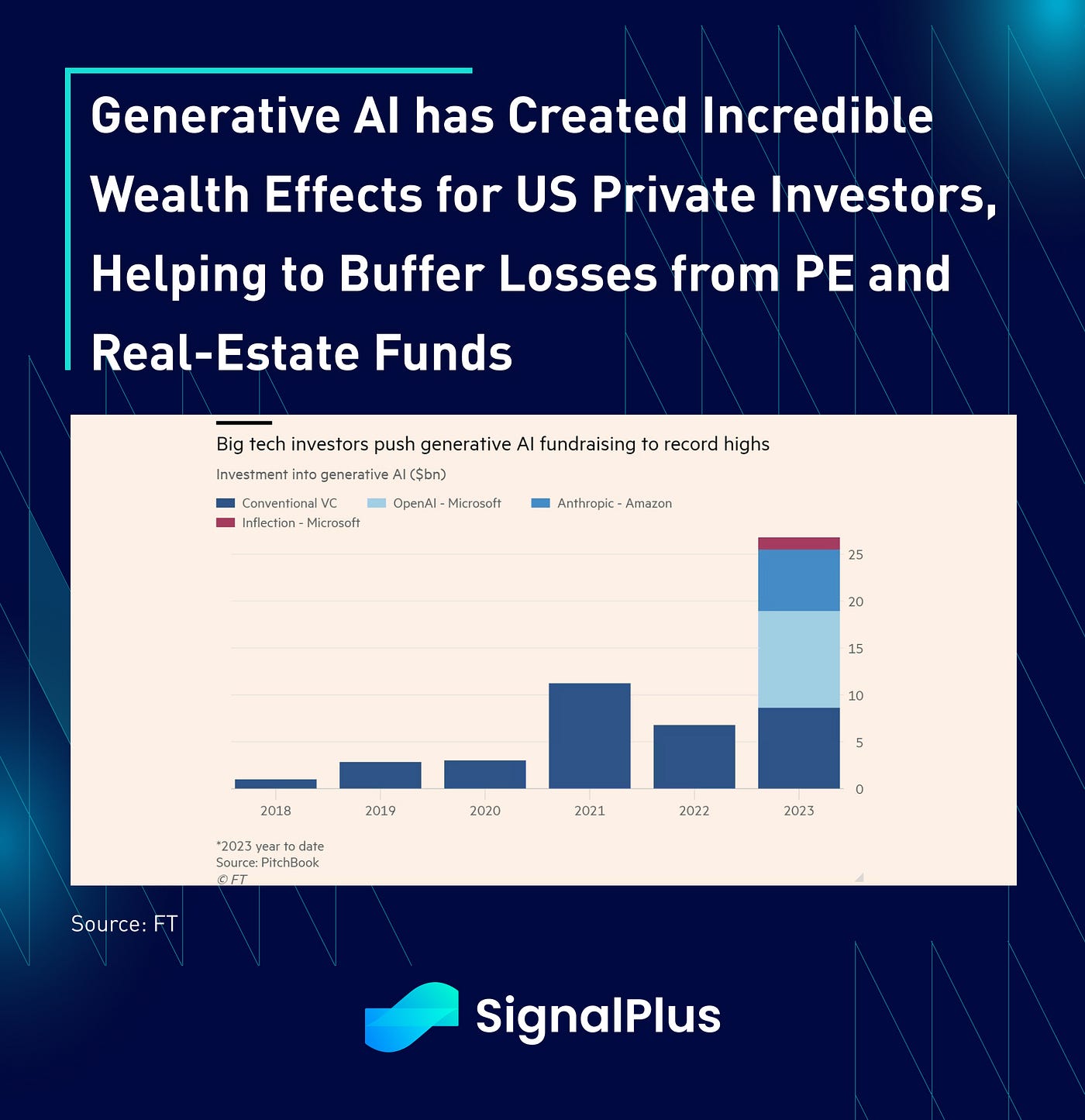

With the benefit of perfect hindsight, it is now clear to see why 2023 was such a positive year for risk assets:

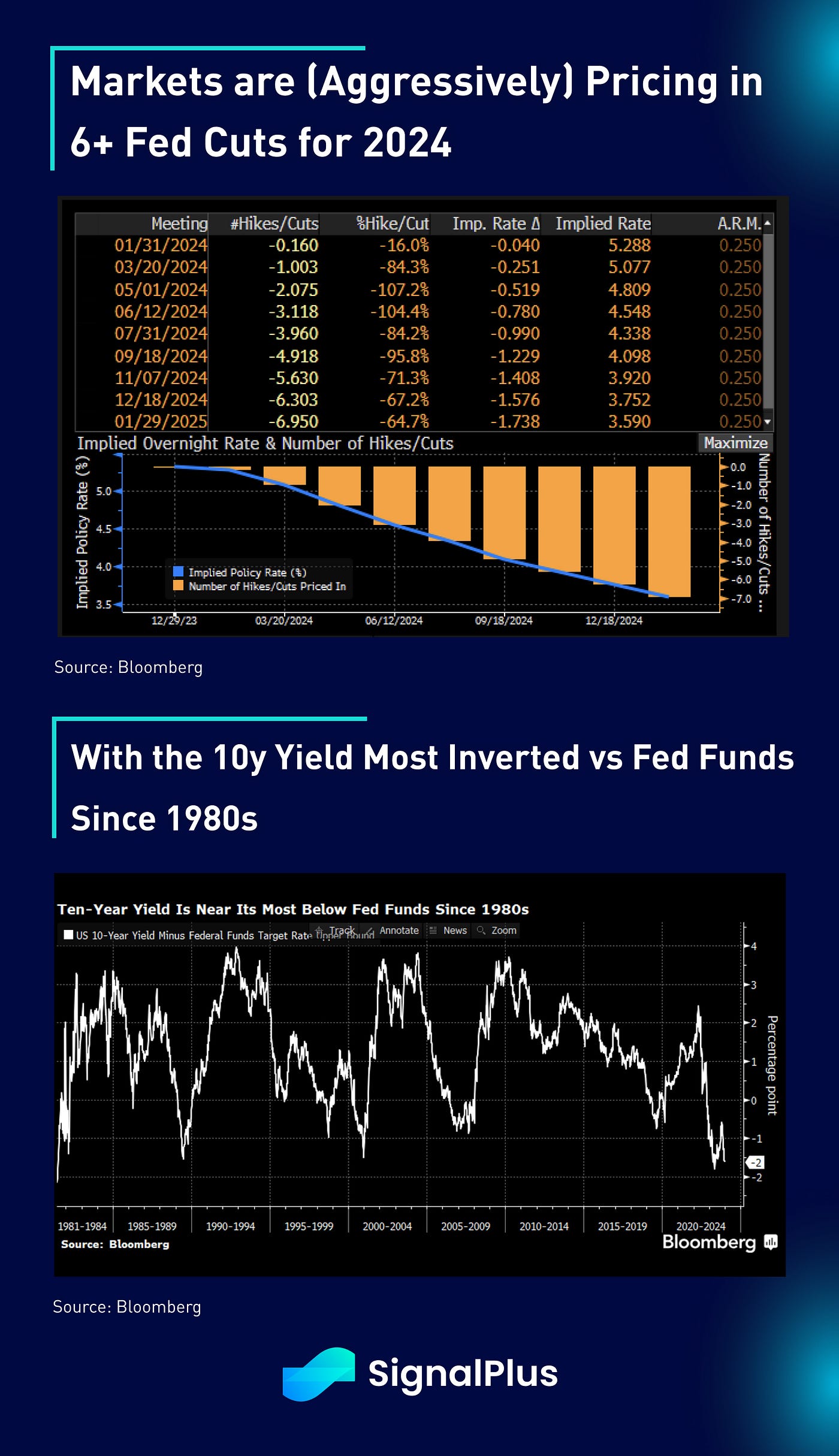

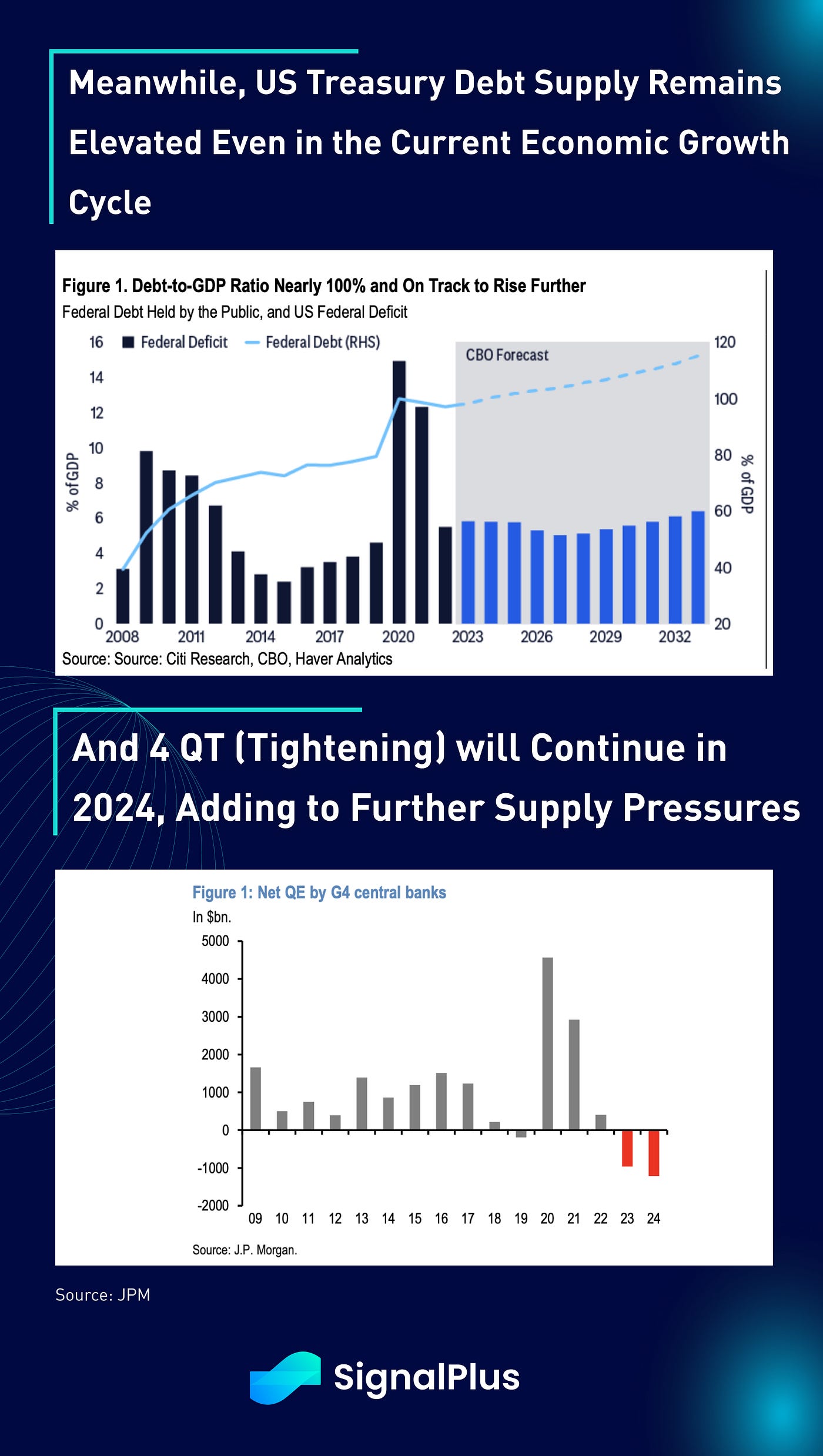

With momentum riding high into the new year, and global central bankers setting up a powerful vanguard of rate cuts, it is probably still too early to consider fading the risk-on move, especially considering the positive early-year seasonality markets tend to enjoy with fresh capital being put to work. While valuations are undoubtedly rich, and we remain negative on US fixed income as we think investors are overestimating the extent of Fed policy easing while underestimating the negative impact of an elevated supply picture, and we believe that yields might not be able to sustain the current levels throughout the year. Nevertheless, we see a non-zero risk of the Fed delivering ‘insurance cuts’ earlier in Q1/Q2 to thaw the deep freeze currently in IPOs / private equity / real estate markets, while offsetting with less aggressive eases later on as the economy remains in fine shape. As such, the right move is probably still to enjoy the current ride for now, and worry about any payback later on towards Q2.

Traders will return this week to a heavy economic calendar, with ISM, JOLTS, FOMC Minutes (the Pivot), ADP, NFP, ISM Services, and Durable Goods to round out the week. Expect markets to return with a bang with early FOMO risks if the dataset remain dovishly inclined!

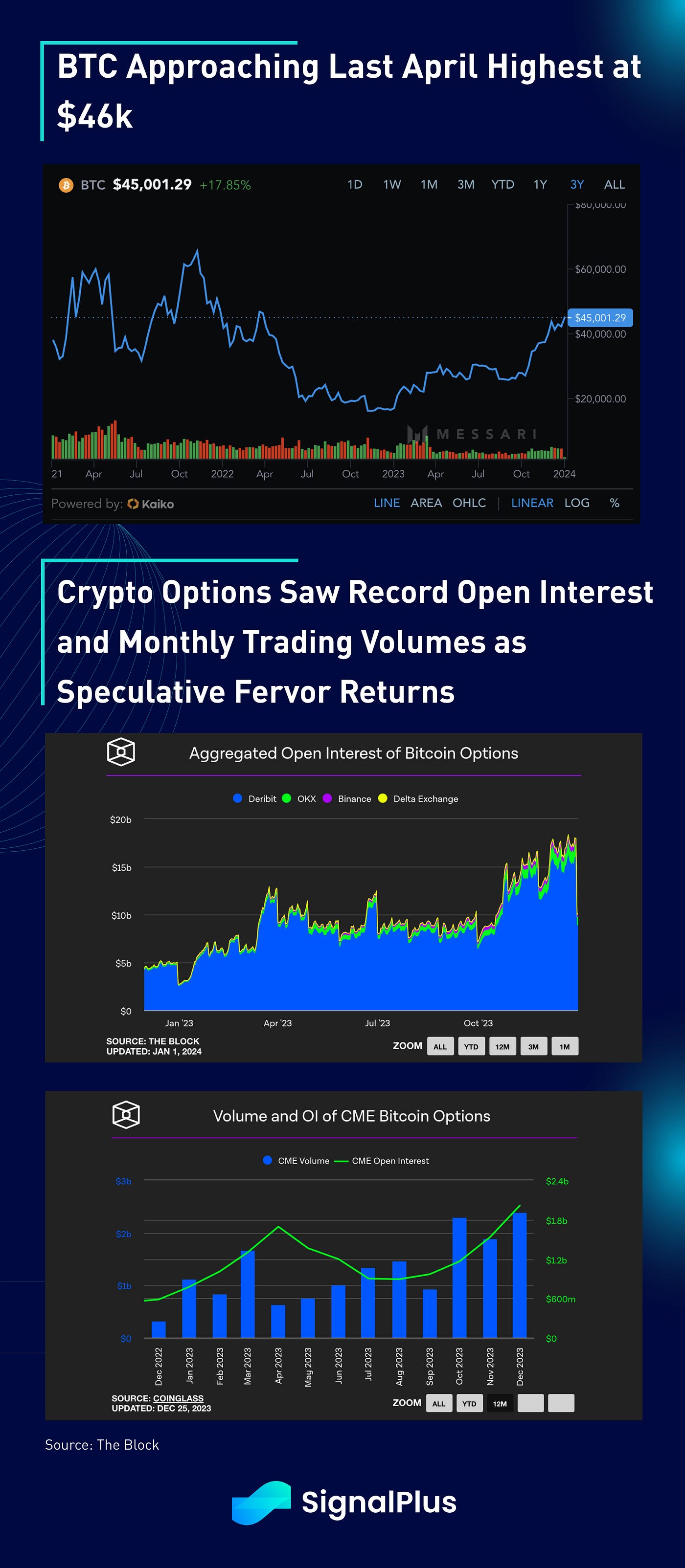

Crypto prices continue to usher with its rapid recovery, as token prices are awash in a sea of green with BTC approaching the last April highs of $46k before we last fell into a year-long bear market. With the SEC expected to give their final approvals on the BTC spot ETFs this week, speculation is running at a fervish pace with crypto options closing 2023 at record open interest and monthly trading volume. Over $11bln of BTC and ETH options expired last Friday on Deribit, with December registered over $1.8bln in monthly volumes, eclipsing the previous highs in October.

In traditional space, we saw some year-end profit taking flows in ‘equity-crypto’ proxies (eg. Miners) as we near the ETF decision, with the near term flows unclear as we balance the prospect of incoming institutional flows versus a long-dormant supply being unlocked from GBTC. Similar to our view on equities, we would suggest against getting in the way of the near-term market momentum, and would be on the lookout for a potential ‘sell-the-fact’ move later on in Q1. Good luck and happy trading in the new year!

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments