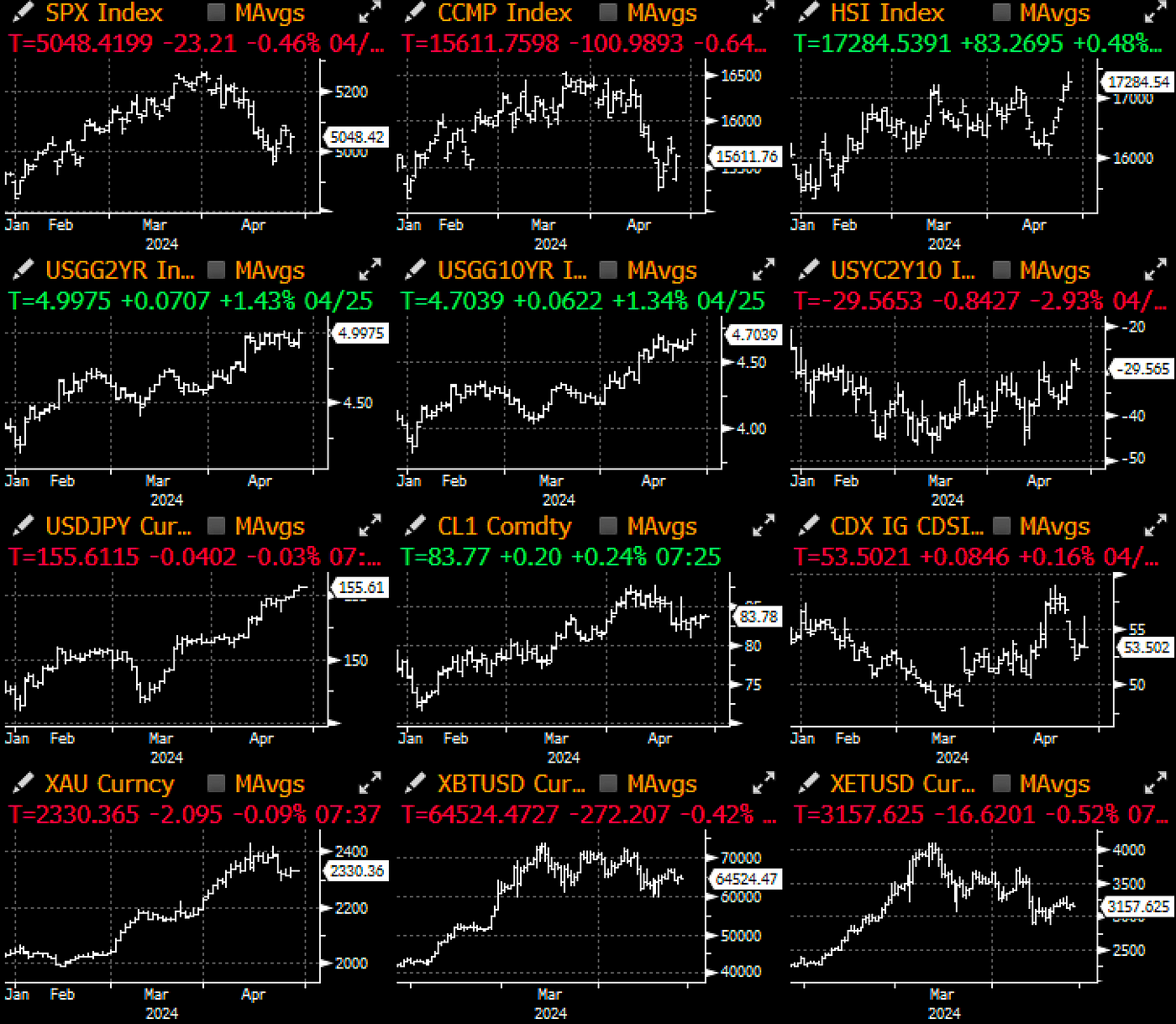

Couple of unfriendly econ data prints affected risk sentiment for much of the NY session. US Q1 GDP came in at 1.6% vs 3.4% in Q4, with personal consumption decelerating to 2.5% (from 3.3%) and goods spending dropping to -0.4% (from 3.0%). Inventories (-0.3%), net exports (-0.86%), Federal spending (-0.2%) all detracted from growth in Q1, while the PCE price index uncooperatively jumped to 3.1% (vs 1.6%), the highest reading since 2Q2023, while private domestic demand was the main bright spot, adding +3.1%. Unfortunately, any optimism was dashed by a significant jump in core PCE deflation to 3.7% (vs 2.0%), suggesting today’s (Fed focused) core PCE is likely to carry upside risks against headline consensus of 2.7%.

All in all, it was a fairly toxic cocktail for asset prices, with softer economic output against higher prices (dare we say… stagflation?). US treasury yields jumped 6–8bp across the curve, with 2yr yields breaching 5% at one point before correcting back to 4.99%. Cumulative interest rates for FY2024 have fallen back to just 1.4 cuts, a staggering change of fortune from 8 cuts (!!) being priced-in earlier in January.

Unless PCE surprises dramatically to the downside, markets would expect some ‘recalibration’ out of Powell’s FOMC presser next week. Recall an earlier interview with Chicago Fed President Goolsebee who stated:

“Now that we’re seeing — after six, seven months of very strong improvement and close-to-2% inflation — something that’s well above that, we have to recalibrate, and we have to wait and see” — Chicago Fed Goolsebee

It would be reasonable to expect the chairman to dial back his March bravado, and be forced to accept that inflation developments have not proceeded in the way the Fed would have preferred. An additional variable would be whether a ‘hawkish recalibration’ would spill over into the QT-taper timing, where markets are currently expecting a taper date as early as May. Keep an eye out on whether “few participants” noted to continue QT in its current space until we see further reserve deterioration.

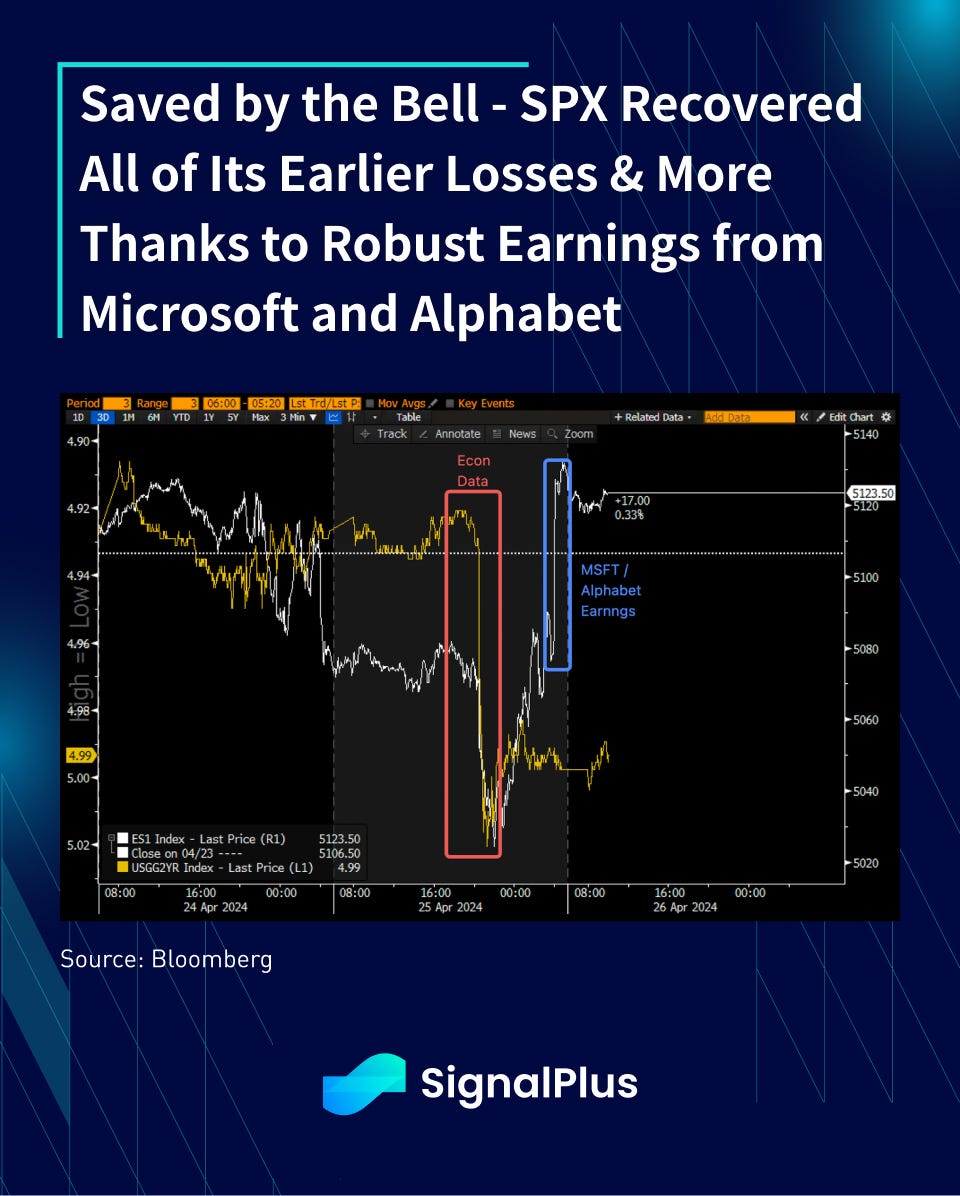

US equities fell -1% for most of the session, weighed down further by poor reaction to Meta’s earnings overnight, before staging a ferocious +2% counter-trend rally post Microsoft and Alphabet earnings late in the session. Microsoft shares jumped >5% after revenues beat across the board (Cloud, PCs, Productivity), while Google jumped over 11% on advertising and services beat, in addition to announcing a $70bln buyback and the company’s first ever dividend payment.

Crypto major prices remain in a holding pattern, with investor attention continuing to be diverted towards memecoins / BTC runes given their YTD runs. BTC ETFs saw a 2nd consecutive day of outflows, continuing a somewhat disappointing 4-week run with mainstream investor interest slowing materially, despite native excitement over the most recent halving. We remain neutral to cautious on price action at the current juncture.

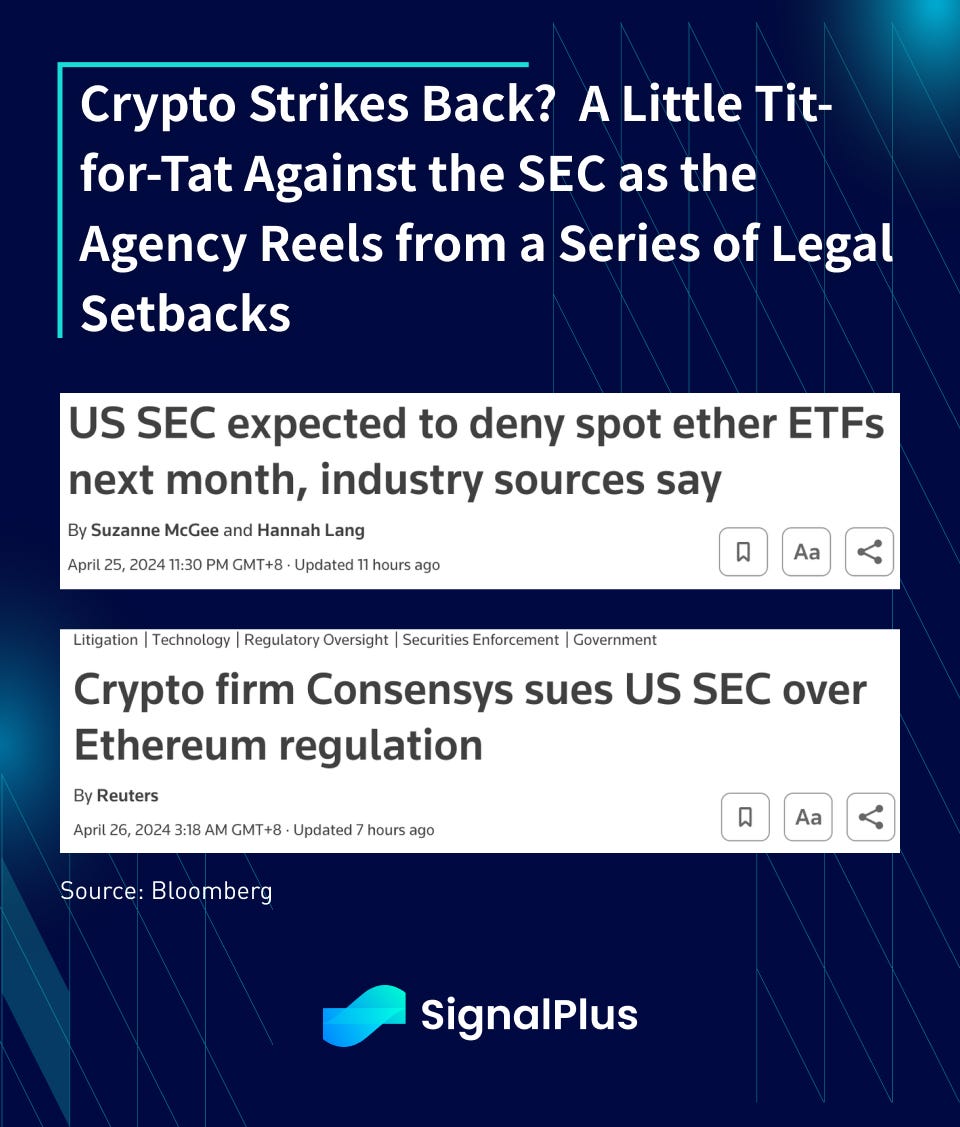

Finally, following reports by the SEC likely to formally reject spot Ethereum ETFs in May, we saw Consensys throw its hat in the litigation rink against the SEC with the complaint alleging that the agency has been “attempting to unlawfully regulate ether through ad hoc enforcement actions against Consensys and possibly others”. Tit-for-tat.

The major takeaway from everything we’ve learned in crypto over the past few years? Always be long lawyers. In fact, be irresponsibly long. Have a wonderful weekend friends.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments