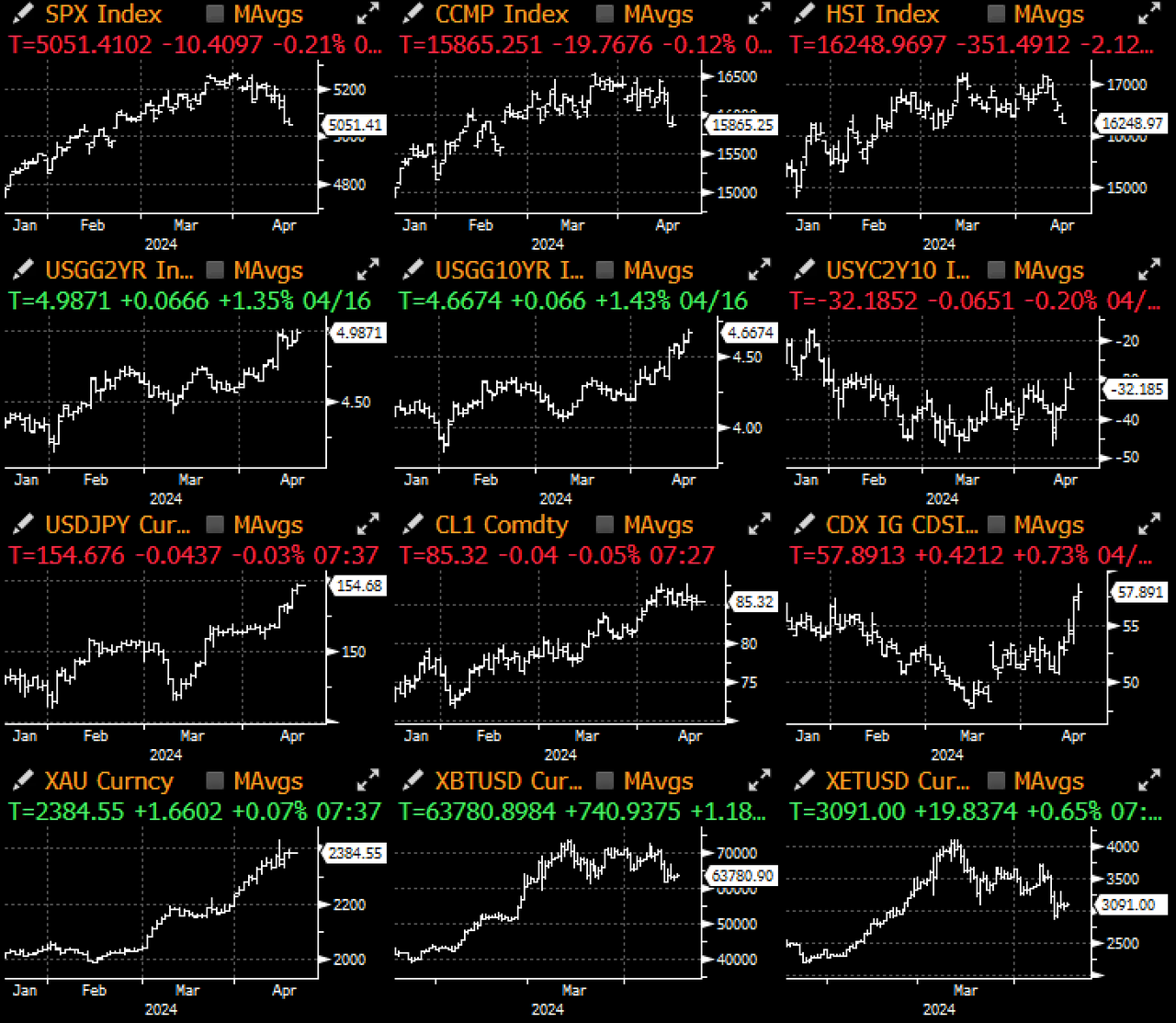

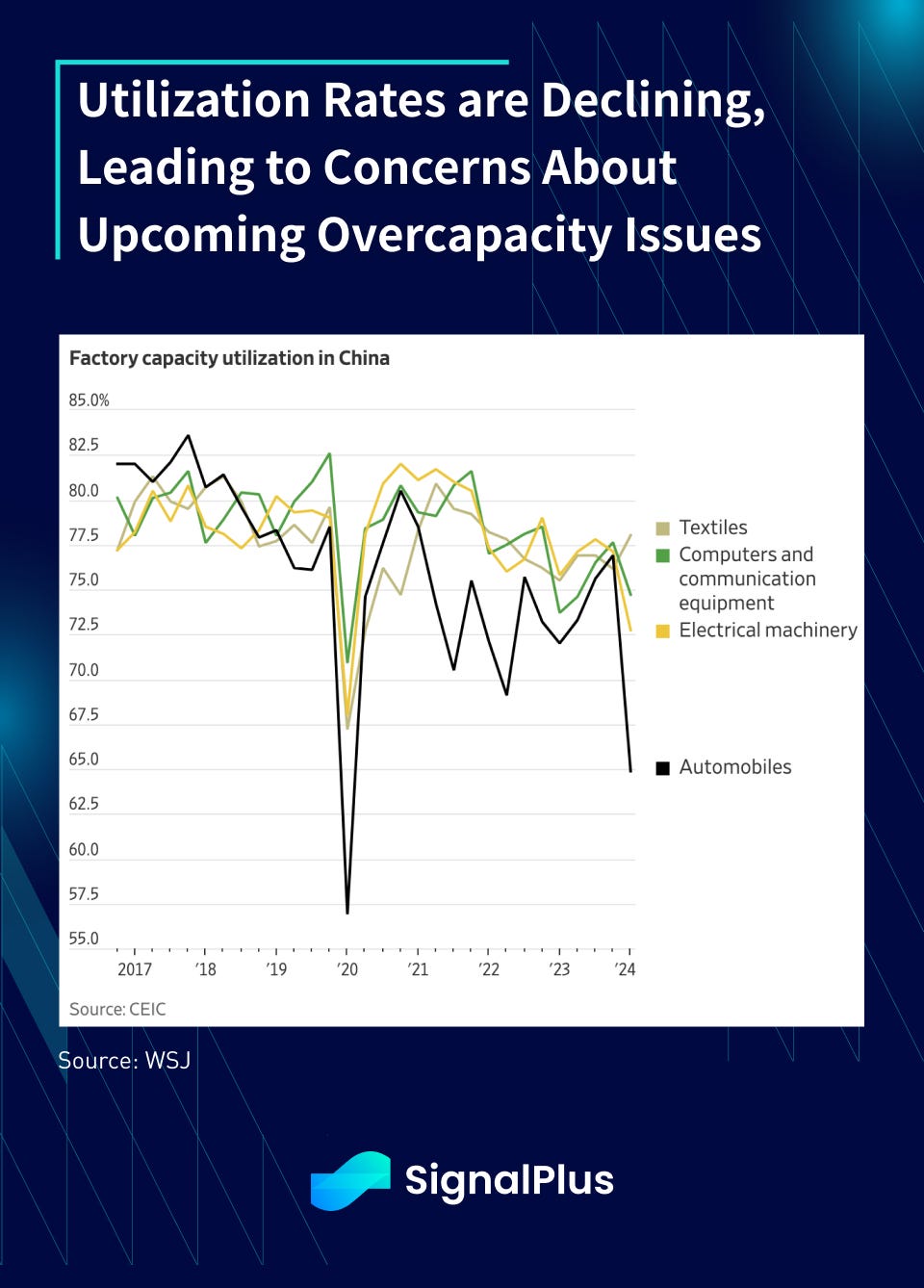

Markets managed to take a short breather yesterday, although PNL tension remains high with choppy intraday price action and thin order book liquidity. China data started on the day with a positive note, reporting a 5.3% Q2 GDP that was well above consensus estimates of 4.8%. However, optimism soon faded as investors remained skeptical of the underlying strength, especially in light of a much weaker set of industrial production and retail sales figures that were less advertised. Industrial production came in at just 4.5% in March, significantly below expectations of 6.0% and last year’s pace of 7%, while manufacturing capacity utilization plummeted to 73.8%, the weakest levels since 2015 outside of the covid period. Falling utilization rates were prevalent even in state-sponsored sections such as automobiles, chips, solar panels, and other electrical equipment, adding to concerns about a looming overcapacity problem.

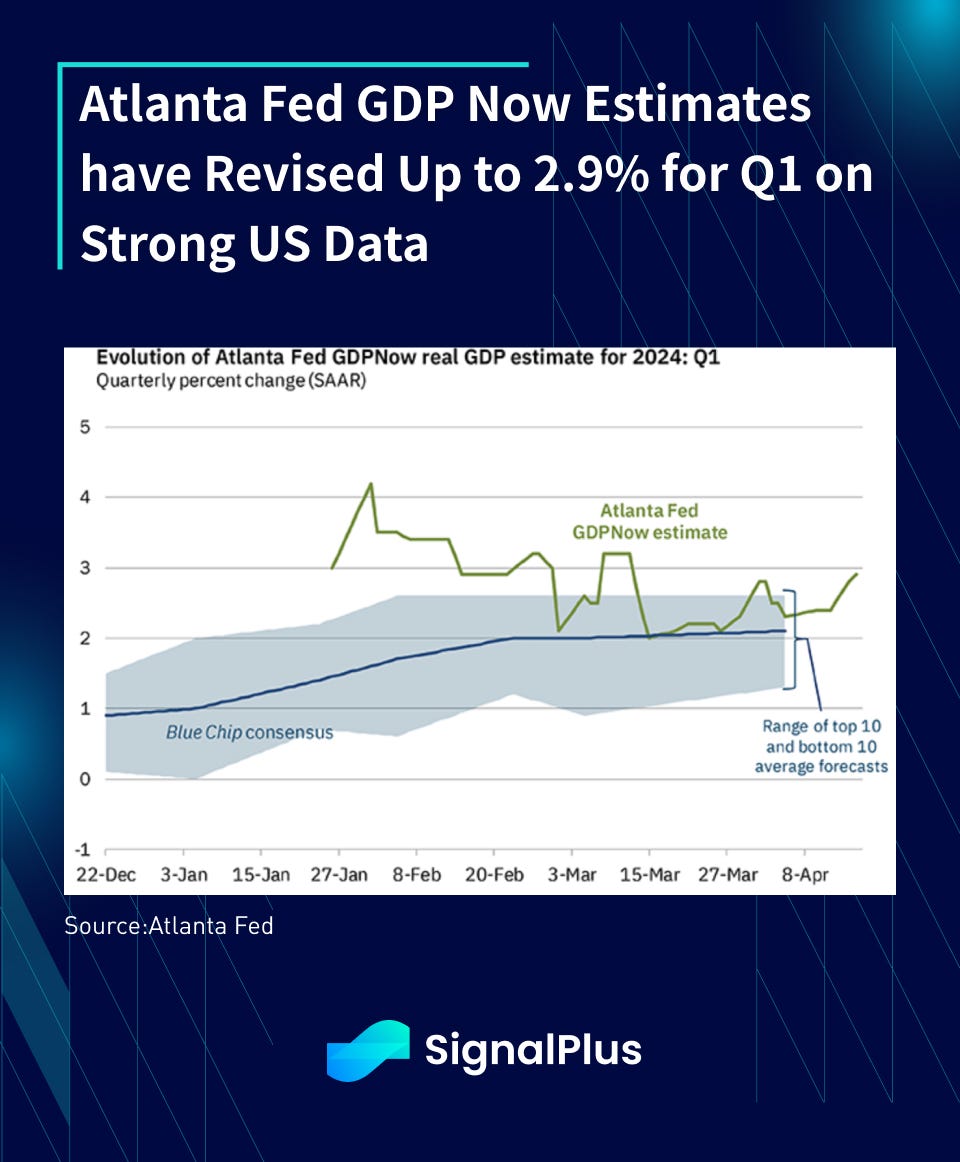

Over in the US, the recent run of strong data has led the Atlanta Fed to raise their GDPNow estimates to 2.9%, still substantially above Wall Street estimates. 10y year real yields (inflation adjusted) rose back to 2.2%, while the 2/10s real yield curve has also steepened back to the steepest levels since October 2022 on rising inflation concerns. By the way — does anyone still remember the ‘guarantees’ of an economic recession with the inverted yield curve from 2022–2023 from casual macro observers? So much for that right?

With the realities of sticky inflation and robust economic activity that’s impossible to ignore, the entire Fed committee, even including the Chairman himself, has been forced (grudingly) into dialing back their dovish narratives, separating the Fed in a lonely camp all on their own when it comes to upcoming policy trajectory:

- Fed Chair Powell: “The recent data have clearly not given us greater confidence and instead indicate that it is likely to take longer than expected to achieve that confidence,”

- Fed Vice Chair Jefferson: US interest rates might have to stay higher for longer if “inflation is more persistent than I currently expect it to be.”

- Boston Fed Collins: “it may just take more time than previously thought” and that “CPI figures in Q1 came higher than I’d hoped”

- Richmond Fed Barkin: want to see more“broader disinflation, not just in goods”

- NY Fed Williams: “rate cuts don’t appear imminent”, alluding that “there are definitely circumstances that we would need higher interest rates, but that’s not my base case.”

Constrating those statements against other developed market central bankers:

- ECB’s Lagarde: ECB will cut rates soon, barring any major surprises; “We are observing a disinflationary process that is moving according to our expectations,”

- BoE’s Lombardelli: interest rate cuts ‘are the direction of travel’

- BoC’s Macklem: “we don’t have to do what the Fed does, we do what Canada needs”

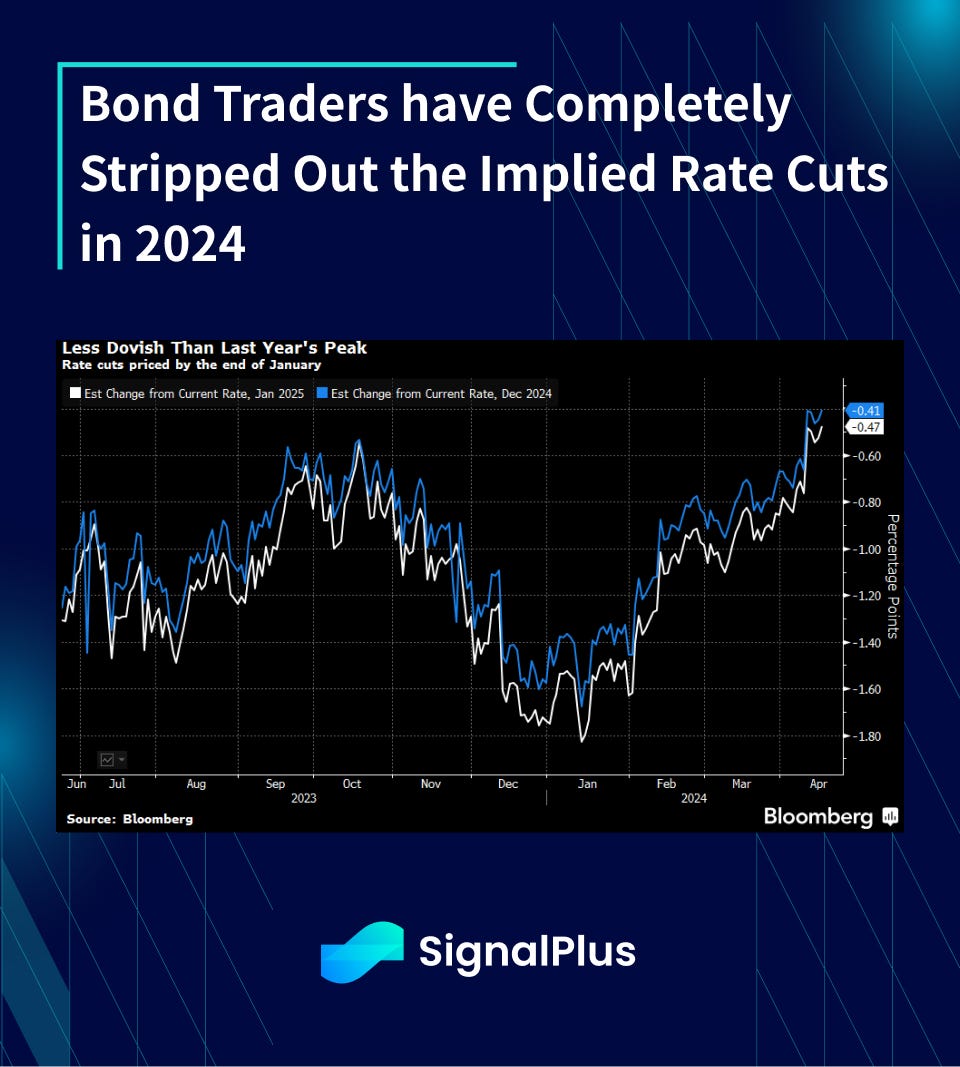

On the back of the Fed’s about-face, interest rate markets have stripped out the majority of implied rate cuts in 2024, unwinding all of the Q1 dovishness and breaking above even last October’s peak hawkishness. Furthermore, the policy divergence with other central bankers is giving a firm bid to the USD, with USDJPY trading above 155, USDCNY fix above 7.10, and the overall DXY index back at the strongest levels since 2022.

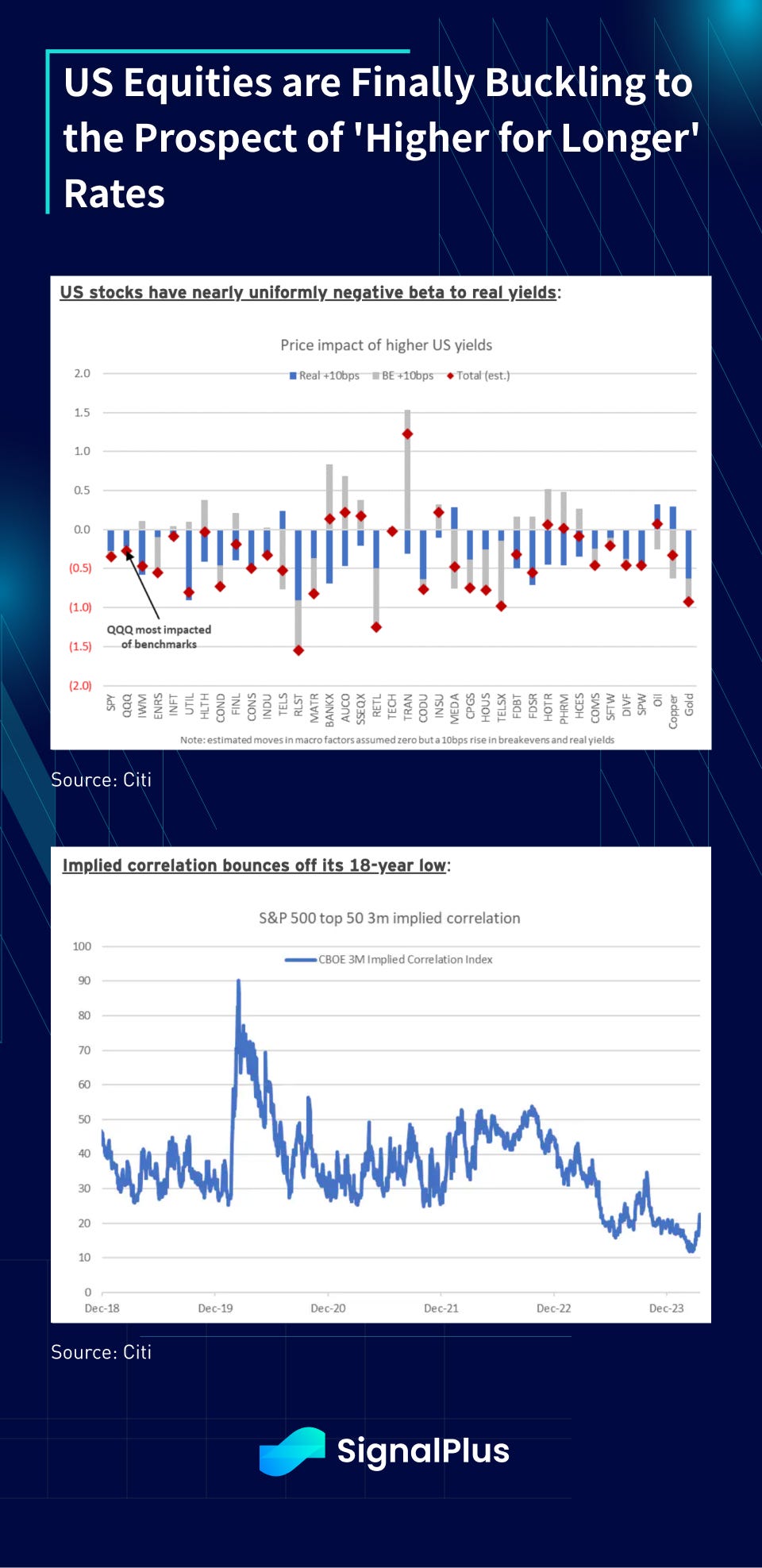

Furthermore, the spillover from higher real yields has been more problematic this time, with equity markets finally buckling under the prospect of rates being ‘higher for longer’, though more due to overbought positioning than changes in underlying fundamentals. US equity’s negative beta to yields have increased recently, leading to back to back -1% drawdown days in the SPX for the 1st time since last October. Furthermore, equity VIX closed above 19 for the first time since Halloween and implied stock correlation has jumped to 23 vs just 12 at the end of march. The ongoing tension around the Middle East will likely keep implied volatility pricing high over the foreseeable future.

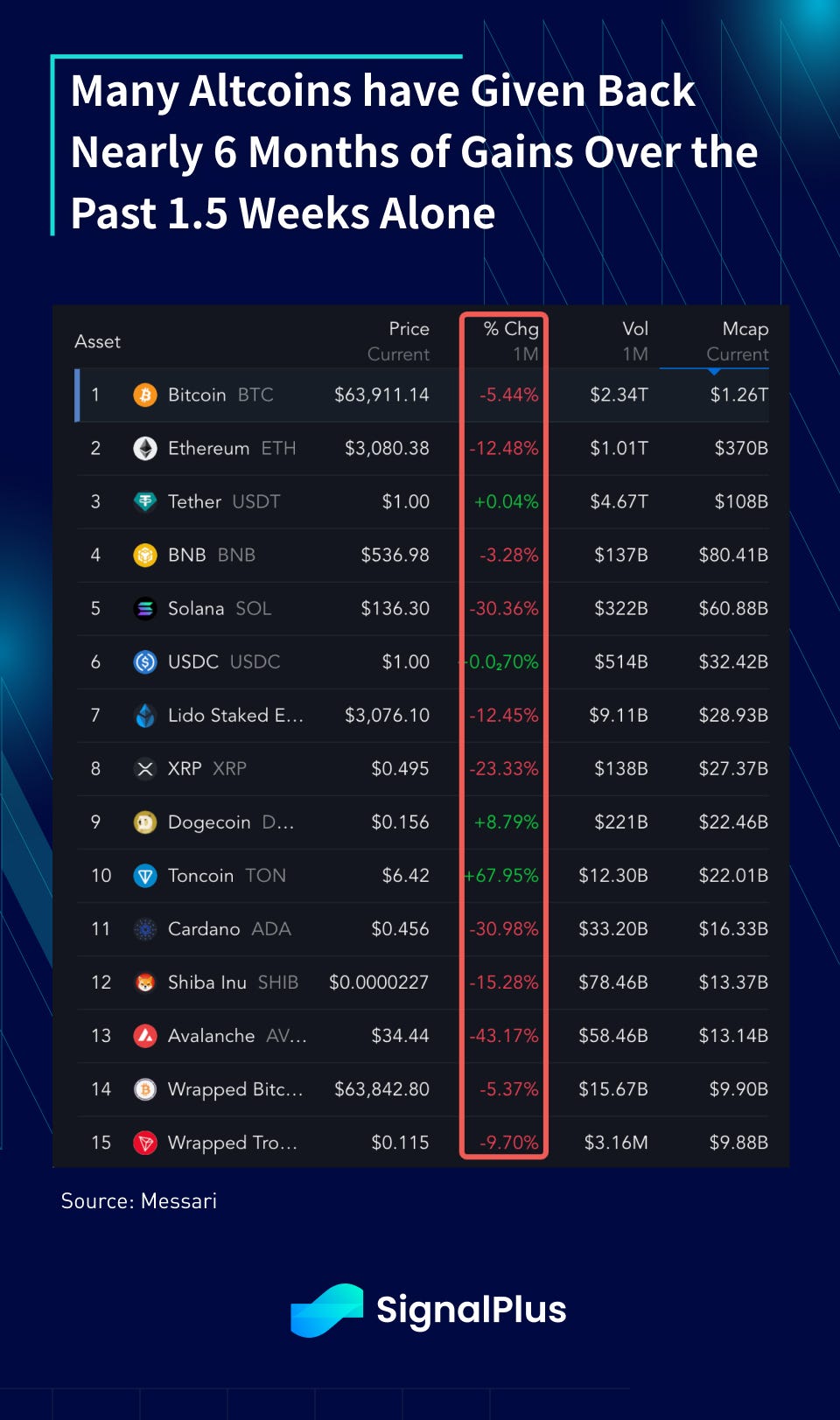

Over in crypto, BTC prices have tested and held a couple of stops beneath 60k, hovering back at 64k as of the time of writing. However, the rest of the crypto space are faring much worse than Bitcoin, with ETH/BTC ratio continuing to dip to nearly 4 year lows, with SEC looking increasingly unlikely to approve Ethereum ETFs this round, while altcoins have lost -30% to -40% of value in the past month vs just -5% in BTC. There has been significant PNL damage inflicted over the past 1.5 weeks, which will take quite some time to work through.

ETF inflows have continued to slow as well, with Blackrock’s IBIT the only ETF to show net inflows since Friday, with retail not showing much interest to ‘buy the dip’. We expect ETF inflows to play a smaller role in the near future as the current FOMO narrative has largely run its course. In the meantime, we would expect Bitcoin prices to trade like a ‘turbo-Nasdaq’ note once again, reverting to its patterned behaviour over the past 4 years.

In other words, less digital gold, more leveraged beta. Let’s pray that our ‘tech-bros’ friends can hold the fort with strong earnings into and out of the current reporting season! Good luck!

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments