Markets continued its quiet but content month-end ways, with Europe continuing the dovish parade on a soft Spanish CPI and the newest ECB member proudly proclaiming that the Central Bank is able to cut rates ‘swiftly’ despite rising wages. In addition, yet another dovish hold from Sweden’s Riskbank added further fuel to rate cut expectations, with nearly 95bp of easing (4x) priced it for the ECB by year-end and around 76bp for the Fed.

Over in the US, Governor Waller gave his speech in the after-hours, continuing his hawkish tone from February with statements such as the “economy is giving us no reason to implement big cuts” and it is “appropriate to reduce the overall number of rate cuts or push them further into the future in response to the recent data”. However, treasury yields were little budged as risk-takers have started to make their long-weekend preparations, while quarter-end rebalancing flows are likely going to dominate price action tomorrow.

Interestingly, Friday will see a release of the PCE deflator with US markets out on holidays, with Wall Street calling for an easing in the PCE core to sub 0.3% MoM, which would be a much welcomed turn after a mini resurgence in core inflation YTD. Markets are unlikely to give the number much heed, with investors enjoying their holidays counting their blessings on a wonderful 1st quarter of returns.

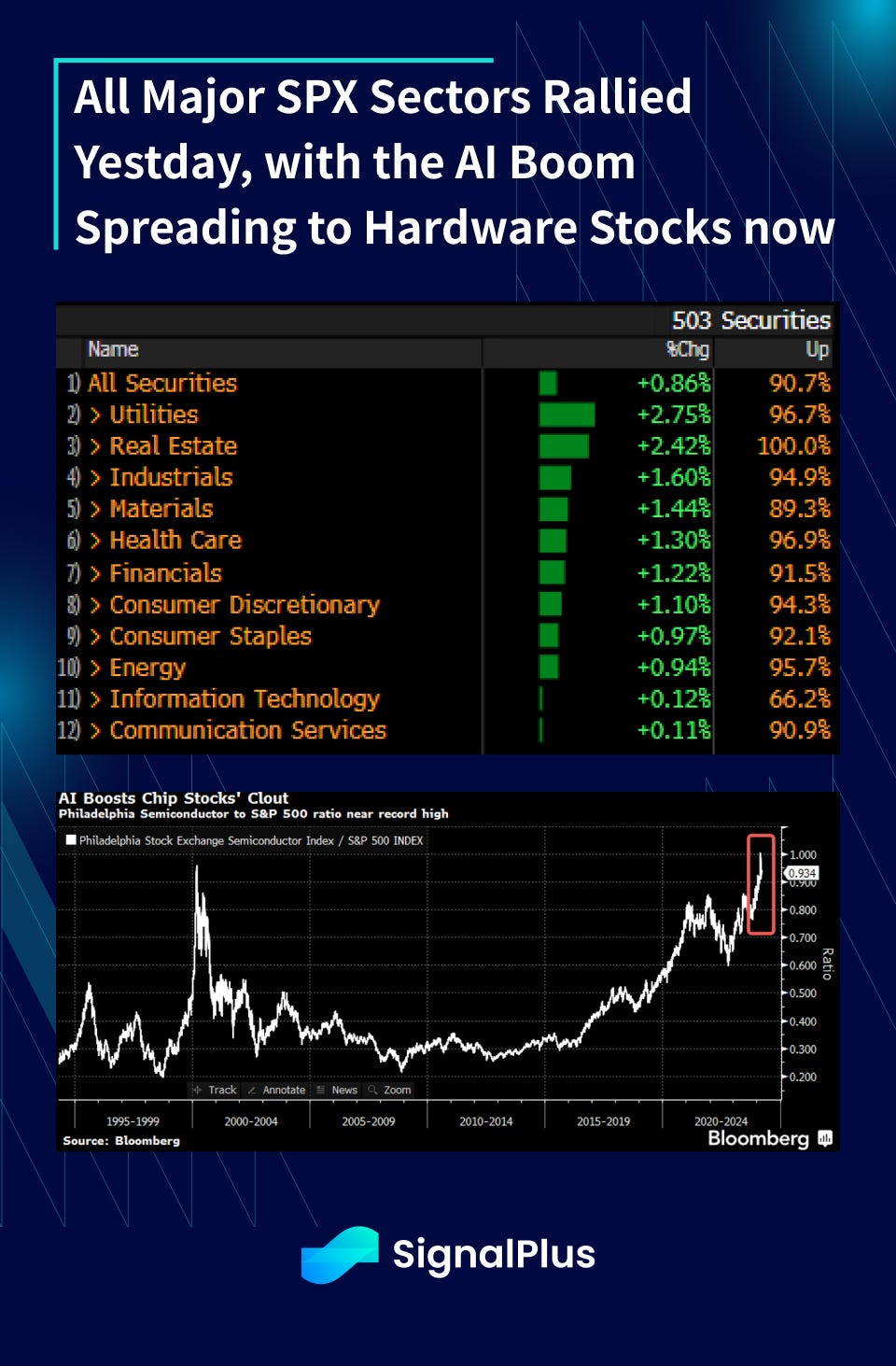

The SPX enjoyed a 91% up-day yesterday, with all major sectors in the green as the party rages on. With Nvidia showing some interim fatigue, the AI rally has started to spread towards hardware with the Phillyl Semi-conductor index now outperforming the SPX at a pace last seen during the dot-com days. Moreover, on a one-year look-back, US stocks are leading global stocks on a risk adjusted basis with a 1yr Sharpe ratio of nearly 3x. This is an unfathomably strong feat given the mega market cap of constituent companies, highlighting the tremendous wealth effects that have been generated on this incredible bull market run.

In crypto, we saw some price volatility around the NY open with BTC prices spiking to nearly 72k before reversing course to a low of $68.5k, coinciding with a choppy open on the Coinbase stock ($267 → $278 → 256 within minutes). The volatility was likely due to a US district judge’s ruling that the SEC’s case against Coinbase will indeed go to trial, where the latter is being accused of engaging in unregistered sales of securities. The stock traded lower by -2.5% yesterday and weighed on BTC sentiment for much of the session, though ETF inflows were positive again with +418mm added on the day.

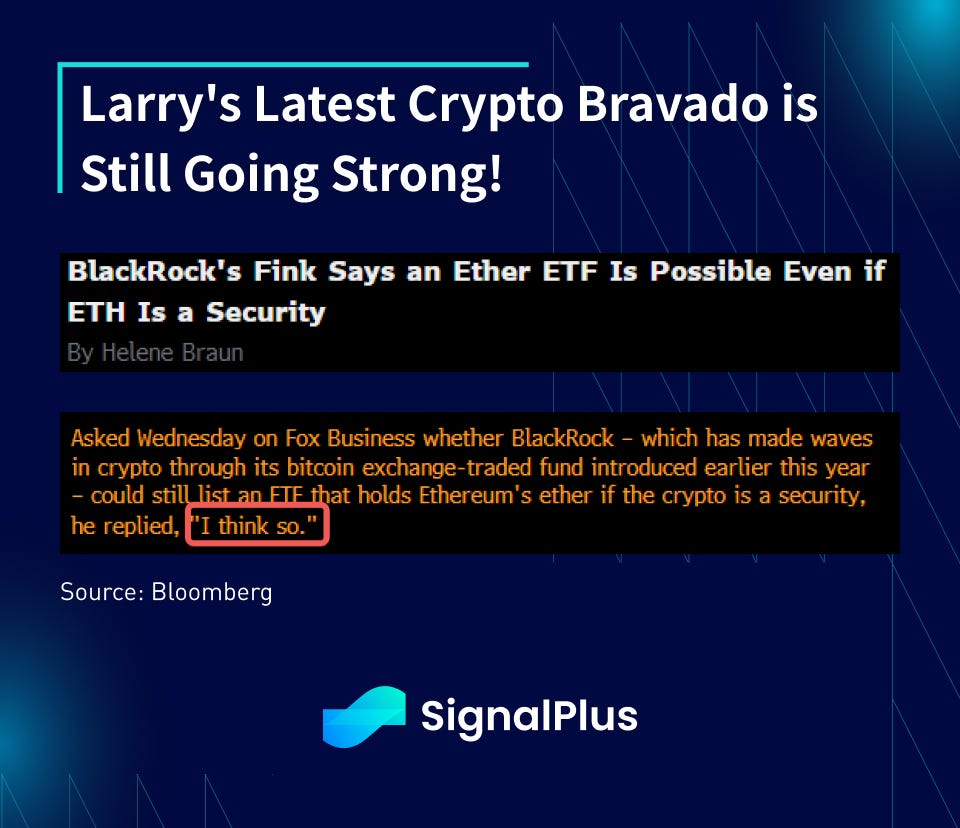

Finally, during an interview with Fox Business, Larry Fink continued his recent bravado on crypto by stating his belief that the SEC could still approve the Ethereum ETF even if the agency deems the token to be a security. Wouldn’t it be helpful if Blackrock, SEC, and the CFTC could just together in a room and sort it out nicely between the group of them?

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments