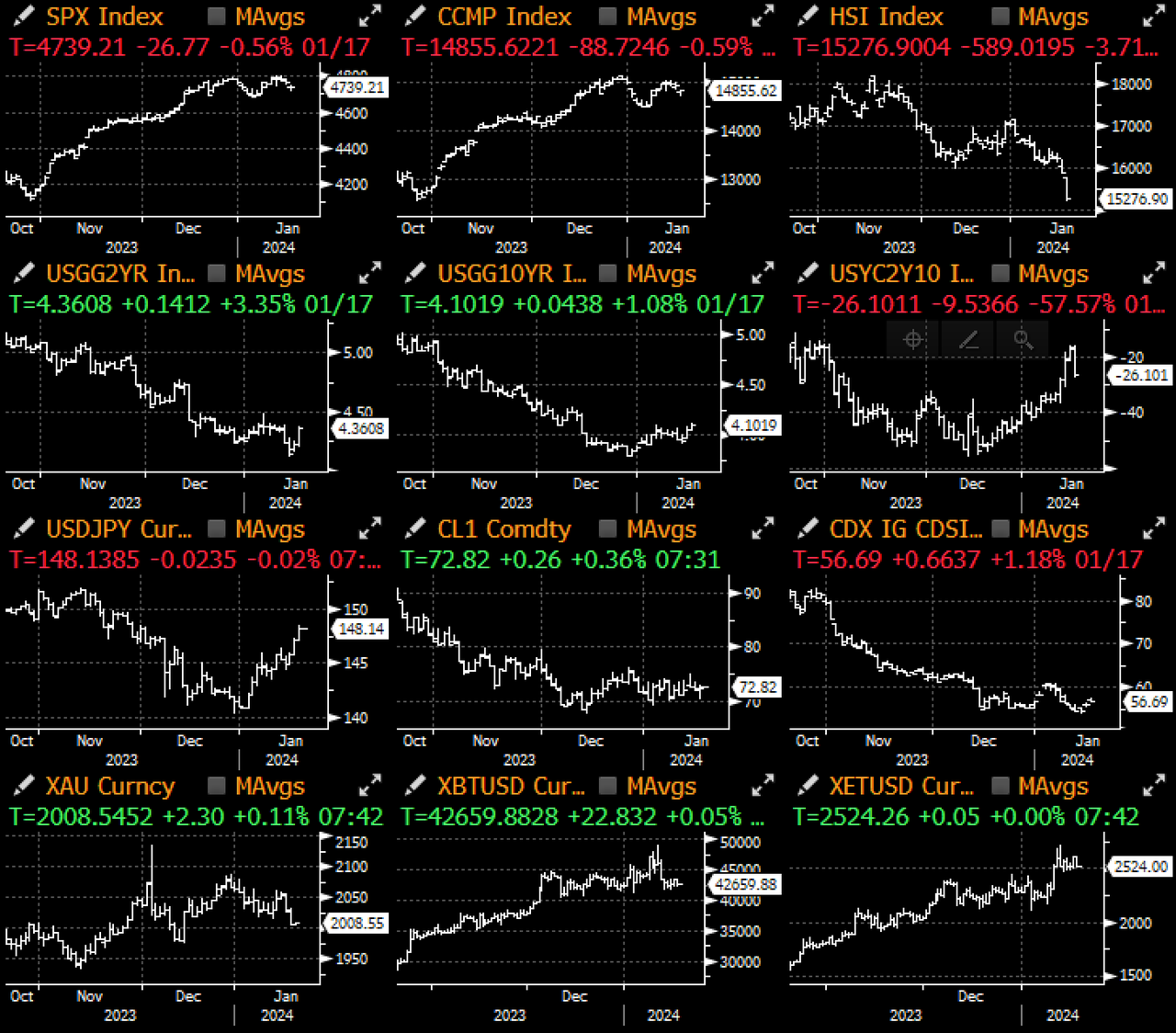

Yesterday marked the first session in 2024 where we saw some meaningful unwinds of the substantial eases priced into the asset markets. Europe and UK led the initial pushback, starting with UK inflation that unexpectedly increased for the first time in 10 months, leading to a 23bp jump in 5yr gilt yields and a -1.8% sell off in the FTSE 100. The move higher in gilts was the sharpest move since the Sep-2022 LDI crisis. The headline print of 4% was double the BoE’s inflation target, and market’s implied cutting odds in May swiftly dropped from 80% down to 55% in a straight line.

The ECB followed suit with ECB president Christine Lagarde signalling that Euronzone interest rates would come down in the summer, rather than in the spring as widely implied by interest rate swaps pricing. Largarde delivered her comments at the World Economic Forum that the ECB would only have the information it required for easing by “late spring”, in order to effectuate any rate easing decisions.

Next up, we had Fed Governor Waller stating that while the US is “within striking distance” of the Fed’s 2% inflation target, they should not rush to cut its benchmark rates until it’s clear that the lower inflation will be sustained. Specifically, he stated:

“The key thing is the economy is doing well. It is giving us the flexibility to move carefully and methodically. We can see how the data comes in, see if progress is being sustained,” Waller said in comments in a moderated online discussion organized by the Brookings Institution.

“The worst thing we’d have is it all reverses after we’ve already started to cut. We really want to see evidence that this progress…in the real data and the inflation data continues. I believe it will.”

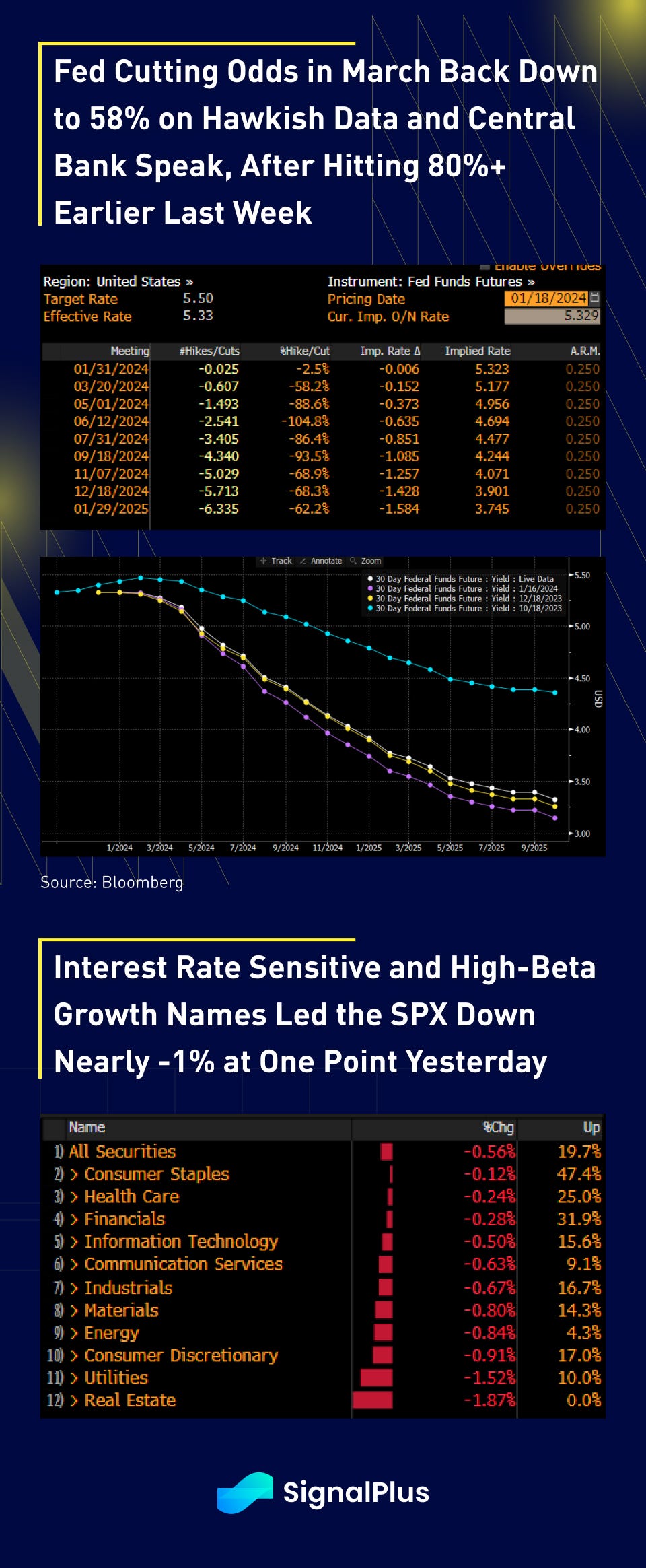

Waller’s comments are some of the strongest worded comments we’ve seen from the Fed against a March easing from Fed officials in recent weeks.

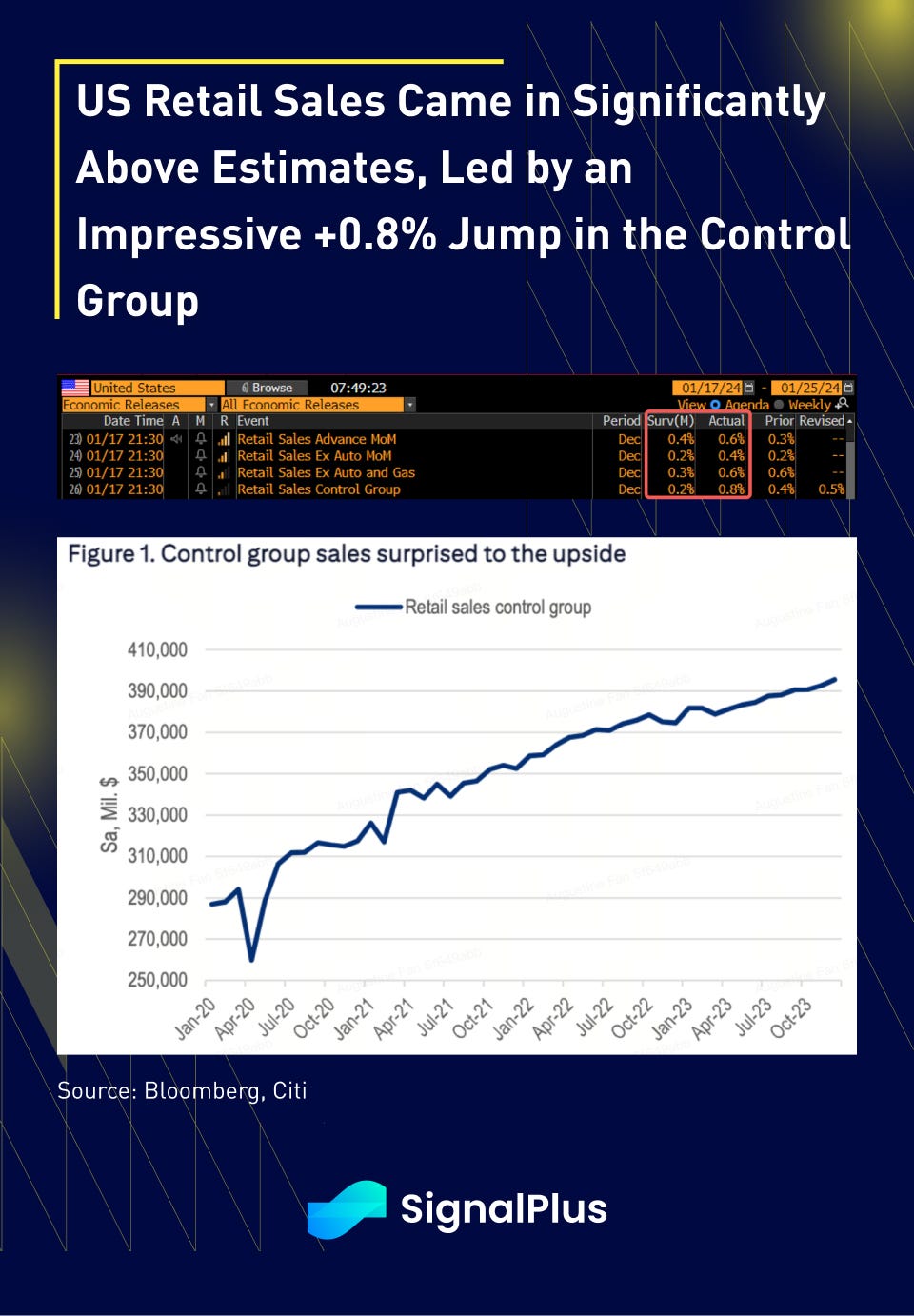

On the data side, retail sales surprised to the strong side, printing 0.6% MoM in December and 0.4% ex-Autos, equivalent to a 5.2% YoY pace. A strong recovery in department store sales (+3% from -2.5%) and general merchandise (+1.3% from -0.2%) contributed to the beat, while the control group (ex building materials, motor parts, and petro sales) was also strong at +0.8%, far outpacing estimates of 0.2%.

The combination of the above pushed treasury 2yr yields +13bp on the day, while the $13bln 20yr reopening also proved to be a mild disappointment, with a 0.9bp tail and a low 2.53x bid to cover ratio. SPX sold off -1% at the lows, led lower by interest rate sensitive sectors (RE -2%, Utillties -1.5%), as well as high-beta growth proxies such “unprofitable tech” with a -2.4% daily drawdown. March cutting odds have come back to around 58% versus hitting >80% last week.

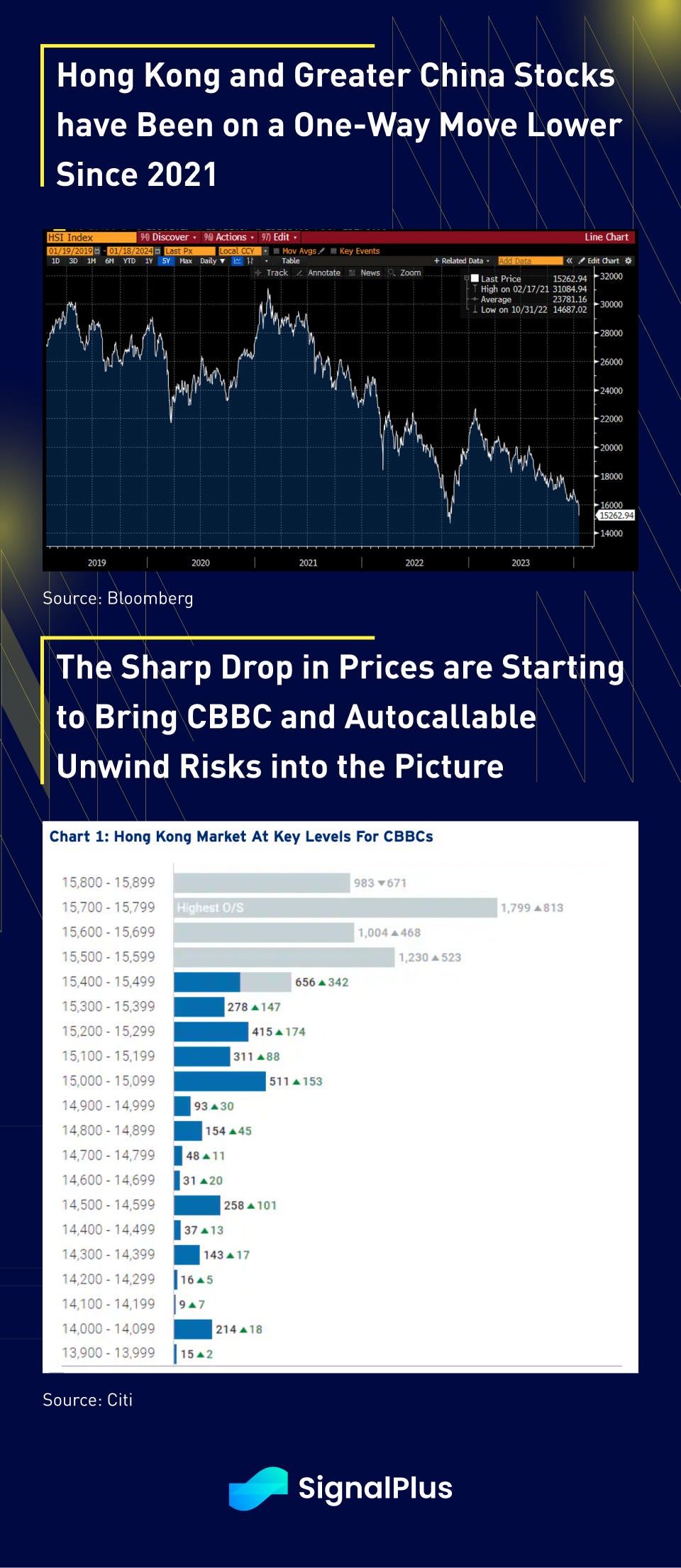

The risk-off move was not limited to just the US, with China/HK stocks seeing a similar blood-bath at the Asia open, with the HSI trading down nearly 4% on China growth and policy disappointments. A complete lack of medium term catalysts have depressed sentiment greatly, with technicals looking increasingly poor and dealers warning about autocallables and CBBC unwinds leading to further downside reflexivity on the HSI. Furthermore, with more local reports of heavy real estate losses and loan impairments for Hong Kong banks, and we are inching closer to forcing a ‘liquidity put’ from local policy makers to put a temporary stop to the situation.

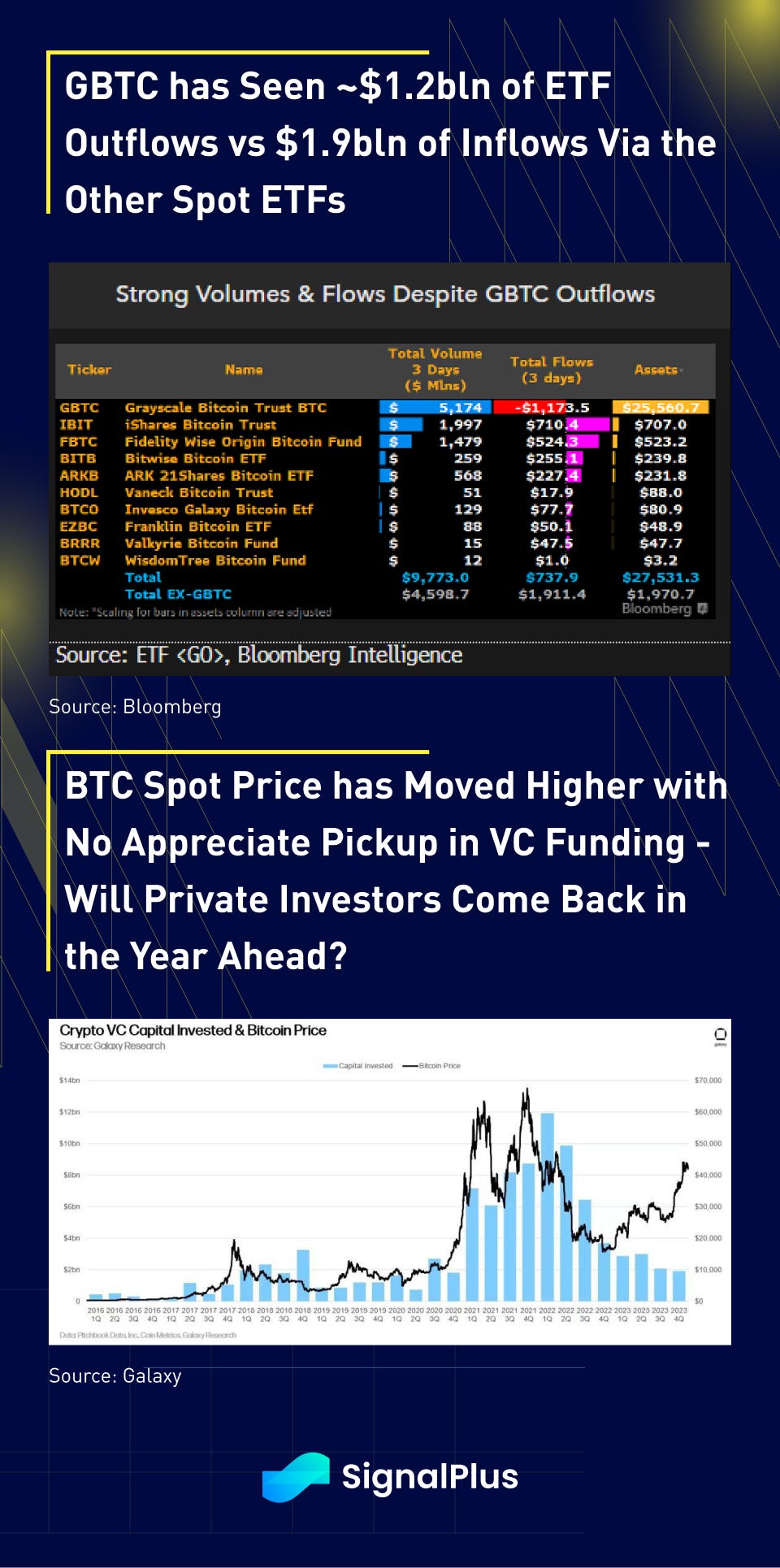

In crypto, according to Bloomberg estimates, GBTC has seen ~$1.2bln in outflows over 3 days, versus 1.9bln of inflows in the other 9 spot ETFs for a net inflow estimate of $800mm. Total trading volume for the new spot Bitcoin ETFs in the US crossed $9.7 billion in the first three days, with GBTC accounting for over 52%. Spot prices have been steady at around $42.5k over the past week, with inflows likely to take time, and near-term price action likely dependent on the overall risk sentiment and repricing of the Fed’s pivot.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments