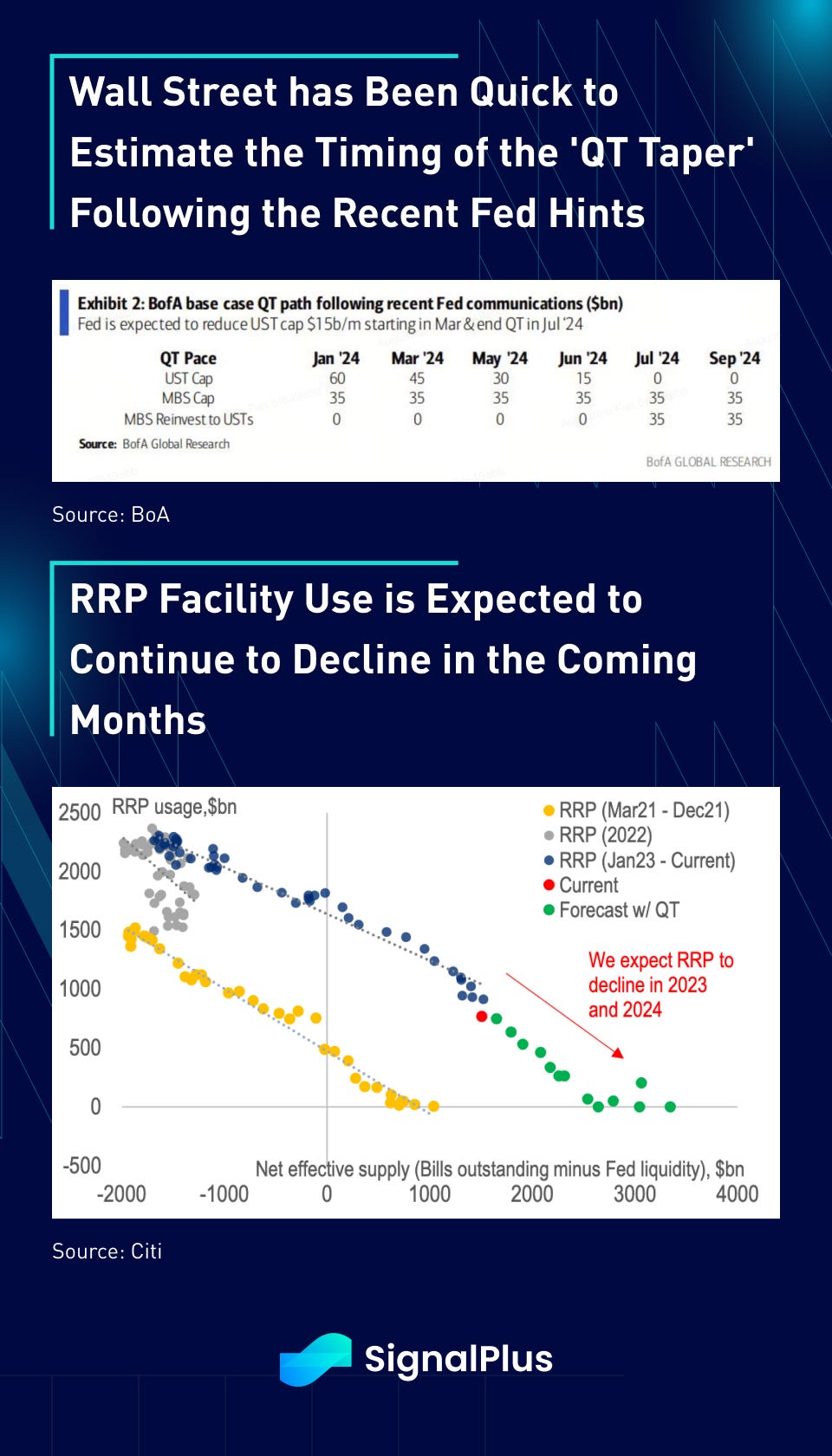

After a first week of busy price adjustments, markets resumed their risk-on tone yesterday, sparked largely by Dallas Fed Logan’s hints that the Fed will be looking to slow down the pace of QT, as they first alluded to in the minutes. Referring to shrinking excess liquidity in the form of declining RRP usage (effectively where mutual fund investors park their excess cash), Logan stated “in my view, we should slow the pace of runoff as ON RRP balances approach a low level” and “normalizing the balance sheet more slowly can actually help get to a more efficient balance sheet in the long run by smoothing redistribution and reducing the likelihood that we’d have to stop [rate hikes] prematurely”.

So not only did we have a ‘Fed pivot’ in December, we are also now presented with a ‘QT Taper’ with unemployment still sub-4% and inflation still well above the Fed’s long-term target. Is it a wonder that everyone is max long risk into the new year?

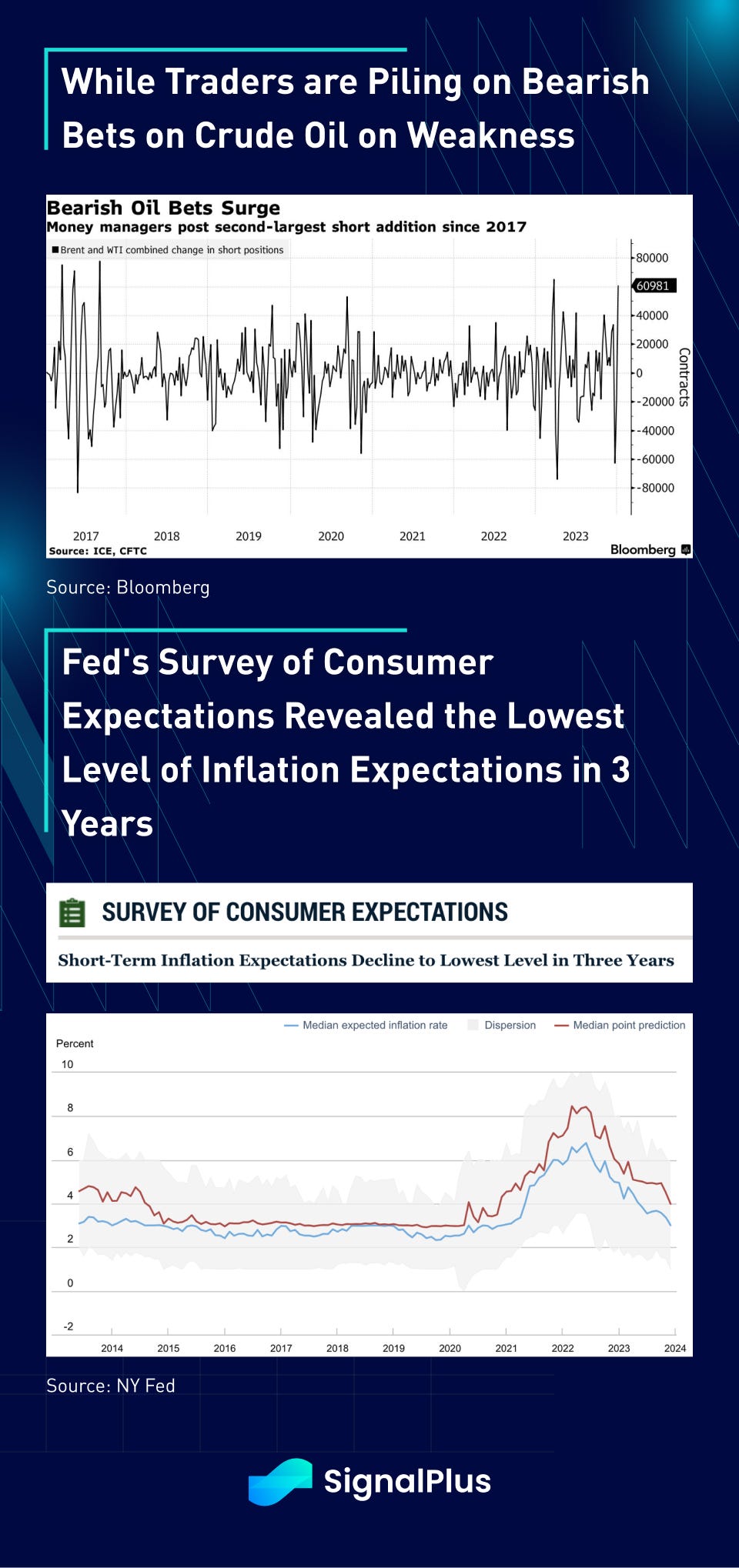

On the inflation side, another aggressive oil price cut from Saudia Arabia (this time for both North American and Asian buyers) sent oil prices down -4.5% and natural gas down nearly 8%, with traders adding to some of the largest shorts in crude oil in over 5 years. Furthermore, the New York Fed’s survey of consumer expectations showed that short-term inflation expectations have declined to the level level in 3 years, with 1-yr expectations falling from 3.36% to 3.01%, and 3-yr expectations falling from 3% to 2.6% in November. Finally, Atlanta Fed’s Bostic mentioned that inflation has come down more than expected, as the Fed continues to open up the narrative for setting up an interest rate cut on the foreseeable horizon.

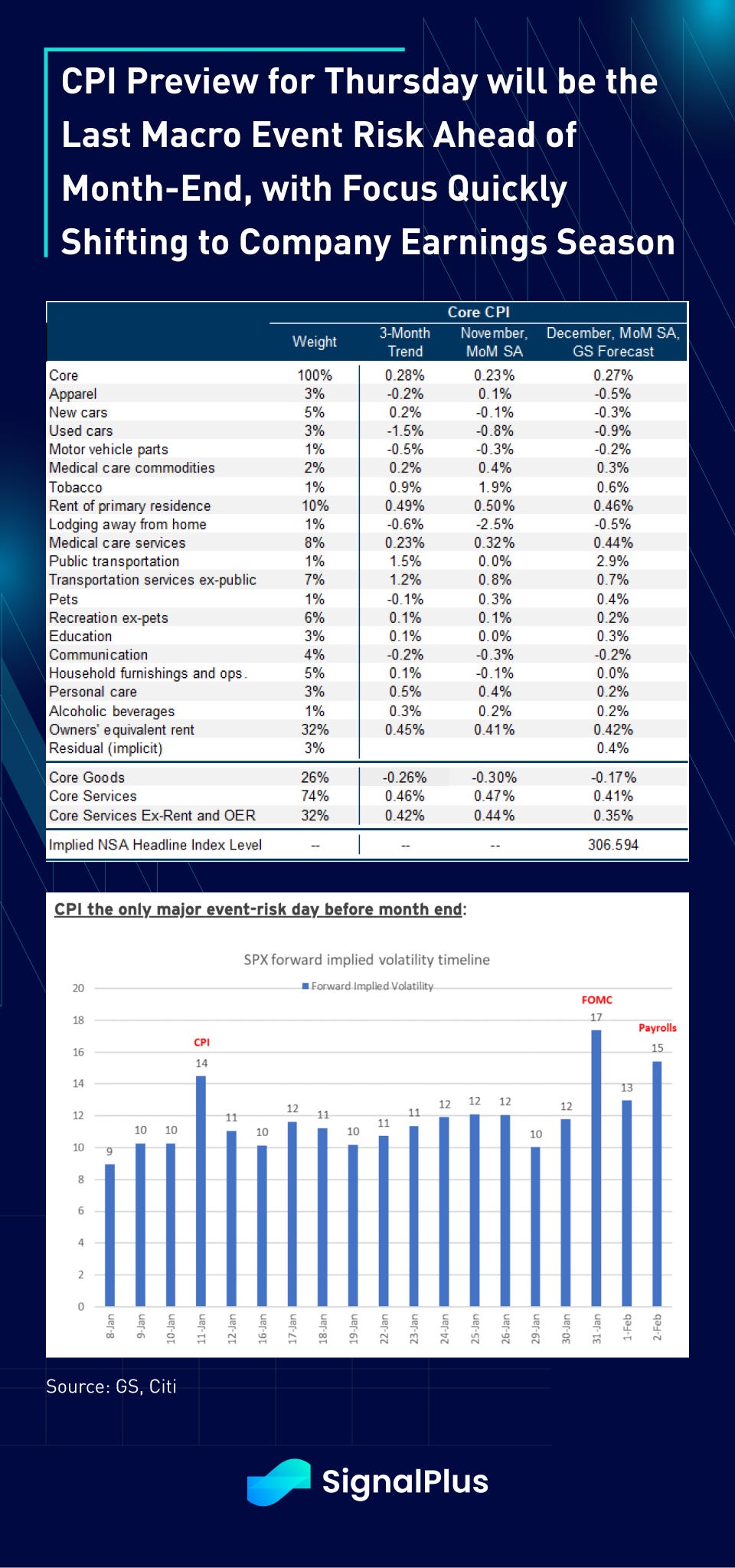

More on inflation, CPI will be due on Thursday where the market is expecting a 0.3% / 3.8% increase in the core, and 0.2% / 3.3%, MoM on the overall headline. Increases are expected to be driven off higher food and energy prices, with shelter prices contributing to the lion’s share of the base increase once again. CPI will be the last macro event risk ahead of month-end, as the market’s focus will pivot to company earnings immediately afterwards until the FOMC on the 31st.

Interestingly, just as the Fed is preparing the market for victory laps on their imminent(?) inflation conquest, investors continue to bid for inflation-protected bonds as the skew appears in favour of a resurgence in price pressures later on in the year. Furthermore, estimates of supply chain disruption pressures (such as from the recent Red Sea attacks) fortell a potentially worrying for inflation ahead, while the recently released German inflation numbers and today’s elevated ‘super-core’ CPI from Japan provide stark reminders that the pendulum might have swung too far the other way on inflation expectations.

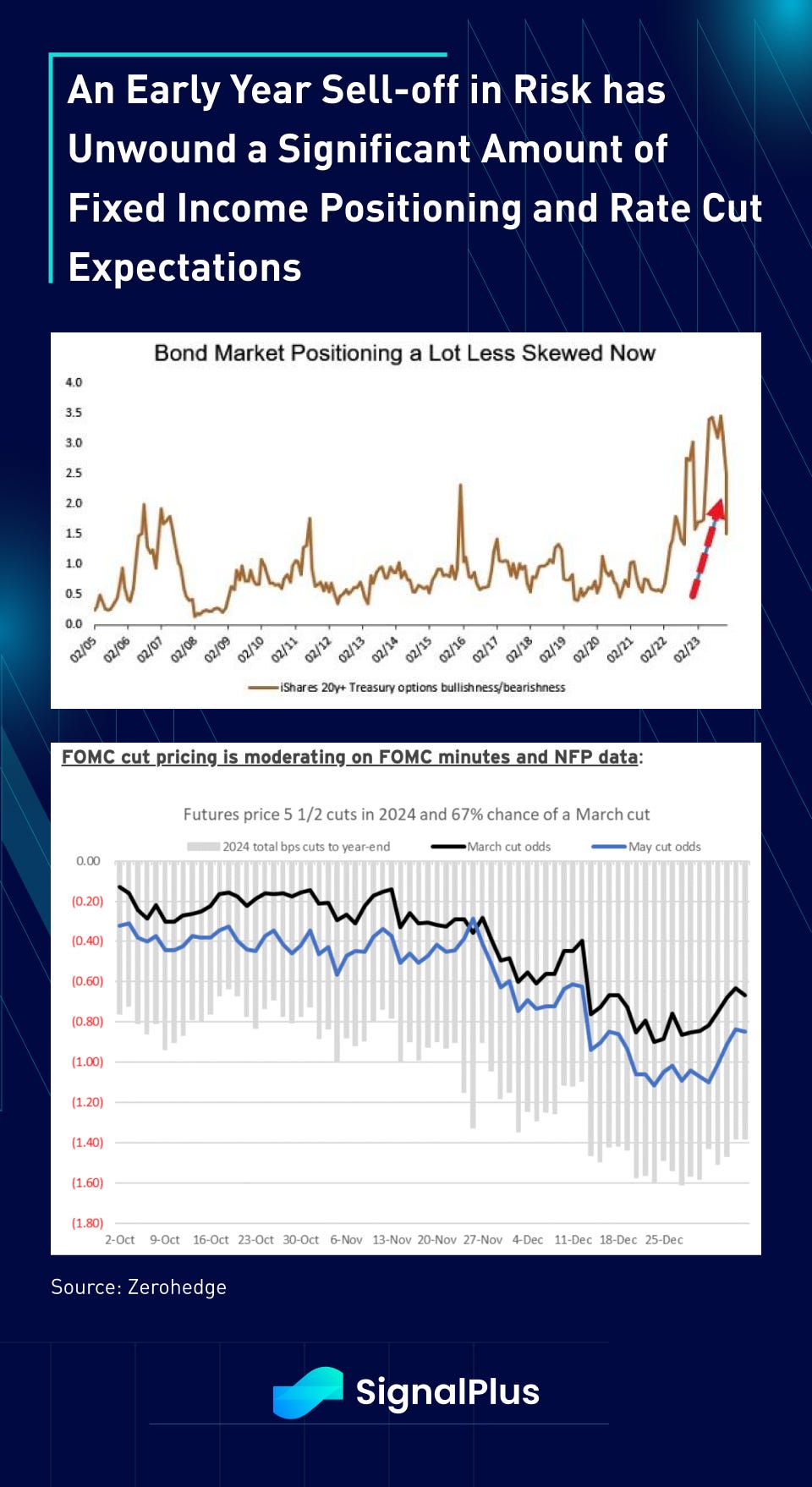

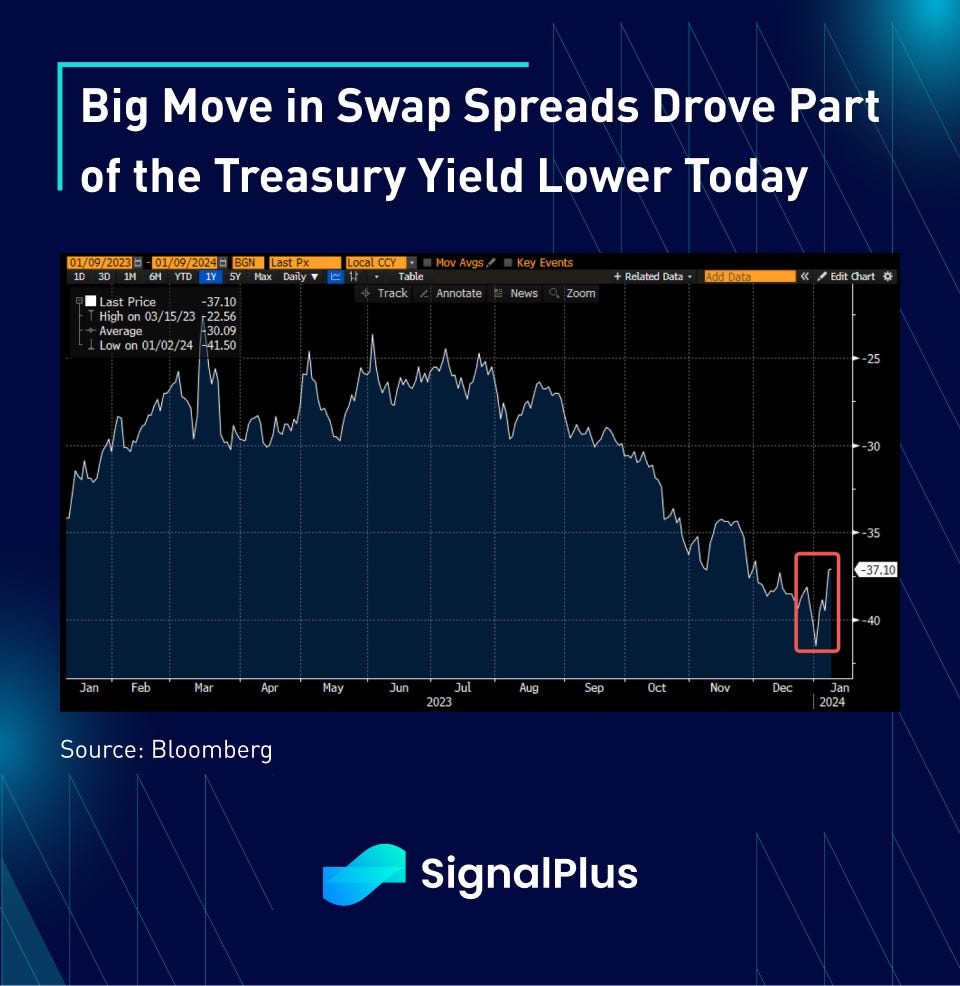

Treasury yields ended roughly 4bp across the curve, despite expectations of a large $110bln in coupon auctions and $30bln in corporate supply issuance this week, with more to come following the banks’ earnings later this week. Part of the yield drop might be in response to the ‘QT Taper’, as 10yr swap spreads (Interest Rate Swaps Less Treasury Yields) have jumped by +8bp since the beginning of the year, potentially marking a secular bottom as the balance sheet reduction era draws to a close.

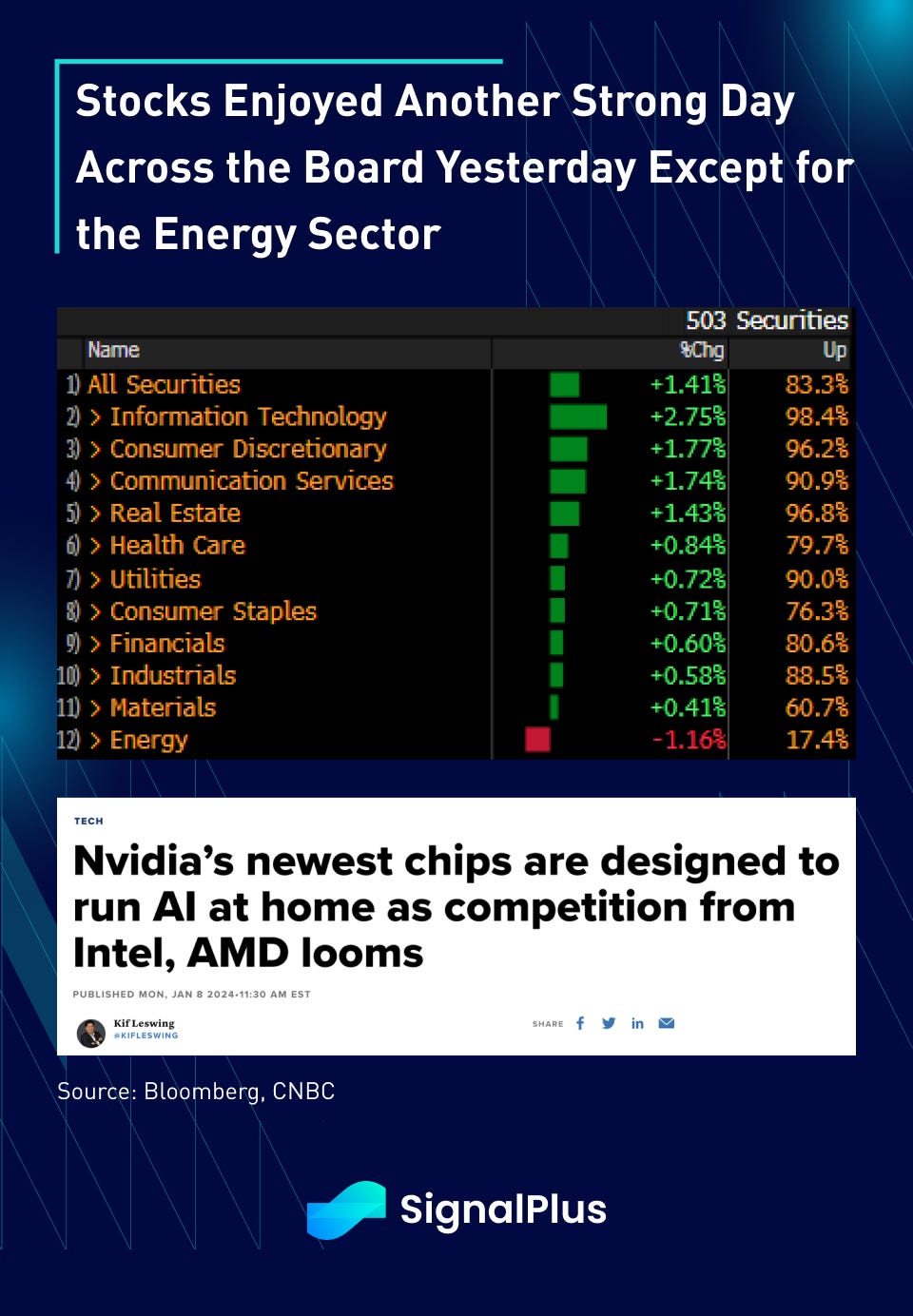

Equities saw a broad rally across sectors, with big tech (as usual) leading the way higher as we had an 83% up-day. All S&P sub-components would have been in the green were it not for the energy sector, which was the odd one out with a -1% sell off following the drop in oil prices. Nvidia helped pace the gains with a +6% day as they unveiled new desktop graphics cards on ‘local AI’ chips (so we can run Stable Diffusion 1.7x faster — yay!), in addition to the announcement that they will be building the H20 chip specifically to cater to the Chinese market while meeting the latest US export restrictions.

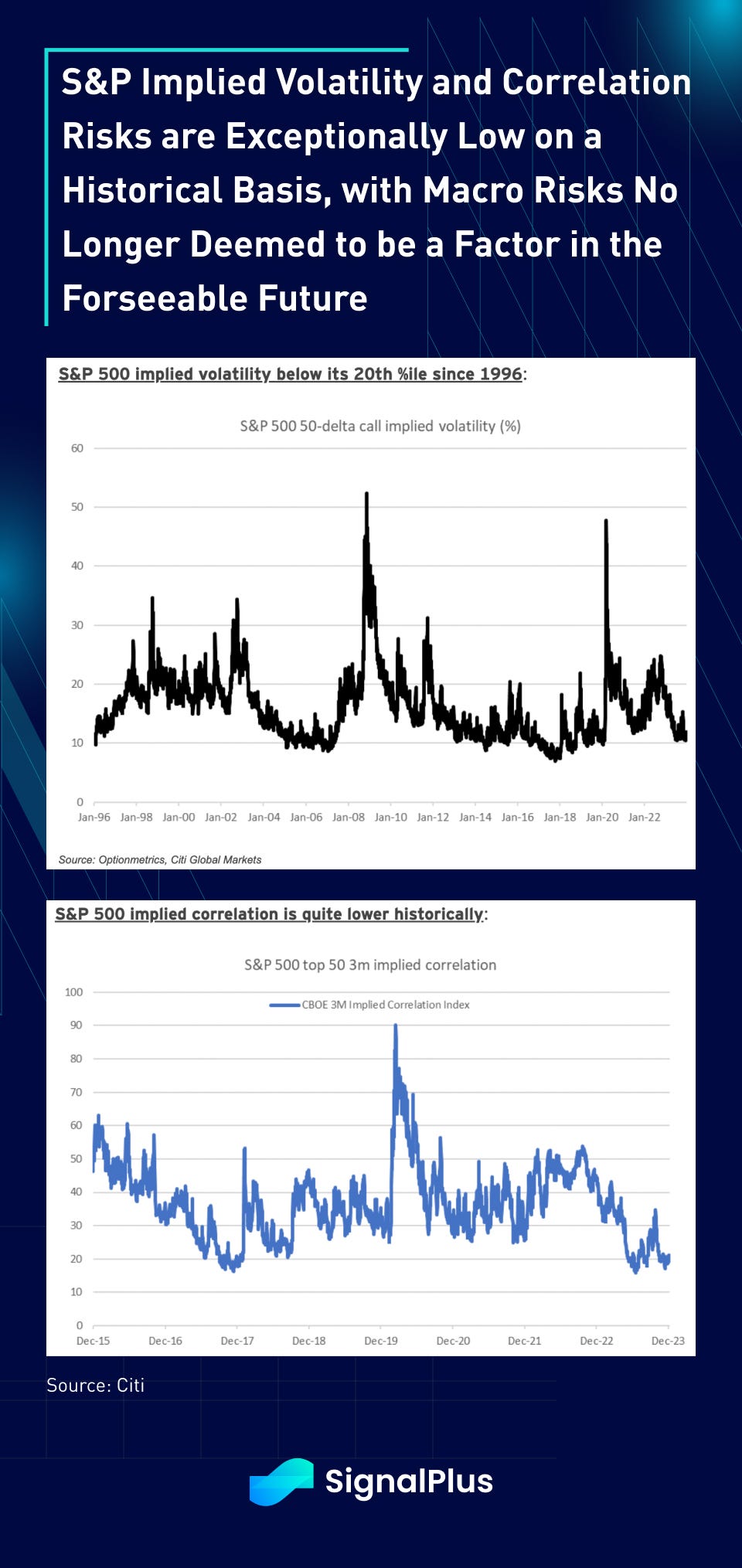

In terms of risk premium, S&P implied volatility has fallen back to its lowest range over the past 30 years, with implied correlation also at historic lows (3rd % percentile since 2006!), suggestions that investors are extremely comfortable and complacent with macro risks at this juncture, with equities strictly focused on company earnings performance in the near-future.

In crypto, BTC has rebounded fully from the earlier sell-off, with prices closing in around $47k and with nearly $200mm in short-futures being squeezed out in the past 24 hours. ETF approval expectations are hitting a cresendo now, with reports of the ETF applicants filing their amended S-1 prospectuses, and former SEC Chair Jay Clayton stating that “approval is inevitable” on CNBC’s Squawk Box yesterday.

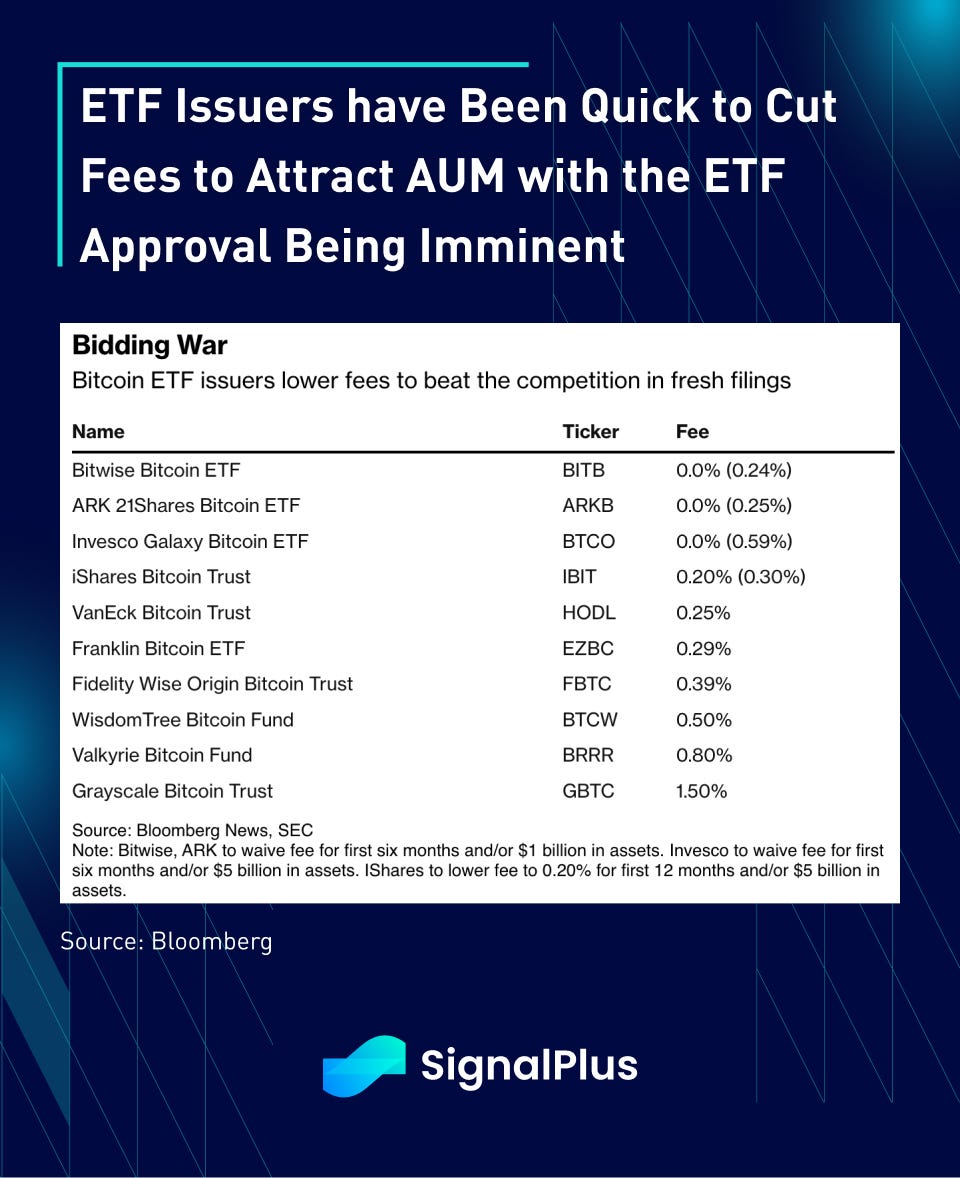

Furthermore, we have been seeing fee war in BTC ETFs with a number of issuers cutting their handling fees to as low as 0.25%, versus 1.5% at Greyscale. We expect Greyscale to remain popular with long-term crypto incumbents as the provider of choice, but would expect most new entrants to gravitate towards the new issuers thanks to the substantially reduced fees, not to mention the ease of usage versus having to on-ramp and custodize with existing crypto infrastructure. A warm welcome to crypto to our TradFi friends who will be joinijng us soon (hopefully)!

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments