Market sentiment remains undecided and influx with a number of diverging headlines and developments across different regions. China started the day with first signs of a ‘liquidity put’ with a proposed market rescue package in the form of more equity buying support via their offshore capital pool (back to the QE game we go), and an Asian-based HF made headlines on their fund closure after wrong-footed bets on China vs Japan. The CIO is an experienced veteran with decades of market experience, and his heartfelt admission of losing confidence offers a stark reminder that macro is a tough beast to tame, outlasting even the most experienced of us.

Speaking of Japan, 10yr yields have jumped 18bp from the lows of this month, with another jump over the past 2 days as BoJ Governor Ueda has put rate hikes firmly back on the menu for April. Ueda’s press conference on Tuesday stated that the BoJ will ‘mull’ if negative rates should be kept if “price goal is in sight”, and that labour unions have been asking for higher pay hikes in their wage talks. He also believes that the BoJ can avoid “discontinuity” in ending their NIRP policy, though traders are paying attention to any pushback stories from the press that might soon follow, as has been the since Ueda took office last year.

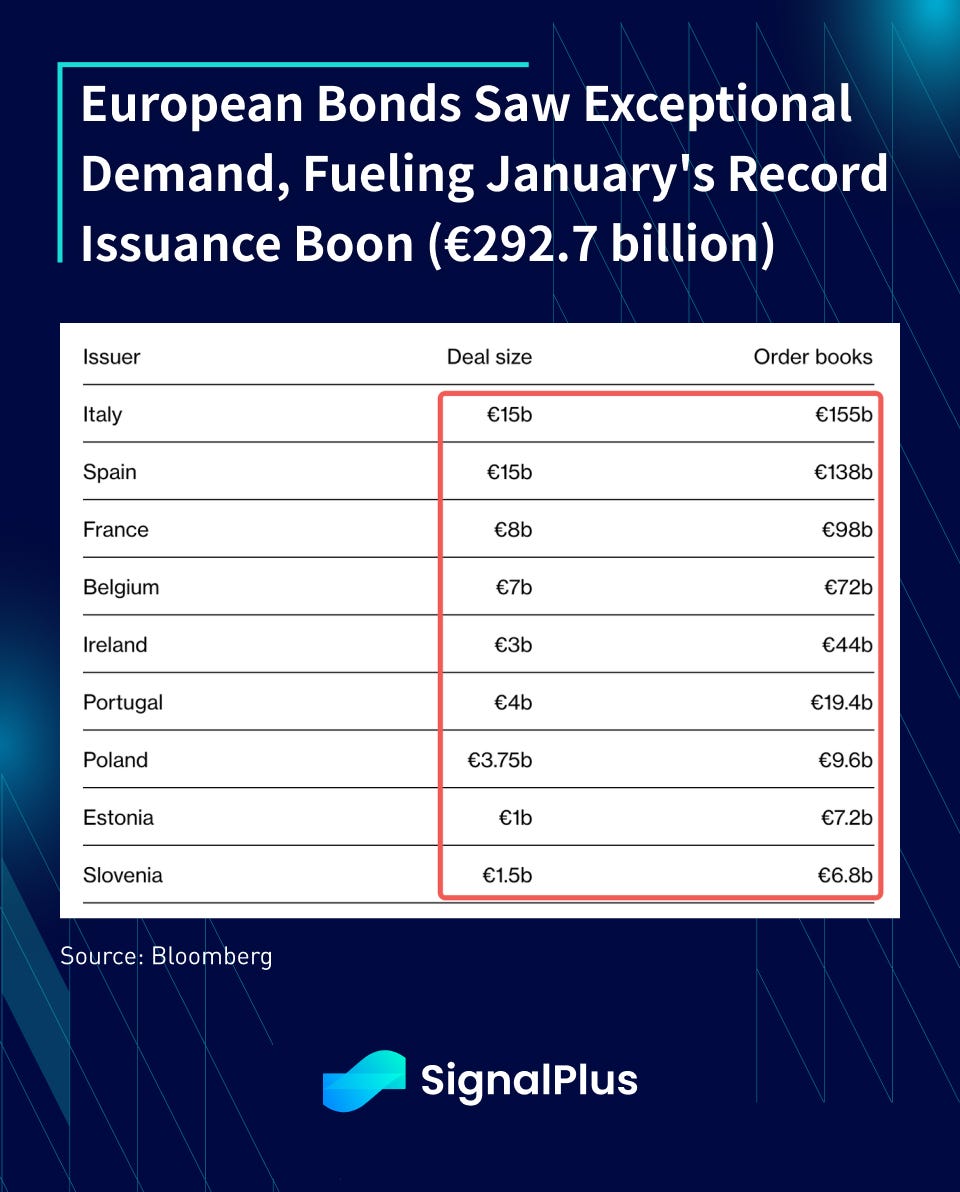

Back in Europe and US, European bond markets notched a new January issuance record with around $320bln of new debt issuance, which were incredibly well received for the most part, with >80% of new deals seeing spread tightening (ie. higher price) post pricing.

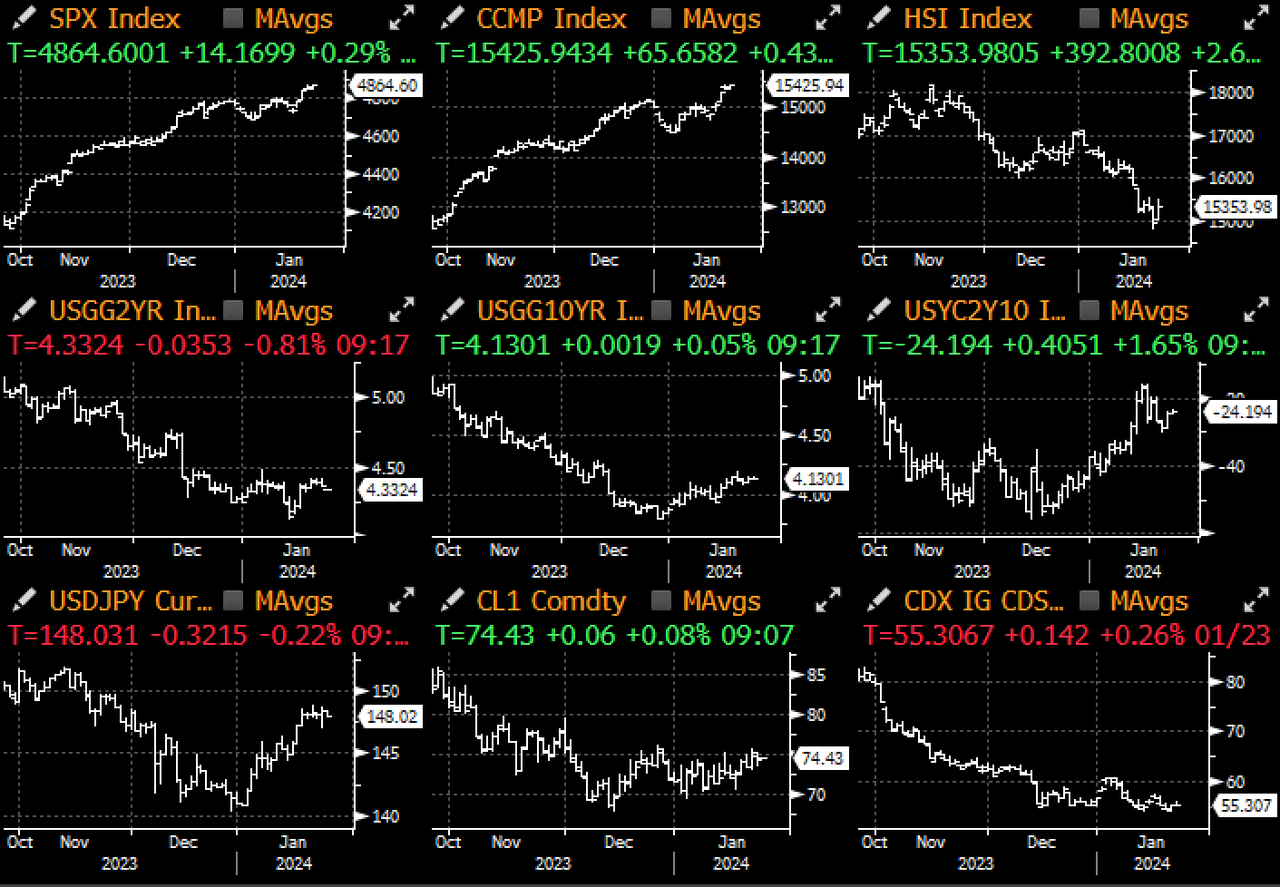

In the US, the record 2yr treasury auction ($60bln in one single clip) also saw decent demand, with the issue clearing right on the screens at 4.365%, with over $154.2bln in bids for a 2.57x cover, with dealers taking the lowest amount at 14.8% since last July. A decent result overall, considering the recent re-emerging concerns on inflation as oil prices have been rebounding.

Markets were quiet overall as we await a very busy week next week ahead of the Fed, Treasury QRA, NFP and month-end. Earnings will also be in full blown mode, so traders are understandably keeping their powder dry this week. Equities and bonds have also reverted much of its negative correlation they enjoyed over the past 6 months (a requirement for portfolio diversification benefits), and their resumption towards zero (or worst, positive) might exacerbate asset pricing moves in February, reminiscent of the 2Q2023 sell off and much of 2023. The easy part of the risk-on trade looks to be over in the near-future.

Speaking of a waning honeymoon, crypto prices continue to be weak as it’s been more of the same with GBTC outflows weighing heavily on markets. Lack of near-term catalysts and inflows (those will happen over months and quarters, not days as we’ve written) are causing mercurial traders to lose faith in the short-run, with long-future liquidations picking up steadily over the past few days.

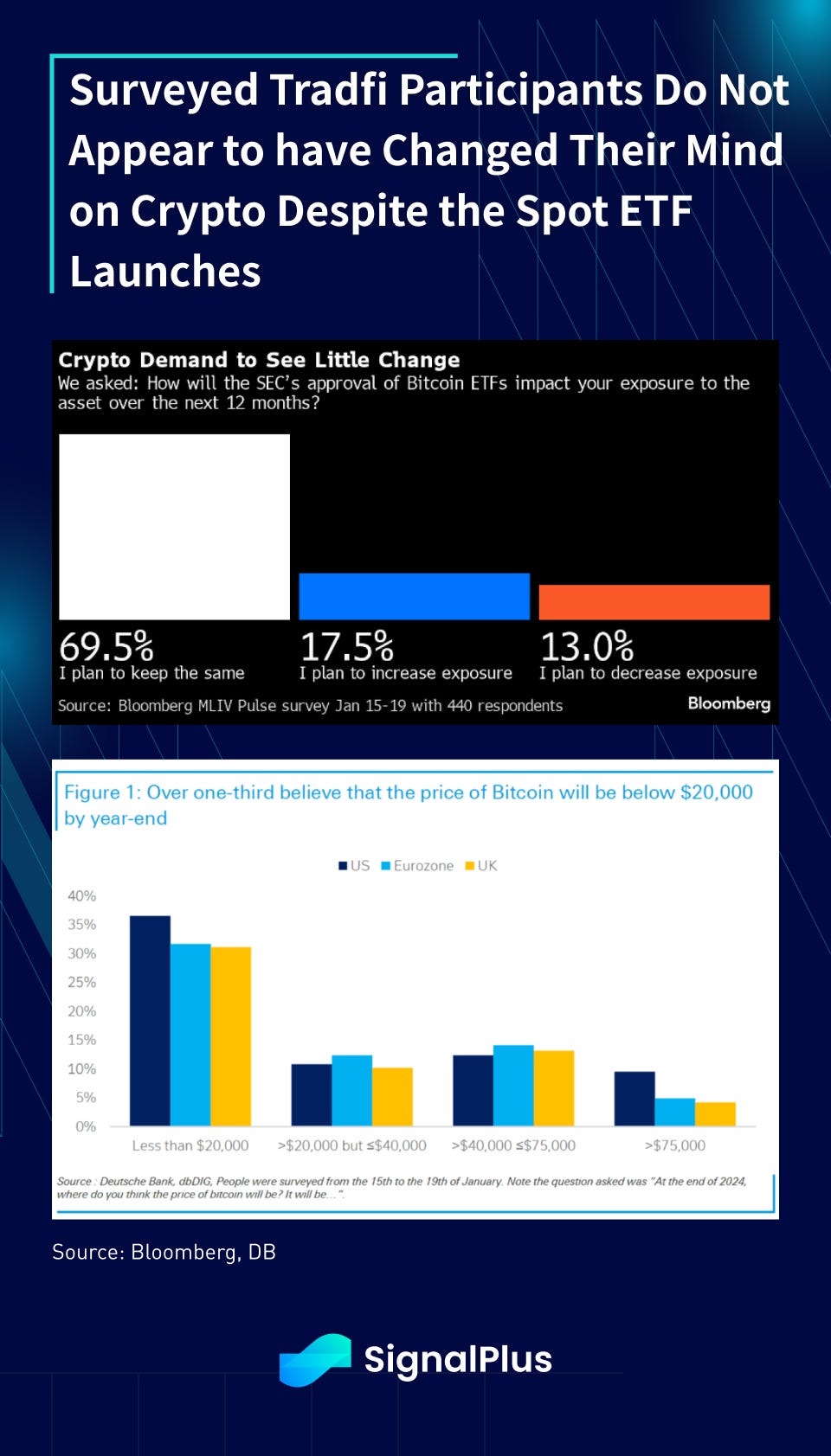

Furthermore, just as we thought Tradfi was starting to be on our side, a number of published surveys from Bloomberg and sell side seem to suggest little near term demand or change in sentiment from the wider public towards crypto in general, where ETFs can be summed up to increase the legitimacy, but not the use-case story for digital assets. 1/3 of those surveyed by a Deutsche Bank survey apparently still believes that BTC will be sub-20k by year-end (they should buy some cheap puts!!!!), definitely an interesting response versus expectations from native participants. The road ahead of us is still very long, it would seem!

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments