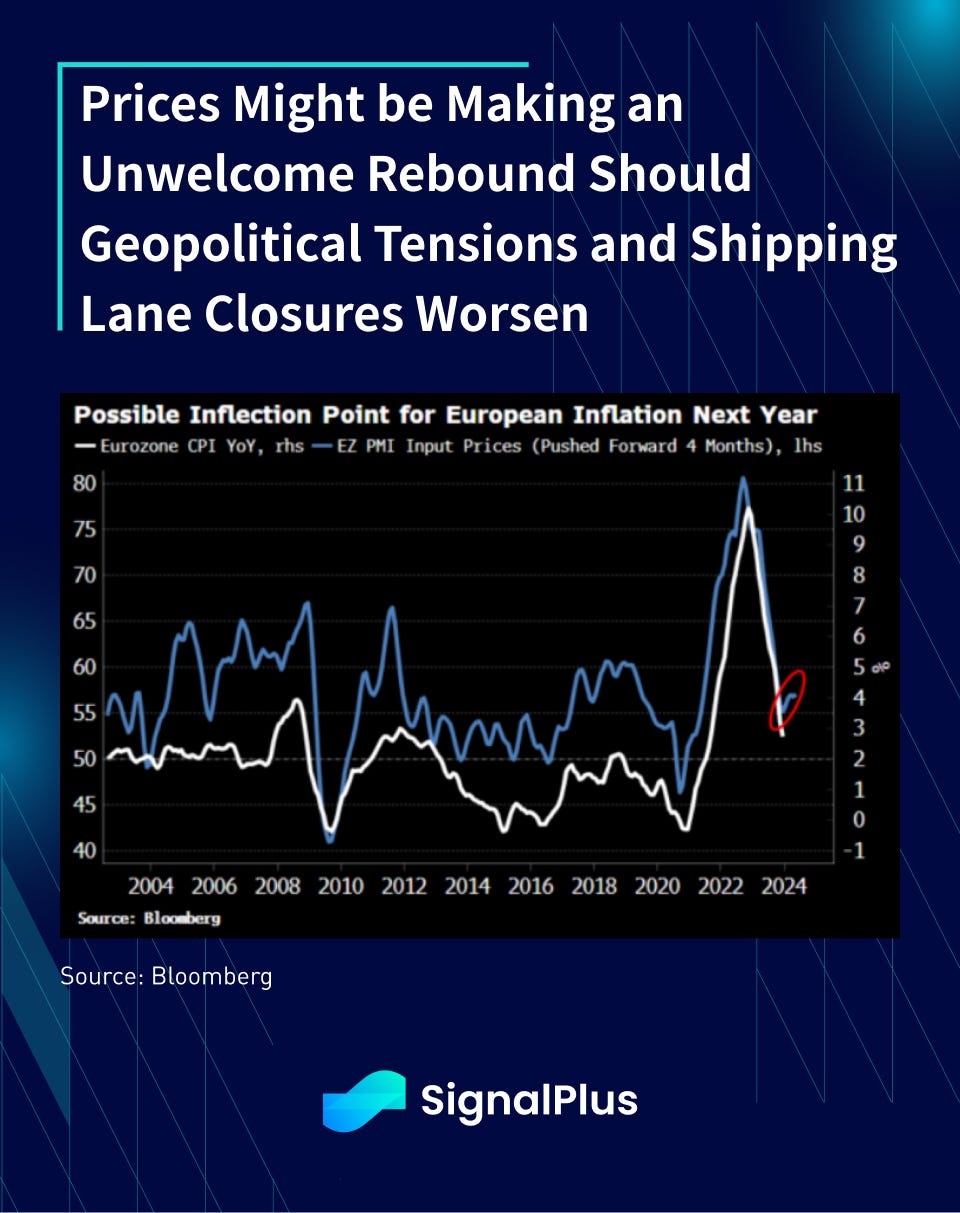

The ECB kept rates on hold for the 3rd straight meeting, though President Lagarde managed her own dovish pivot with a couple of key omissions and new statements. The ECB communique omitted a previous line which stated “domestic price pressure remain elevated… owing to growth unit labour costs”, while Lagarde stated during the press conference that “the disinflation process is at work”, and that price pressures would “ease further over the course of the year”. Furthermore, while she further reiterated that the council deemed it to be “premature to discuss rate cuts”, she hedged the comment by stating that such a move was “likely” in or by the summer, when the economy could progress further along the “disinflation process”.

Similar to the US, where policymakers have made explicit pivots and declared early victories against inflation, there are signs that input prices might have made a short-term bottom, and we might be dealing with an inconvenient rebound in the near future, especially if the shipping lane shutdowns and jump in oil prices continue to worsen.

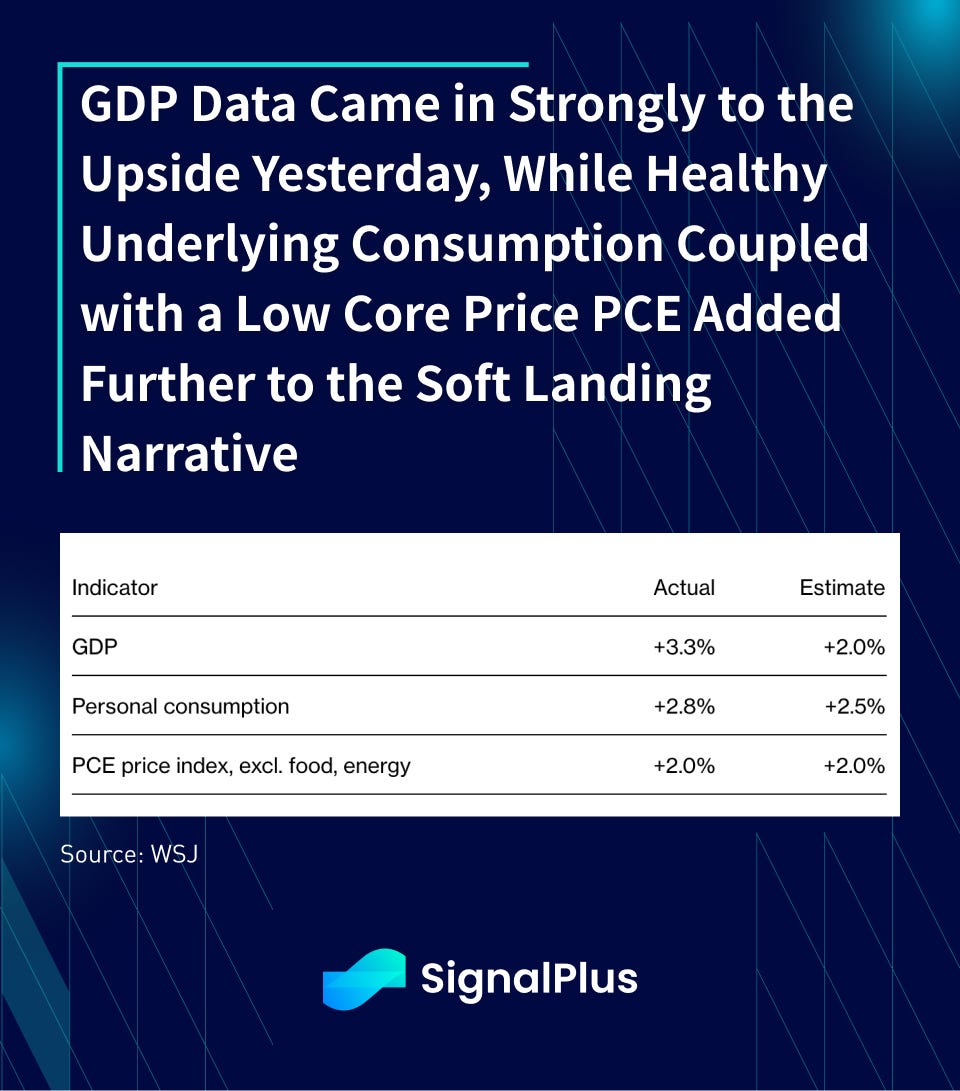

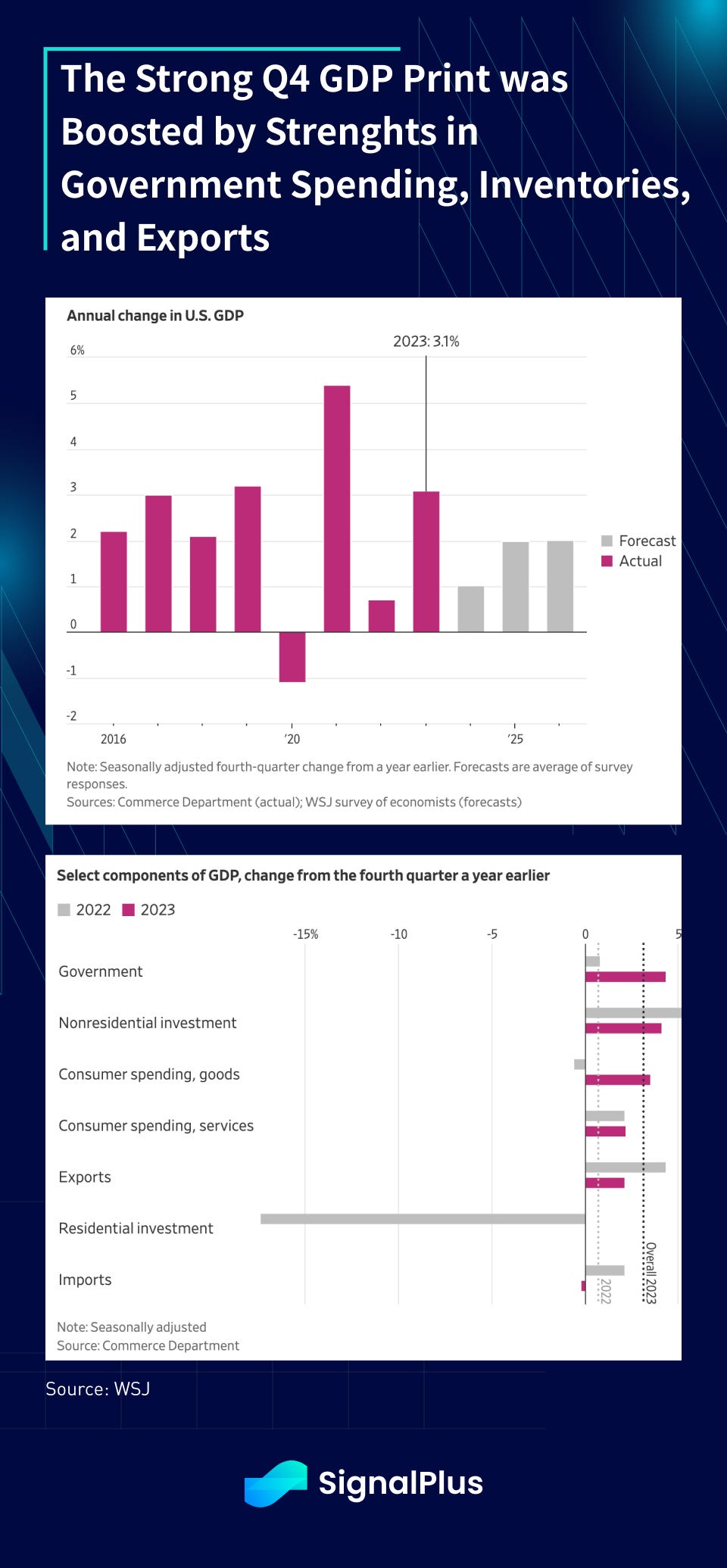

In the US, Q4 economic data gave markets a stern reminder of how strong the US economy has been, with Q4 GDP coming in at 3.3% vs 2.0% expected for a sizeable upside beat, with personal consumption also coming in above expectations. Strong government spending, inventory build-up and positive net exports constituted the majority of the upside, with final demand staying on target.

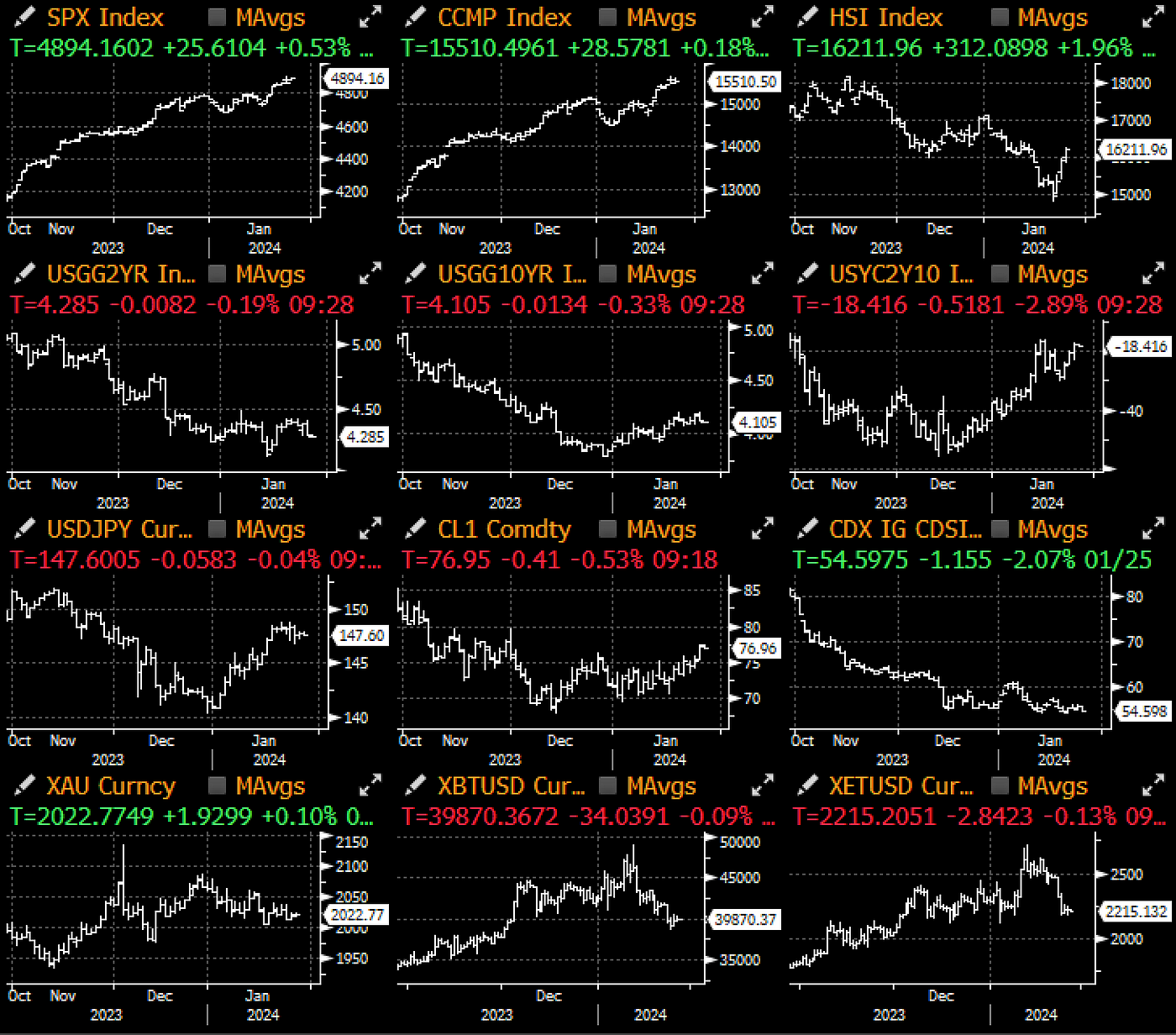

The Fed and bond markets notched another win yesterday in its soft-landing narrative, with stronger GDP, robust consumption, disinflation price pressures, and further signs of a gently easing labour market (initial claims +27k on the week) pushing yields lower in a bull steepening manner. Furthermore, a dovish ECB in Europe, rescue support packages from China, and a soft inflation miss in Tokyo CPI today are working in conjunction to keep asset prices, with the S&P 500 hovering around ATHs despite a -11% slide in Tesla and bleak revenue forecasts from Intel in the afterhours.

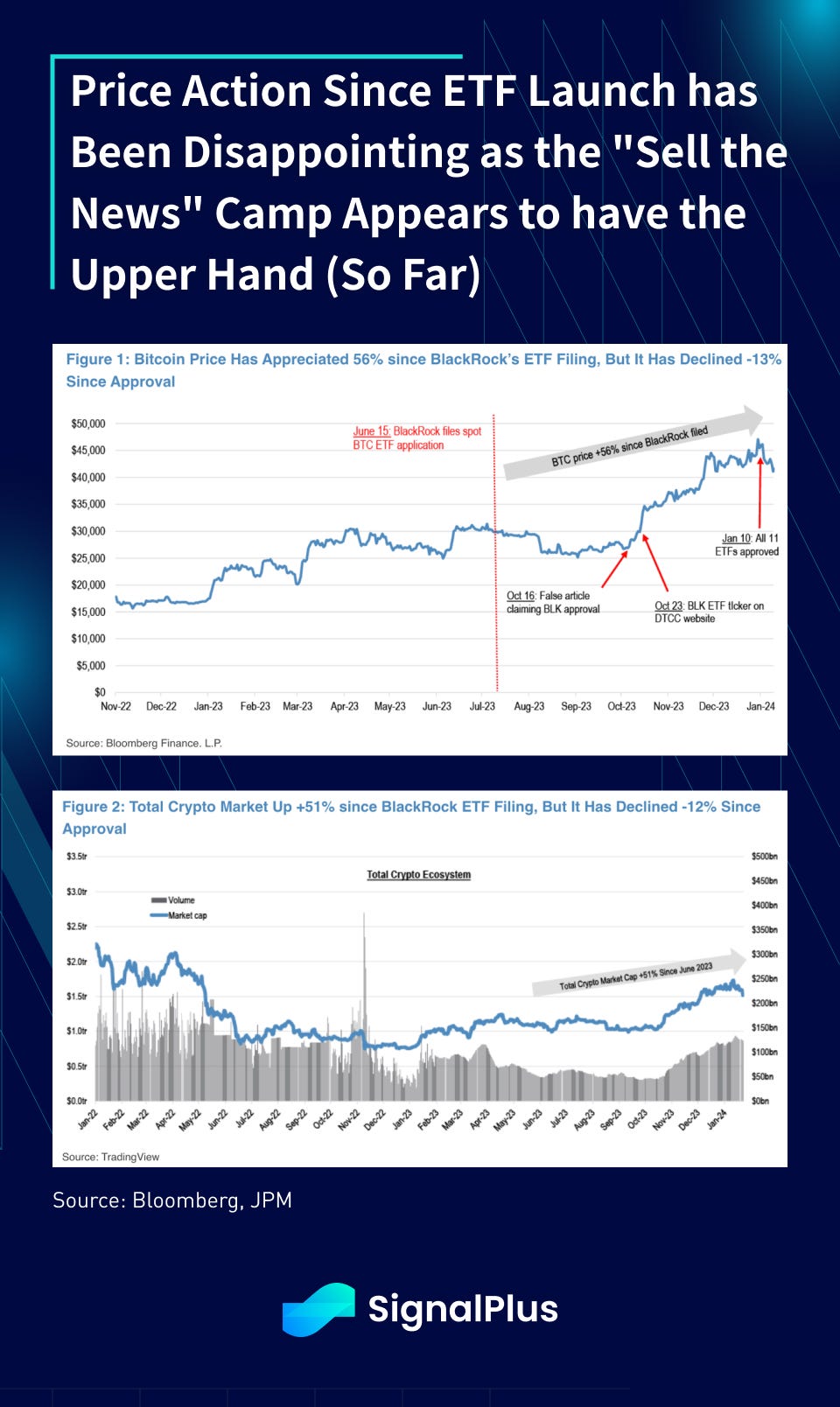

As the dust settles on the spot BTC ETFs, the verdict has started to turn more negative, with the disappointing price action follow-up as Bitcoin struggles to remain above $40k.

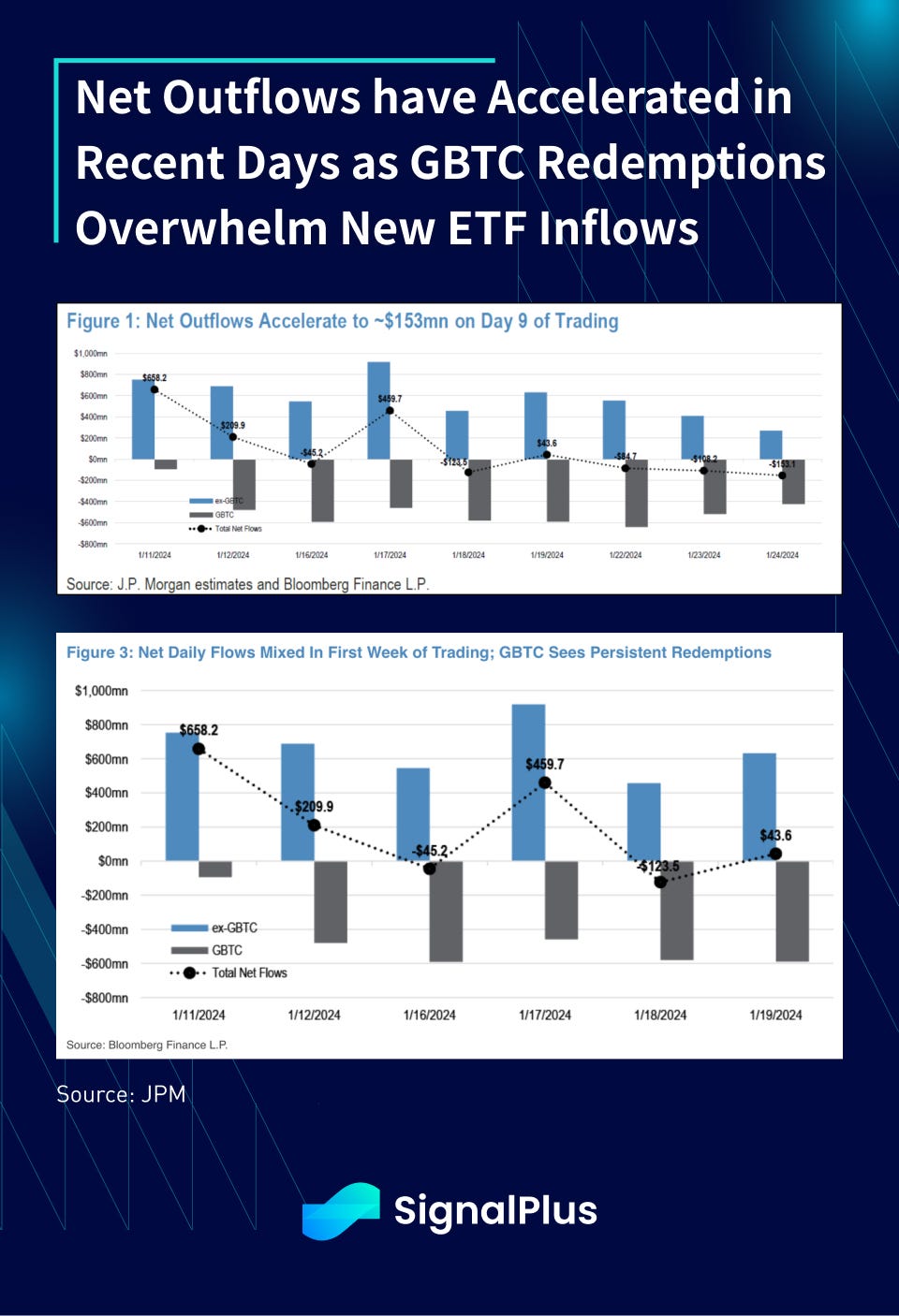

Net outflows have accelerated to ~$153mm after the first 9 days of trading, compared to +$1.2bln of inflows after the first week. JPM did a benchmark comparison of the BTC spot ETFs vs the GLD launch (gold ETF), where the latter only managed to raise $3.5bln of inflows after the 1st year of launch, well short of the $10-$50bln of forecated inflows that have been touted from various corners of the crypto-sphere. The post 1-week performance of spot ETF inflows have also lagged GLD thus far, weighted heavily by the persistent redemptions out of GBTC.

With large MTM gains that remain to be realized out of long-term GBTC holders, as well as the super-high fees charged by Grayscale versus the new spot ETFs, one should probably expect GBTC outflows to continue for the foreseeable future, and the current defensive sentiment to remain for quite a while longer.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments