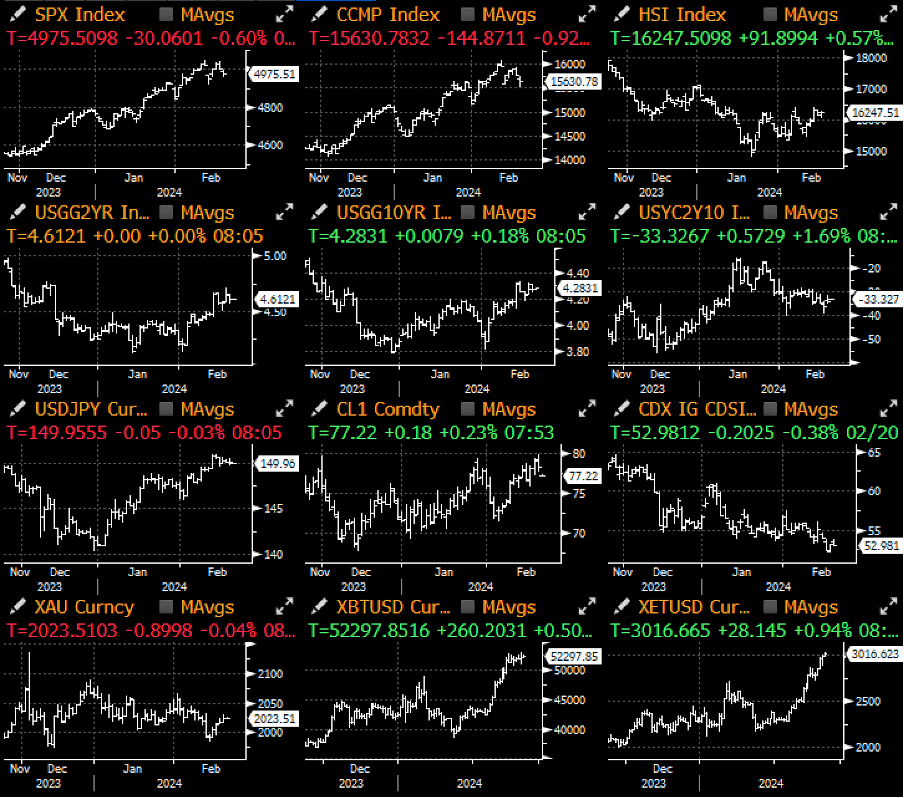

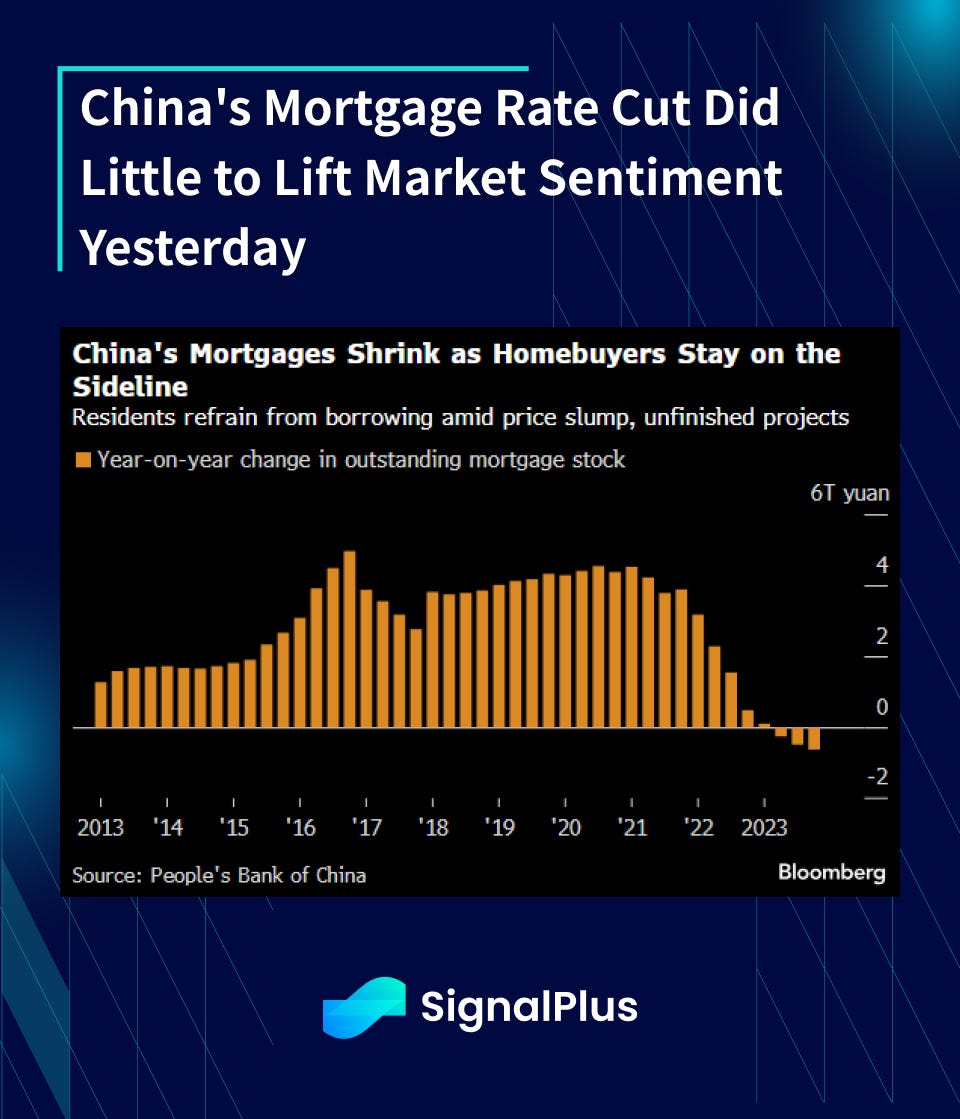

Markets started yesterday’s session with a mortgage rate cut out of China as they continued with piecemeal plans to stimulate their economy. The 5yr loan prime rate was cut by 25bp to 3.95%, the first cut since last June and largest cut since 2019. However, the move failed to impress investors overall, with the CSI 300 ending the day just 0.2% higher and bond yields failing to make new lows. Markets continue to see these measures as just baby steps towards trying to address bigger structural issues, as low housing demand is much less about the price of credit than the supply-demand imbalance and depressed economic outlooks.

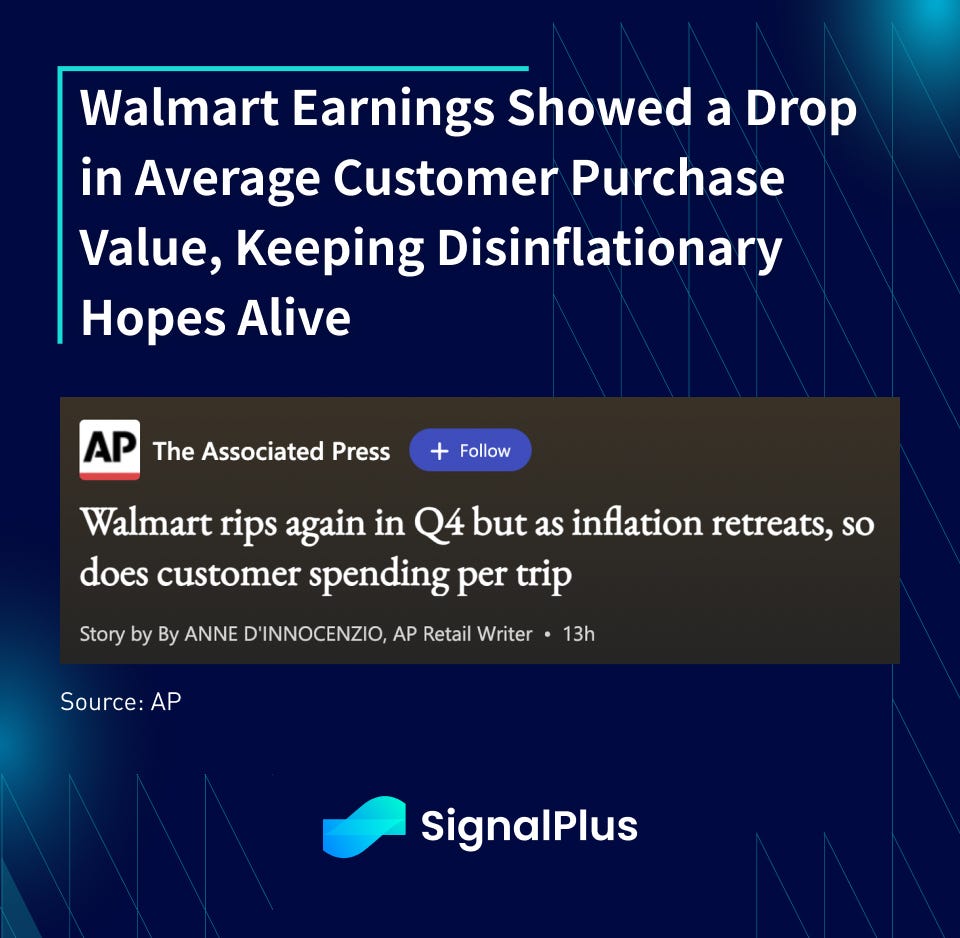

In the US, softer than expected CPI out of Japan and Canada, a dovish BoE’s Bailey (don’t need inflation to come back to target before they can cut rates), but a heavy $50bln of IG corporate supply pivoted the treasury curve steeper. Furthermore, Walmart’s earnings showed a -0.3% drop in average consumer spending ticket, despite a 4.3% rise in transactions, signaling a downshifting in dollar value purchases and giving markets hope that the disinflation narrative is still well and alive.

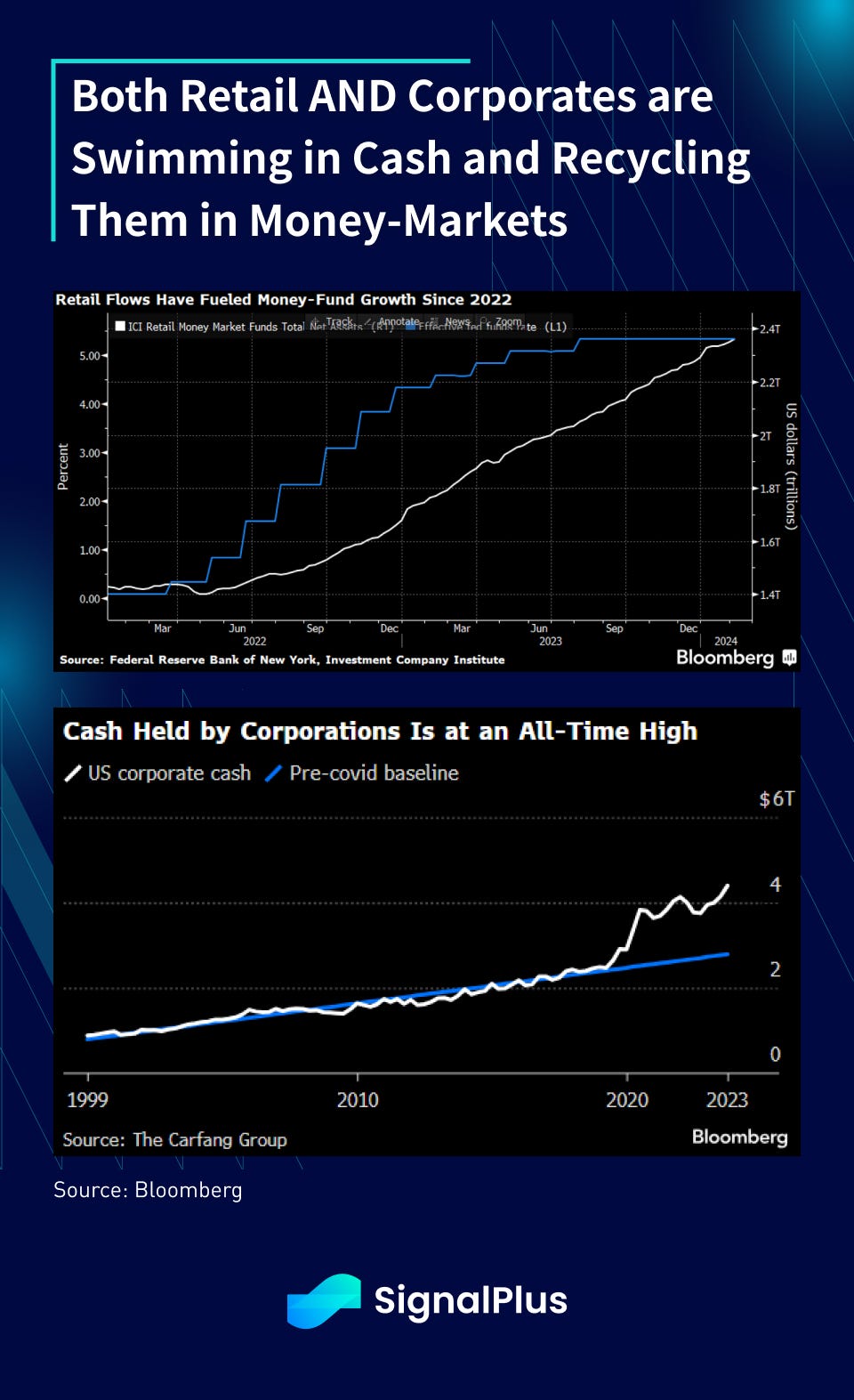

Over in equities, the rolling correlation between bonds and equities has continued to weaken in February, with equity prices staying close to all time highs, while bonds have been battered by a repricing of rate-cut expectations (higher for longer) over the past 6 weeks. Interestingly, as one of the key points we are paying attention to in 2024, investors continue to plow into money market funds with yet another $128 billion added to US money market funds since the start of the year, with total assets now balloning to a massive $6 Trillion — 3x crypto’s total market cap!

Furthermore, it’s not just moms-and-pop that are putting $ into savings accounts, but corporates are also sitting on a record $4.4 trillion of cash and recycling them into T-bills. As such, it’s hard to be too bearish risk assets and equities, outside of a trade, against this ocean of liquidity support in the US.

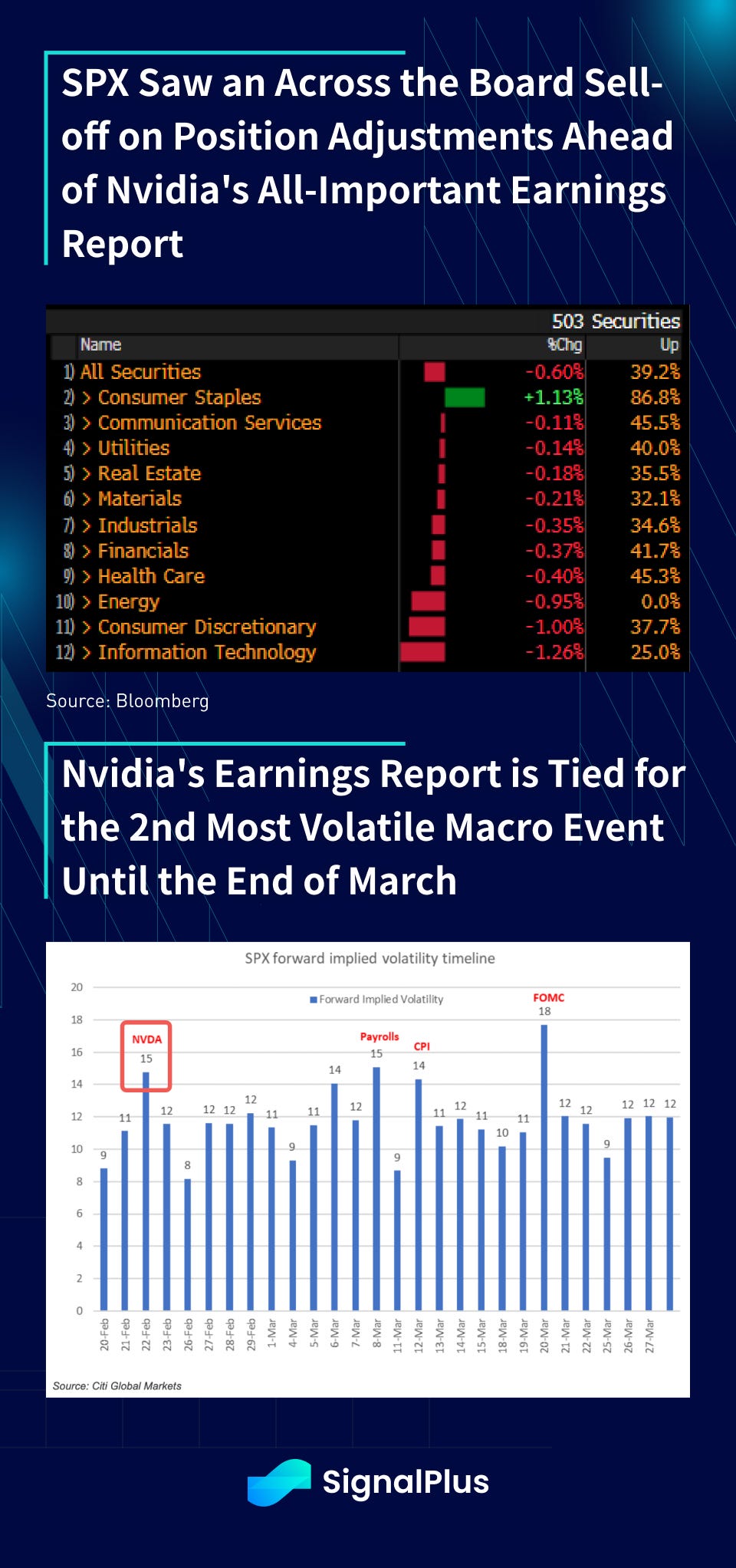

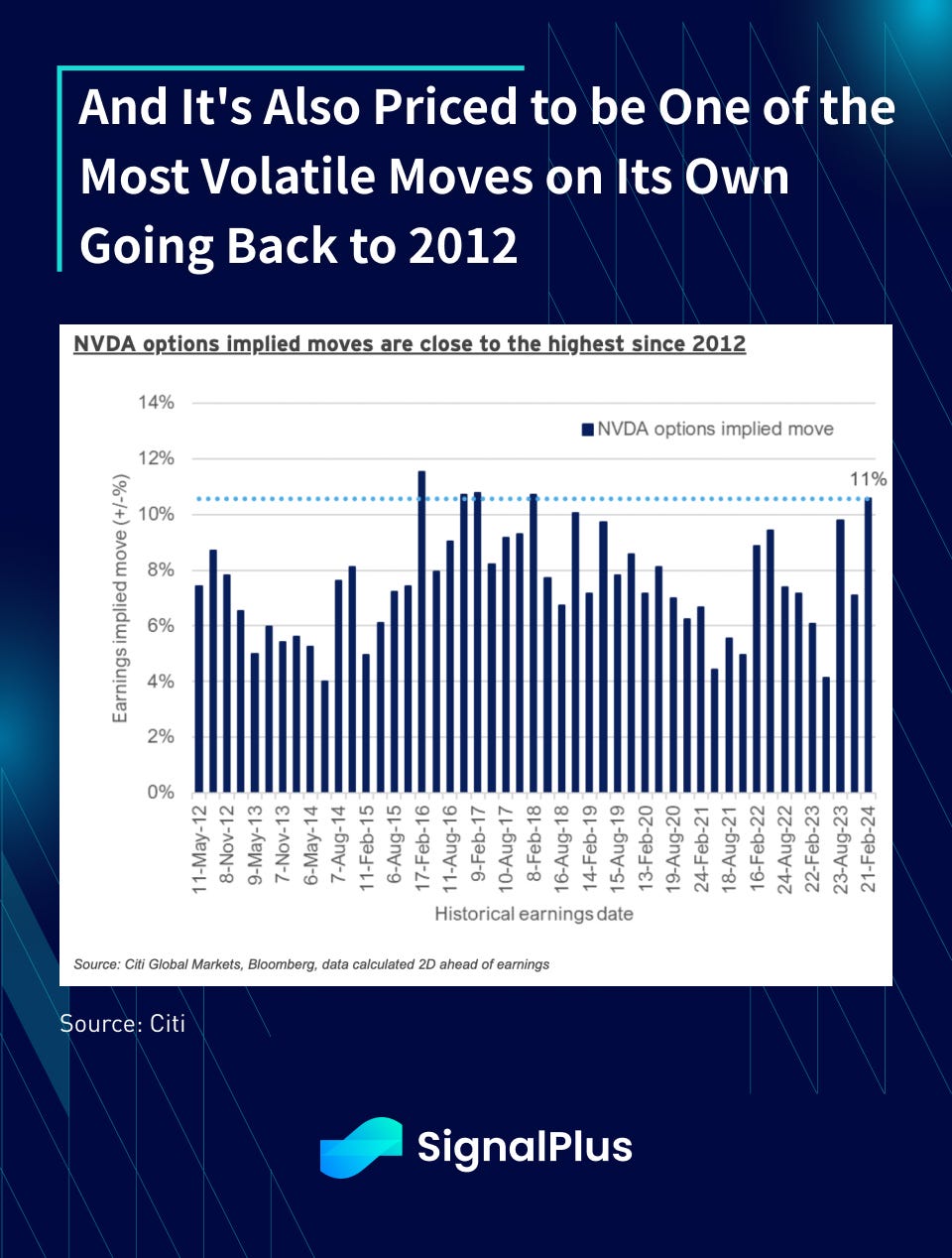

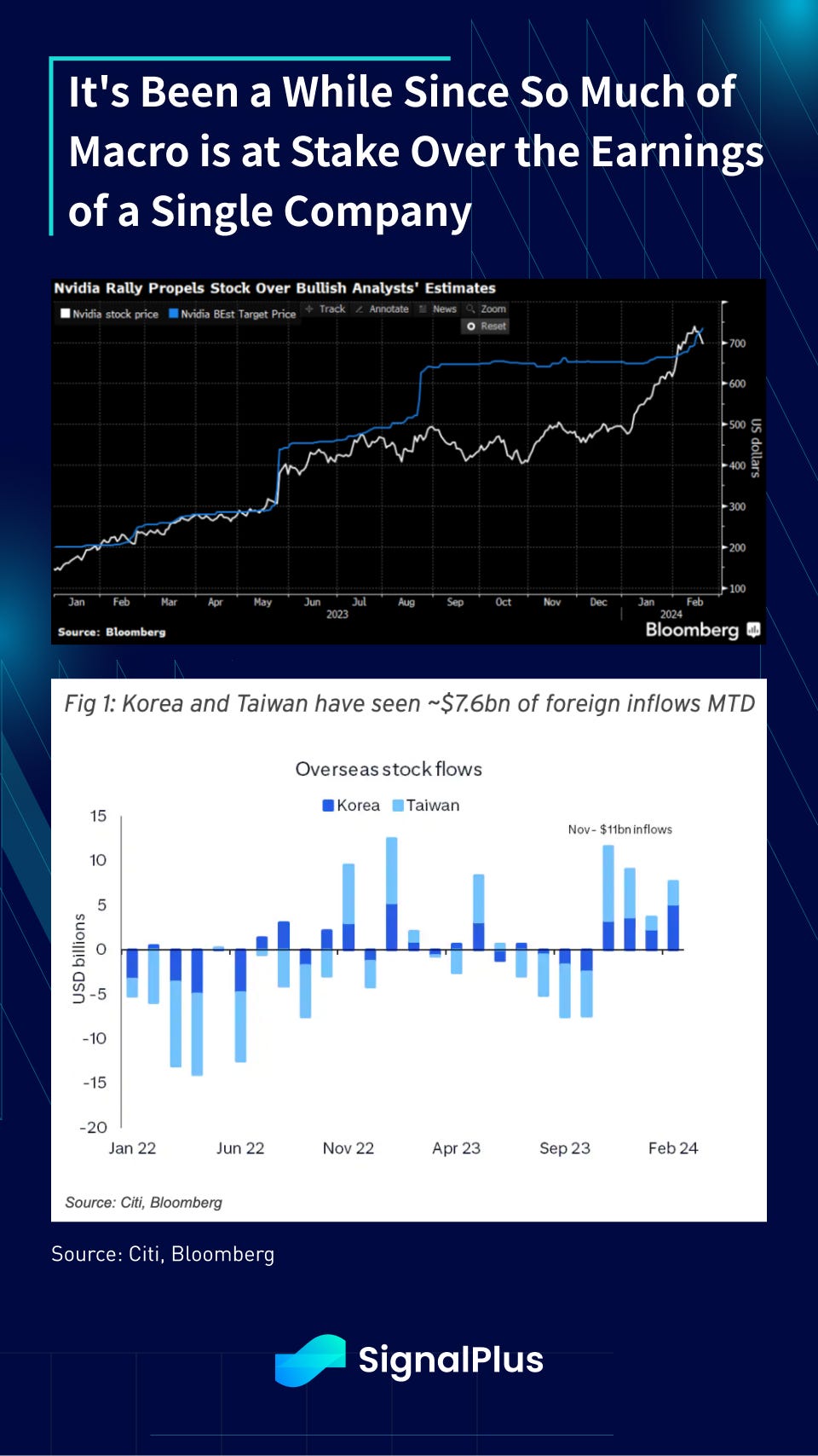

Nevertheless, equity markets did see a retracement yesterday as SPX saw an across the board sell-off, led by tech, as we head into the all important Nvidia earnings report later today. Without trying to over-state its importance, this earnings is being priced as the 2nd-most significant market moving event until the end of March, coming in just below the March FOMC and tied with the upcoming NFP release. Furthermore, on an individual basis, Nvidia’s option-implied move of 10.6% is around the highest range of its historical earnings releases going back to 2012, which is equivalent to a daily market cap impact of +/- $180 billion, for those of us who are counting. The AI FOMO theme is also evident through nearly $8 billion of foreign inflows into Korea and Taiwan equities YTD, so it’s probably fair to say that a lot is riding on this single earnings release.

Over in crypto, sentiment continues to surge with ETH breaking above $3K, and the 9 new ETFs saw the biggest volume day ($2billion) since day 1 of trading. Bloomberg’s ETF analyst ranks this their collective activity to be around the Top-10 traded ETFs in US markets, an incredible feat given how early we are still with mainstream re-involvement. CME’s futures open interest has also rebounded back close to record highs after suffering at ETF-led drop earlier in January.

However, as something we’ve also alluded to before, this shift in focus to (TradFi) ETFs is also shifting the balance of power a bit back to the West, with US trading venues now accounting for an increasing amount of Bitcoin’s market depth based on data from Kaiko. Furthermore, similar to what we see with traditional index activity, trading volumes have also spiked into “4pm EST fixings” as ETF issuers mark their books, and we would expect this behaviour to continue as more US-based ETF products get listed. This ‘changing of the guard’ is a trend that we have been highlighting, and warrants continued attention as digital assets become further institutionalized in the foreseeable future.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments