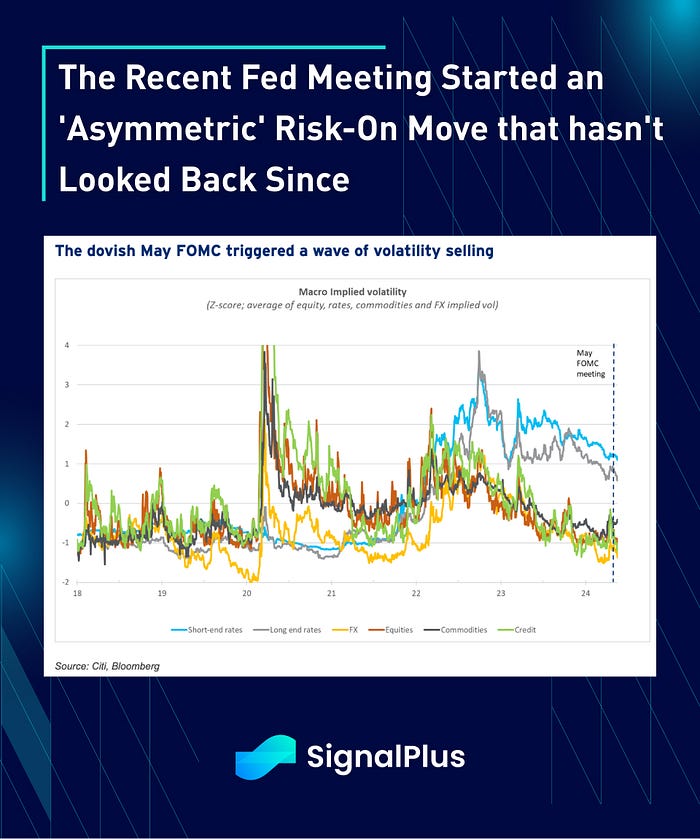

We ended the past week with a slowing growth and lower inflation hopes giving rise to yet another soft landing narrative. This is not the first time we’ve seen this movie, and the natural thing to do would be to FOMO into stocks, buy credit, receive rates, sell vol, and earn carry income. That has pretty much been the exact script since the last FOMC, with no signs of letting up without any significant variables on the horizon.

Equities made new ATHs this week, with the SPX rising 1.5% on the week and breaking above 5300. Automakers (+4.4%), tech (+2.9%), and real estate (+2.5%) on the week on friendly financial conditions. 10y yields fell -8bp on the week, and -27bp on the month, while oil (+2%), gold (+2%), and copper (+8%) all staged impressive rallies on the month. As the following WSJ article would attest to — what’s there not to love in the investment world?

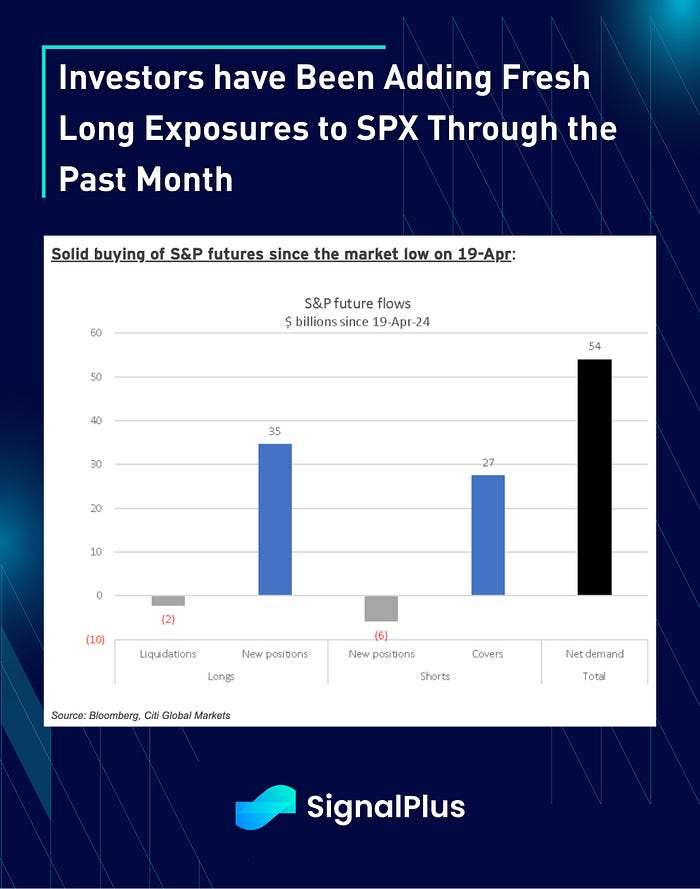

Furthermore, Wall Street dealers believe that the current recent equity recovery has morphed from pure short-covering to fresh long exposures, with Citi estimating that over $50bln of SPX futures have been added over the past month. ICI reports that over $20bln in US domestic equity ETFs have been issued MTD as retail have been profitably chasing this rally higher.

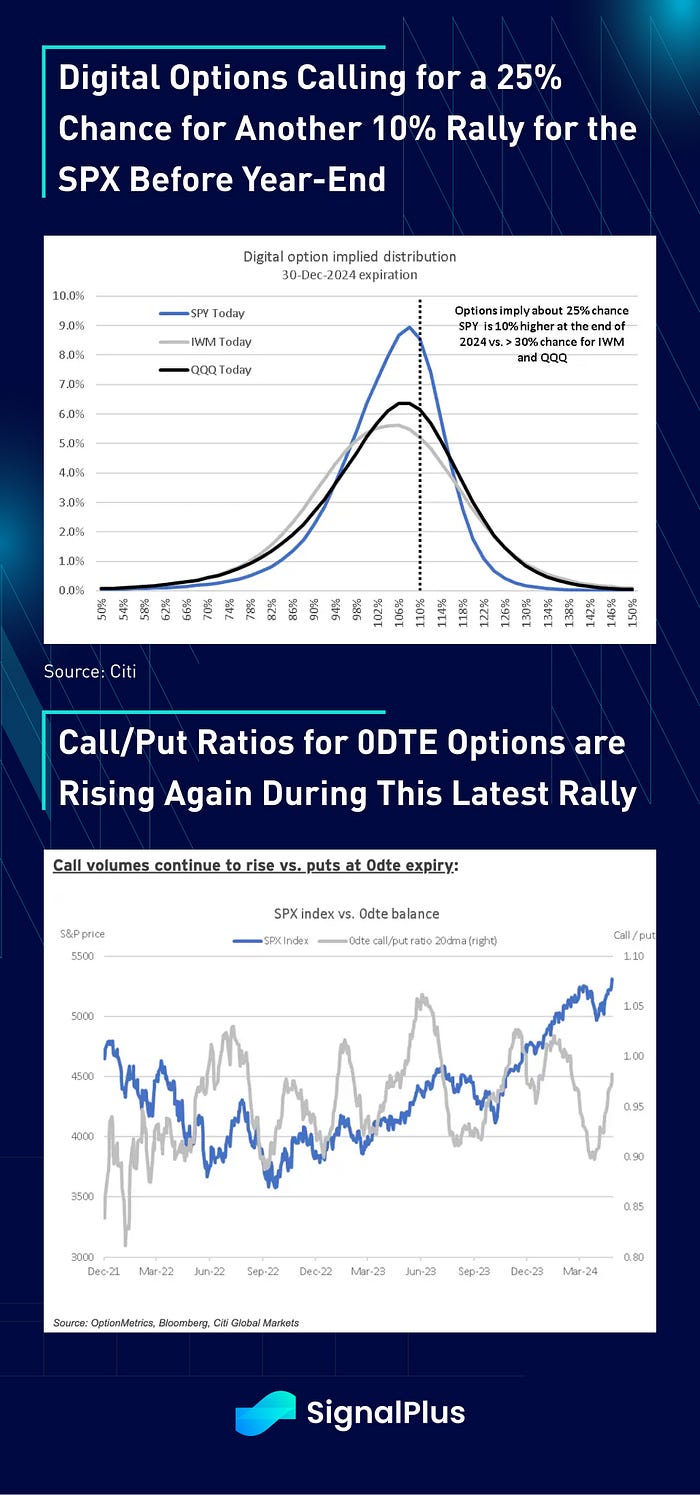

Equity option flows are pointing in a similar direction, with digital options (binary outcomes) pricing in 25% of a further 10% rally in the SPX to the year-end. Furthermore, call/put ratios on 0DTE options have been rising again throughout this rally with ~56% of volumes attributable to calls.

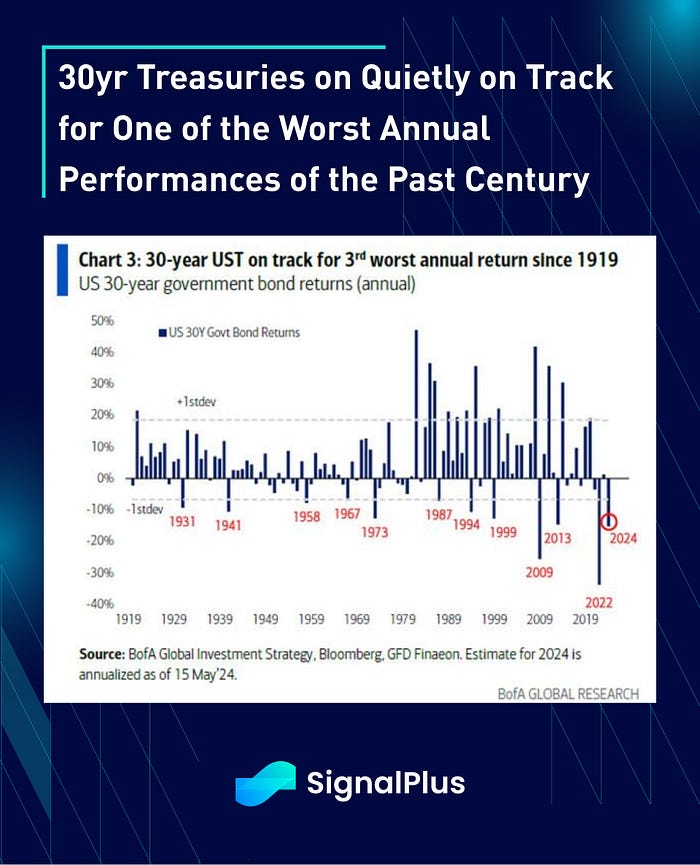

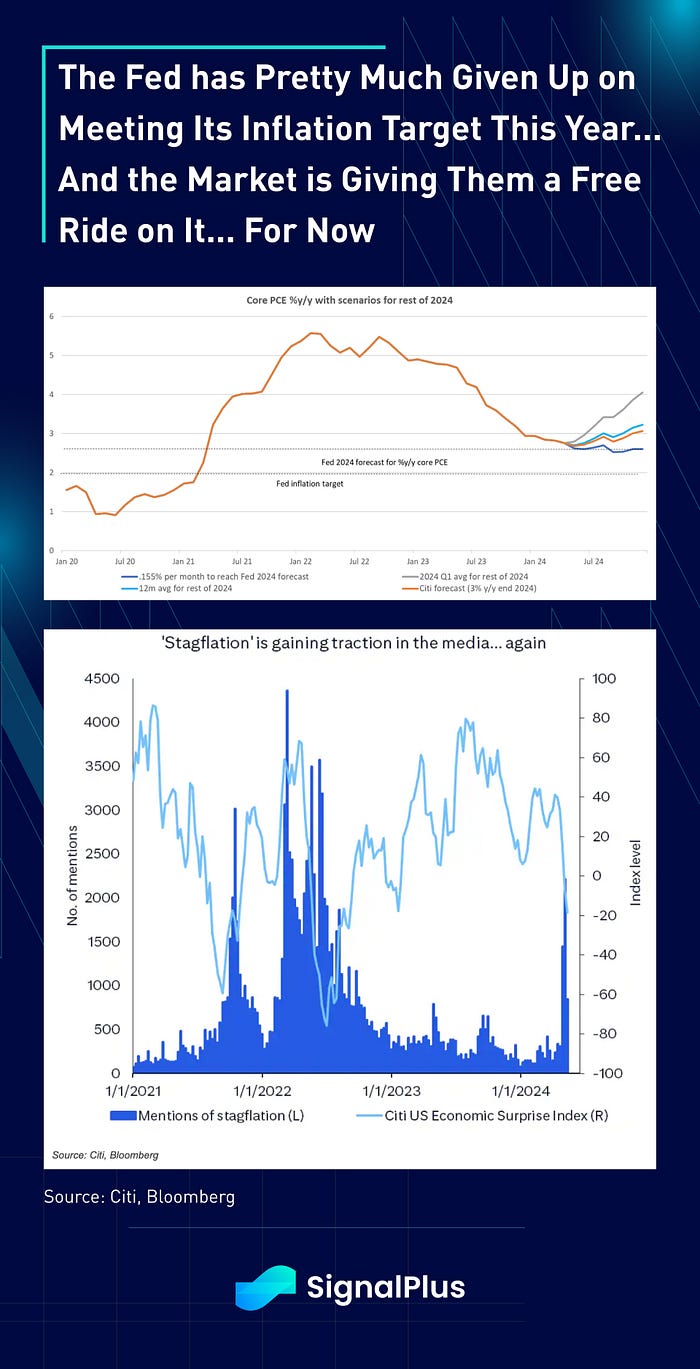

Underneath all the euphoria, it’s interesting to see that the 30yr long bond is the odd-one out, and is on track for the 3rd worst annual return over the past century based on BoA calculations. Lax government spending, out of control budget, overly-easy financial conditions, and an inflation-tolerant Fed (what inflation target?) are punishing long-rate instruments, as the fiscal largesse will have to be paid at some point via higher real rates and/or a weaker FX. But just not today…

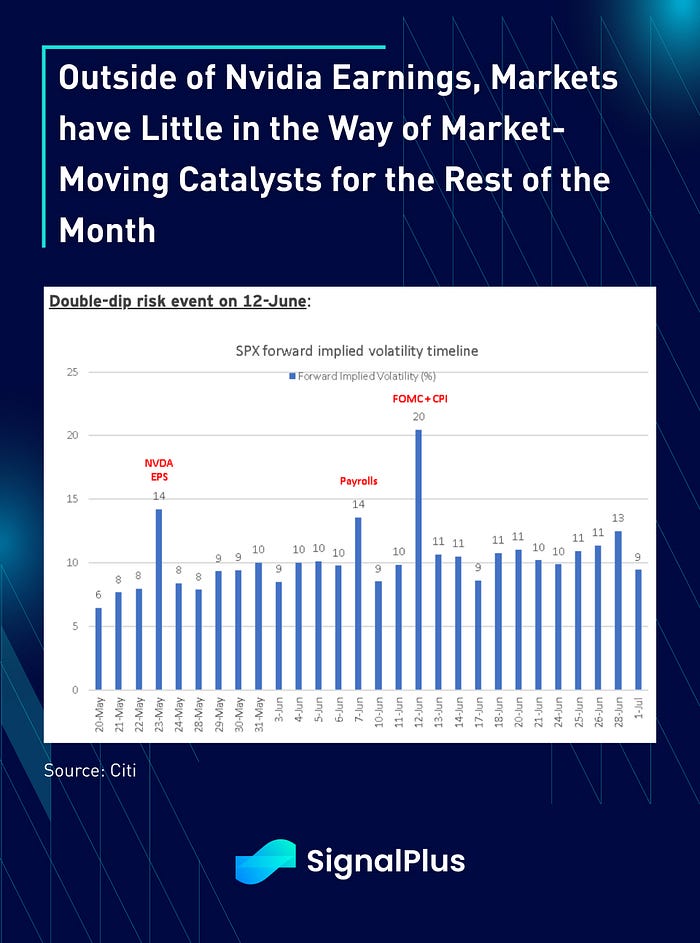

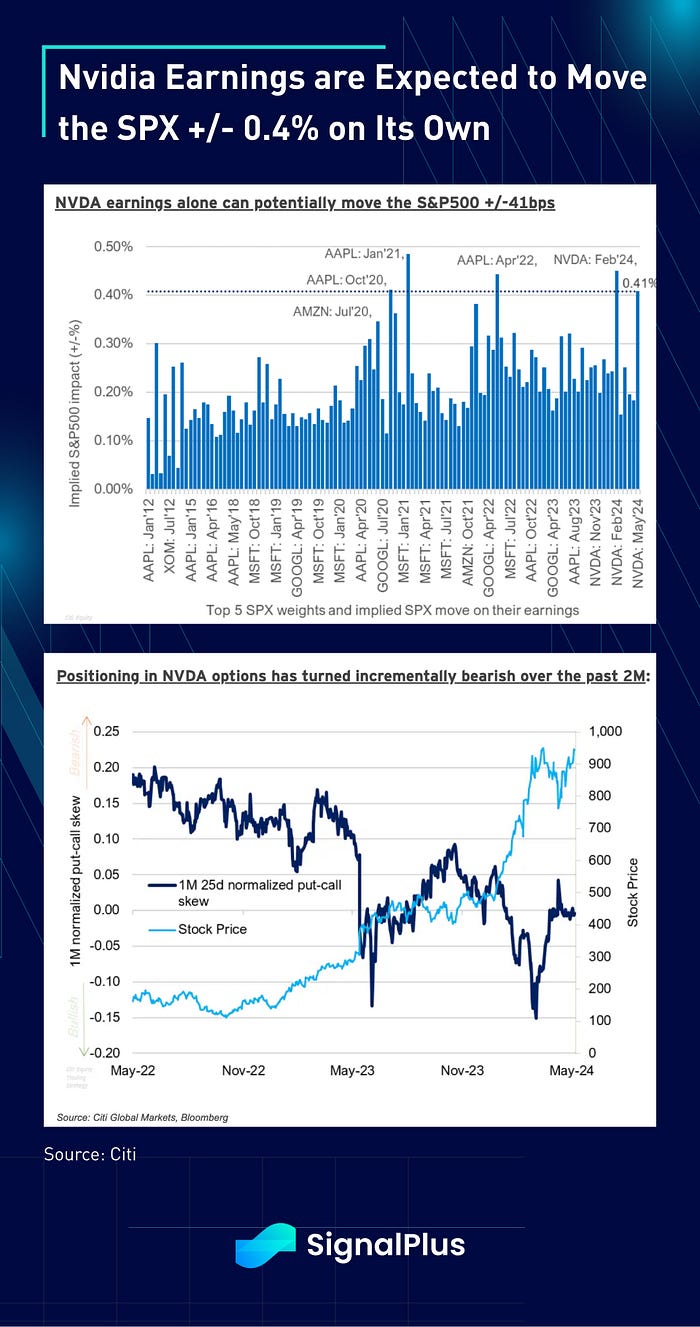

Looking ahead, economic data will be on ‘holiday mode’ with no catalysts of note until Nvidia earnings on Thursday, and then nothing again until NFP and FOMC+CPI in the first 2 weeks of June. Nvidia options imply a +/- 0.4% move on SPX based on earnings day based on the chip-giant’s heavy weight on the index, with positioning in the stock appearing less heavily concentrated than earlier in the year.

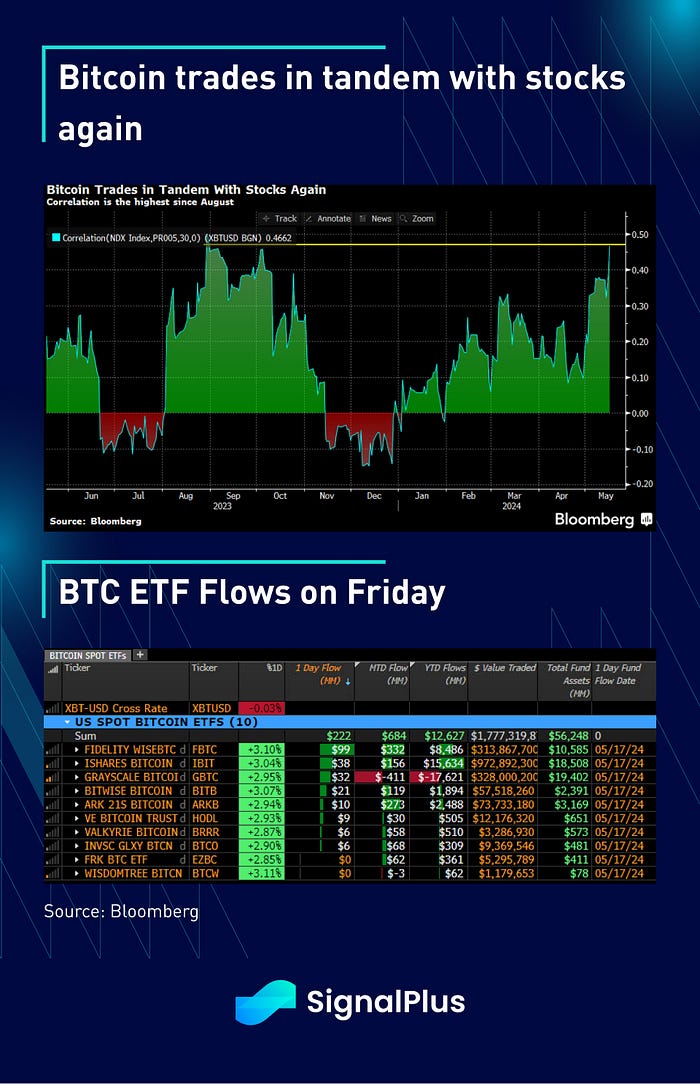

Not much to mention in crypto, with BTC prices trading with the highest short-term correlation to the Nasdaq since 3Q24. Price action looks constructive at 66k, with natives looking for a test of the ATHs again over the next weeks. Nothing changes sentiment like price, and certainly nothing changes crypto prices like equities at this juncture. While ‘everyone’ was a rates trader in 1H23, is every macro asset class now a Nasdaq day-trading tool in disguise? Hope the quiet markets will give everyone some well-needed rest in the near-term!

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments