Market

BTC began a rebound last week amid continued pessimism and completed the rebound to $67,000, surpassing my minimum target of $65,000. Currently, it continues to move sideways within the range but remains unstable. The bombardment of various macro issues, including the war that began two weeks ago, continues. It is surprising that BTC is still maintaining above $60,000, but considering the still unstable macro situation, GDP and PCE economic data releases, and stock earnings season this week, hedging was recommended at the $67,000 level. (Greekslive Options Community)

Another important event awaits us in early May.

- May 1 – QRA, FOMC

- First week of May – Earnings for most stocks

- May 6~10 – BTC mining company earnings

It looks like we’re going to have some pretty volatile weeks ahead of us. Judging the current market, it is suitable for short-term trading within the range, and it seems difficult to be sure of the direction until the range is broken. In other words, this sideways trend may last longer than expected. My view from a month ago that said BTC would likely reach $80,000 in April was definitely wrong, but I still think BTC is not the top. But first this volatile situation must calm down. If the overall situation worsens further, the sideways/weak trend is likely to continue. For the time being, it is best not to use too much leverage. Altcoin trading is still not recommended.

I wouldn’t be too bearish because nothing has changed yet. Overall, I remain optimistic.

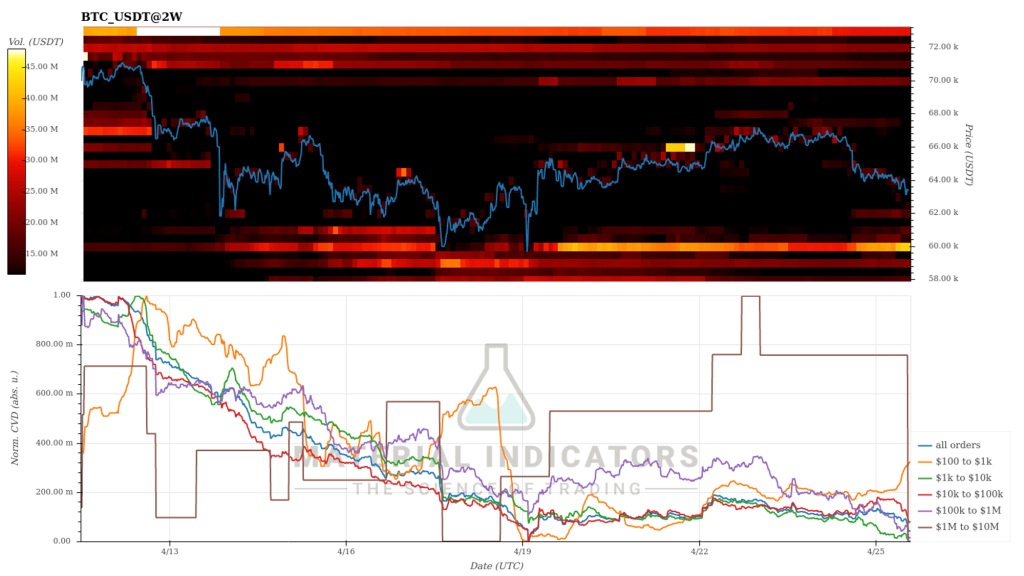

Buy orders at the $60,000 level still exist. The brown whale sold BTC today, but nothing has changed compared to a month ago. In order to break below the range, a lot of spot selling is needed. I check the buy delta at the $60,000 level whenever the price falls.

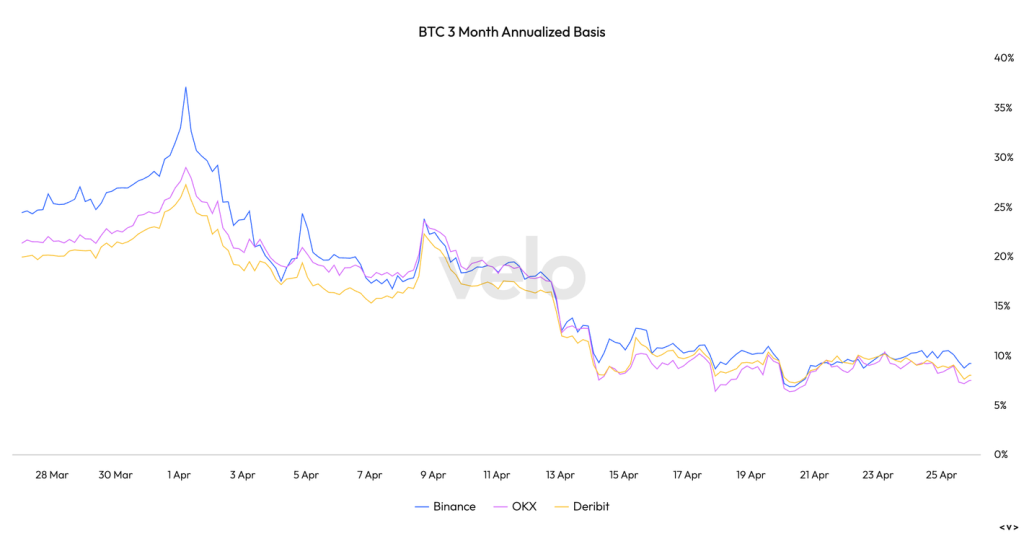

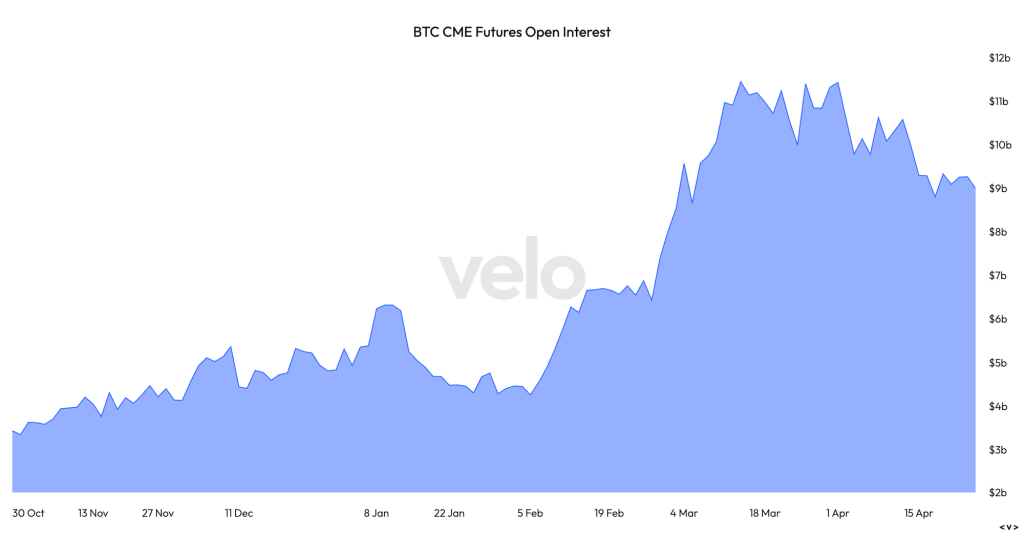

Futures basis continued to decline throughout the month, falling from 30% to below 10%. CME futures OI also continues to decline. To put it positively, we can say that the market is normalizing, and to put it negatively, we can say that market enthusiasm (demand) is decreasing. Objectively, it is clearly a risk-off situation. I think the prerequisites for the next upswing are well underway.

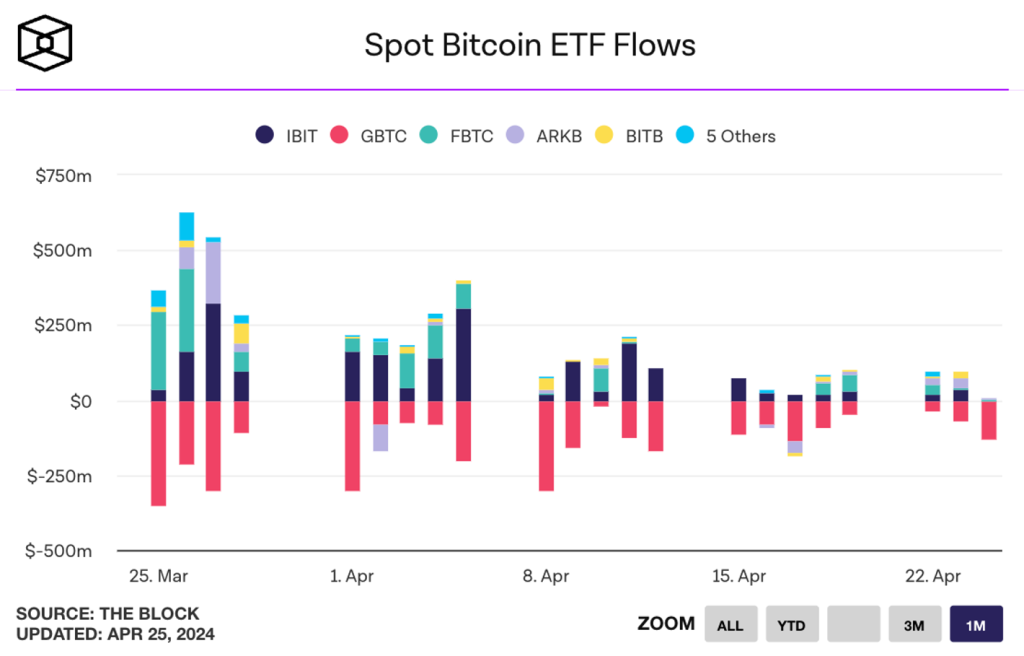

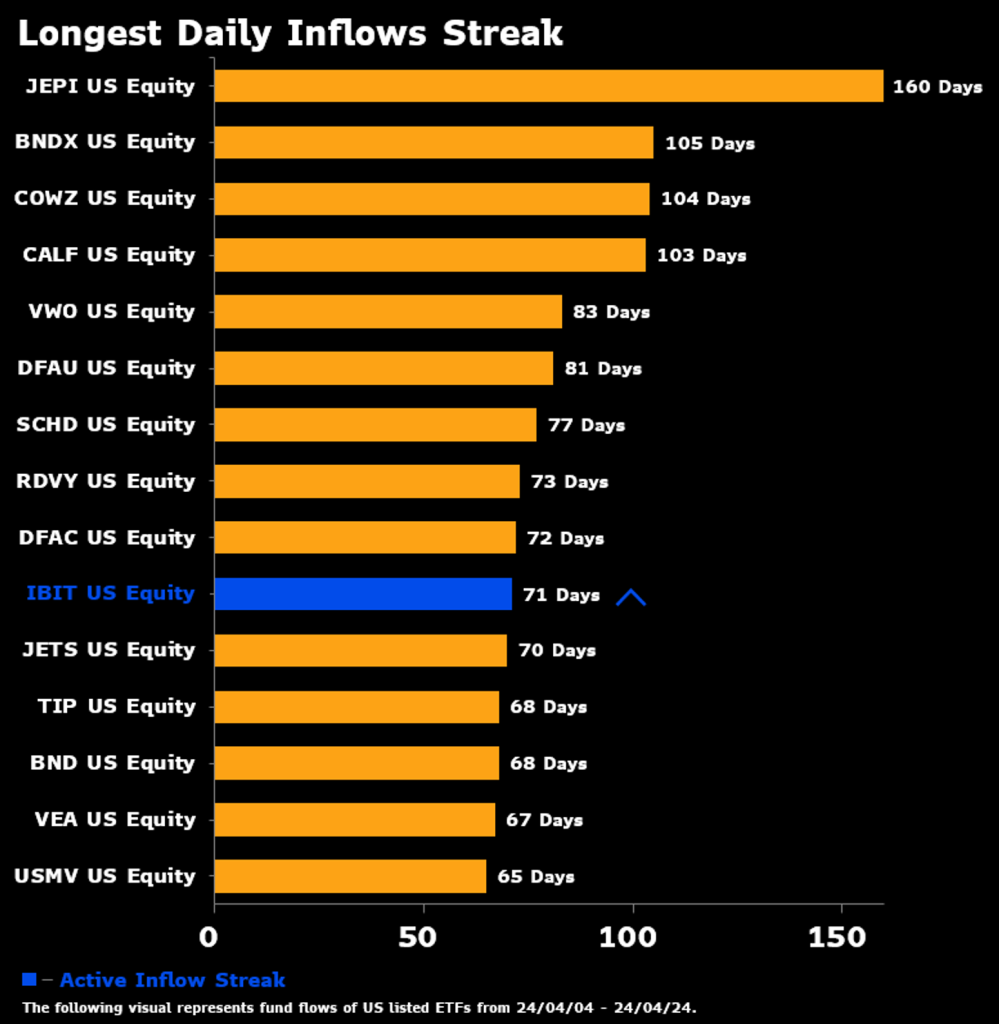

Today’s big news and most interesting issue may be the news that IBIT’s 71-day continuous inflow has come to an end. Additionally, GBTC outflow continues. This is clearly bearish news, as ETF flows clearly have a significant impact on the psychology of market participants. As I have consistently said, TradFi has no choice but to react sensitively to macro issues, so it is natural that ETF inflows decrease in risk-off situations. Since trading volume on existing exchanges is still high, it is best not to expect too much that the ETF will increase the price of BTC. This is good for the long-term trend of increasing long-term holders.

In Hong Kong, BTC spot ETF trading will begin on April 30th. While this is certainly optimistic news for the long term, I think the inflows will be limited. Crypto investment is prohibited in mainland China and the Hong Kong market is smaller than the US market.

It is certainly true that IBIT’s 10th place record, with inflows for 71 consecutive days, is a great record. News of institutions holding ETFs through 13F is also continuously increasing, although the amount is not large. This is a very surprising result, considering that even just a few years ago, this would have been unimaginable. It’s still positive in the long run.

There was news today that the ETH spot ETF will not be approved in May. I wasn’t surprised at all. The probability of approval in May has been close to 0% since a month ago. I haven’t mentioned ETH at all for several weeks. If it gets approved, I’d say it’s the best deal of the year, but the odds are so low I’m not betting anything on it. It is true that the ETH spot ETF has an impact on the entire BTC and crypto market and is a good material to revitalize the market, but the possibility right now is very low.

ETH/BTC did not decline further despite this news and is showing signs of recovery… It’s definitely strange.

IV took a big hit this week, falling 10 points. A massacre that has been difficult to see in recent weeks. As boring market movements continue, people’s expectations are also decreasing. Selling options was attractive in a range-bound, high-vol environment. Currently, a lot of leverage has been erased and it appears that the high volatility environment is likely to cool down somewhat, so IV is considering the possibility of maintaining the downward trend for several more weeks. Remember, half-life is a meme. It does not lead to immediate demand.

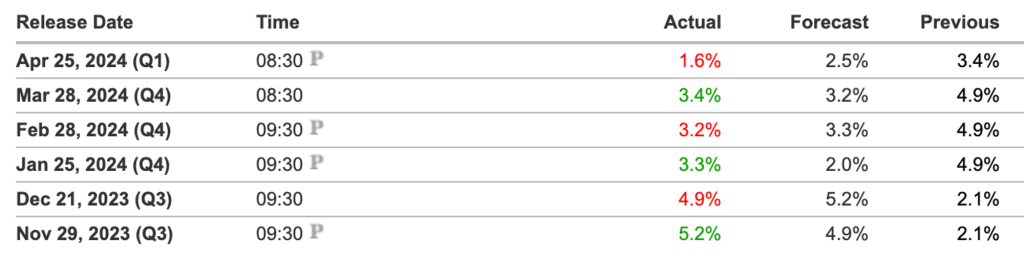

Today’s GDP release was lower than previous figures and below expectations. Inflation is still high and GDP is low, leading to discussions among people about stagflation. This will become clearer in the next GDP, but I don’t think the CPI will rise sharply, so I’m not feeling bad about the 1.6% GDP growth. Unemployment has not risen and the economy is still growing. But I agree that there is a chance it could get worse.

Macro data is released and Yield is dropping a bombshell on the markets. 10Y has risen to 4.7%, just before 4.8 (panic level), and 2Y is lowering expectations of a rate cut this year (either one or no rate cut this year). The possibility of raising interest rates is also being discussed. A very confusing situation. Although this is an honest response to the data, a continued rise in 10Y is clearly a bad sign for the market. It would be helpful to keep checking.

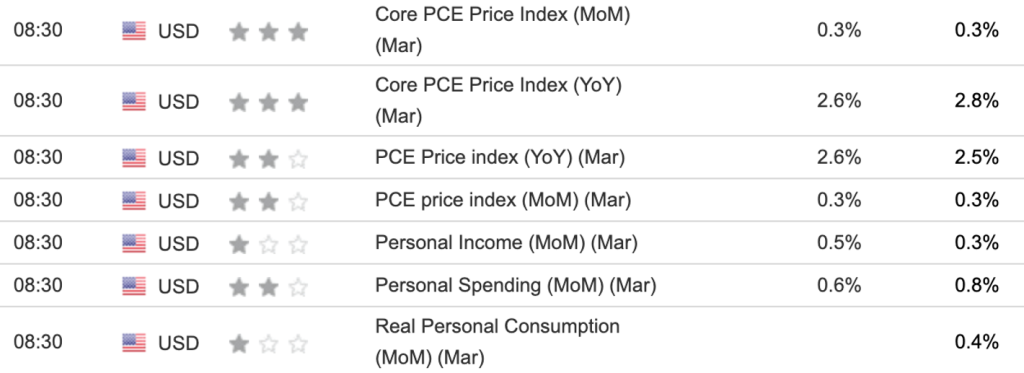

The reason long positions still need to be cautious is because of the PCE data release tomorrow. Of course, since the CPI was hot, it is expected that the PCE has already been reflected in the market to some extent, but since the PCE is the Fed’s inflation data, it will definitely not be good if it is higher than expected. Still in a state of tension.

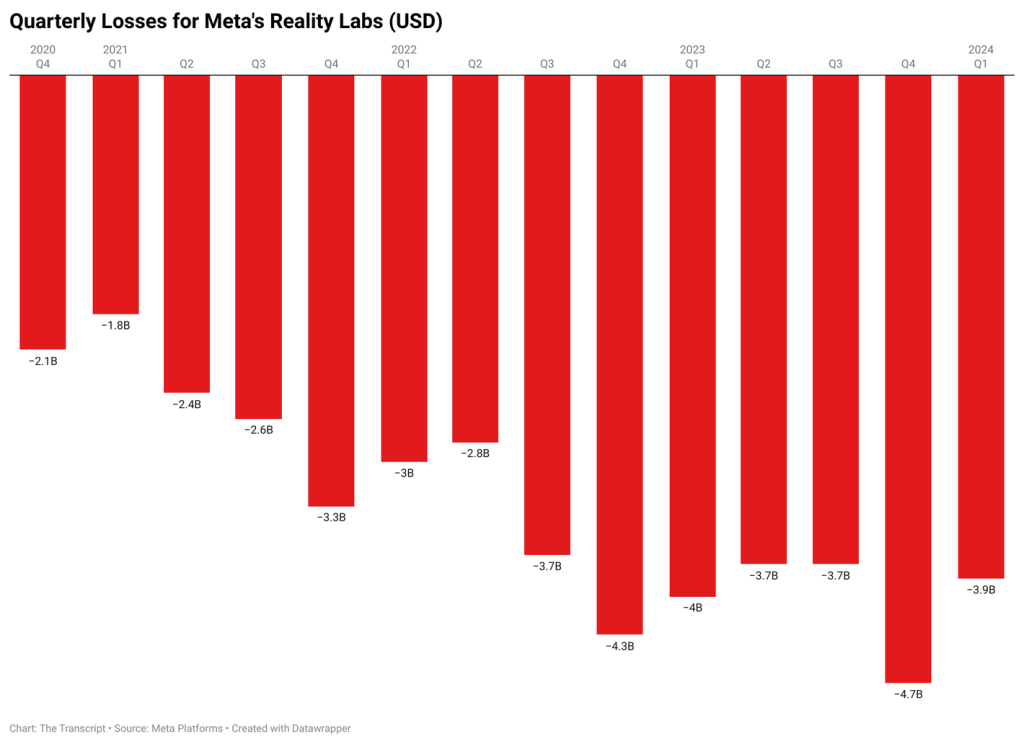

The ones that received the most attention in earnings were probably TSLA and META. Here we will only talk about META. META’s earnings were certainly good, but the guidance was poor. The stock price fell 20% due to lower-than-expected guidance. This includes concerns that META’s revenue is mostly from advertising and that increased capital expenditures will deteriorate profitability. What I can sense is that expectations for AI are decreasing a lot. Of course, I think these expectations are short-term, but currently, all AI-related sectors are being affected.

I think SPX is still in a correction phase as it was last week. If the 5000 level is not defended, we expect to retest the previous ATH of 4800 level. Movements are likely to remain volatile as a significant number of corporate earnings are expected next week. Most market movements are largely influenced by liquidity, but this earnings, along with macro data and AI expectations, has the potential to stimulate people’s emotions.

These are all my personal interpretations and opinions

NFA DYOR 🙂

Comments