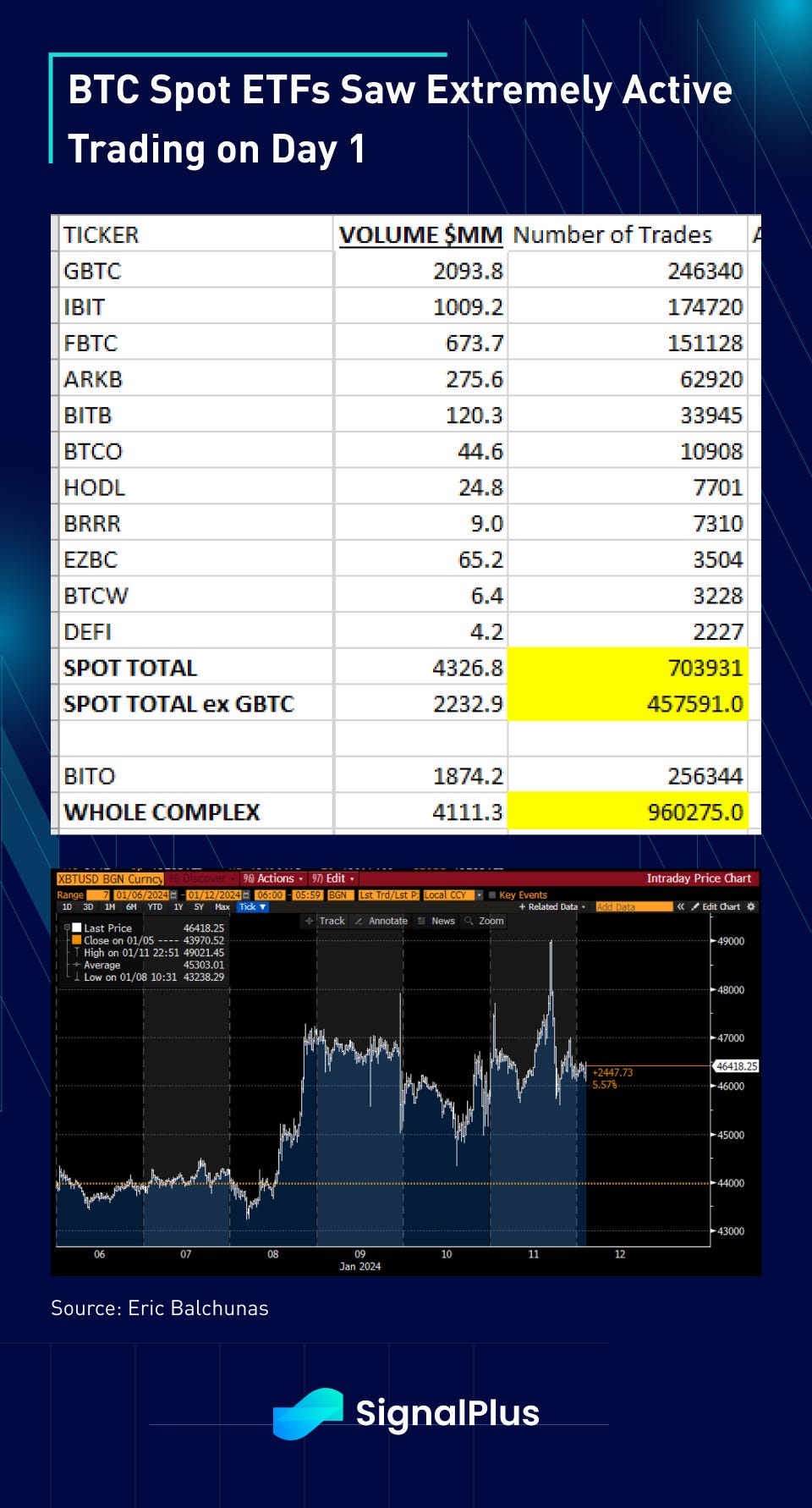

US spot Bitcoin ETFs left its record in history today, ratcheting $4.6bln in trading volumes in Day 1, led by Grayscale’s GBTC at $2.1bln, followed by Blackrock’s IBIT at $1bln. Bloomberg ETF analyst Eric Balchunas called it “easily the biggest Day One splash in ETF history”, with over 700,000 individual transactions out of the 11 spot ETFs, double the number of trades for the Nasdaq QQQ, signifying a lot of smaller individual participation.

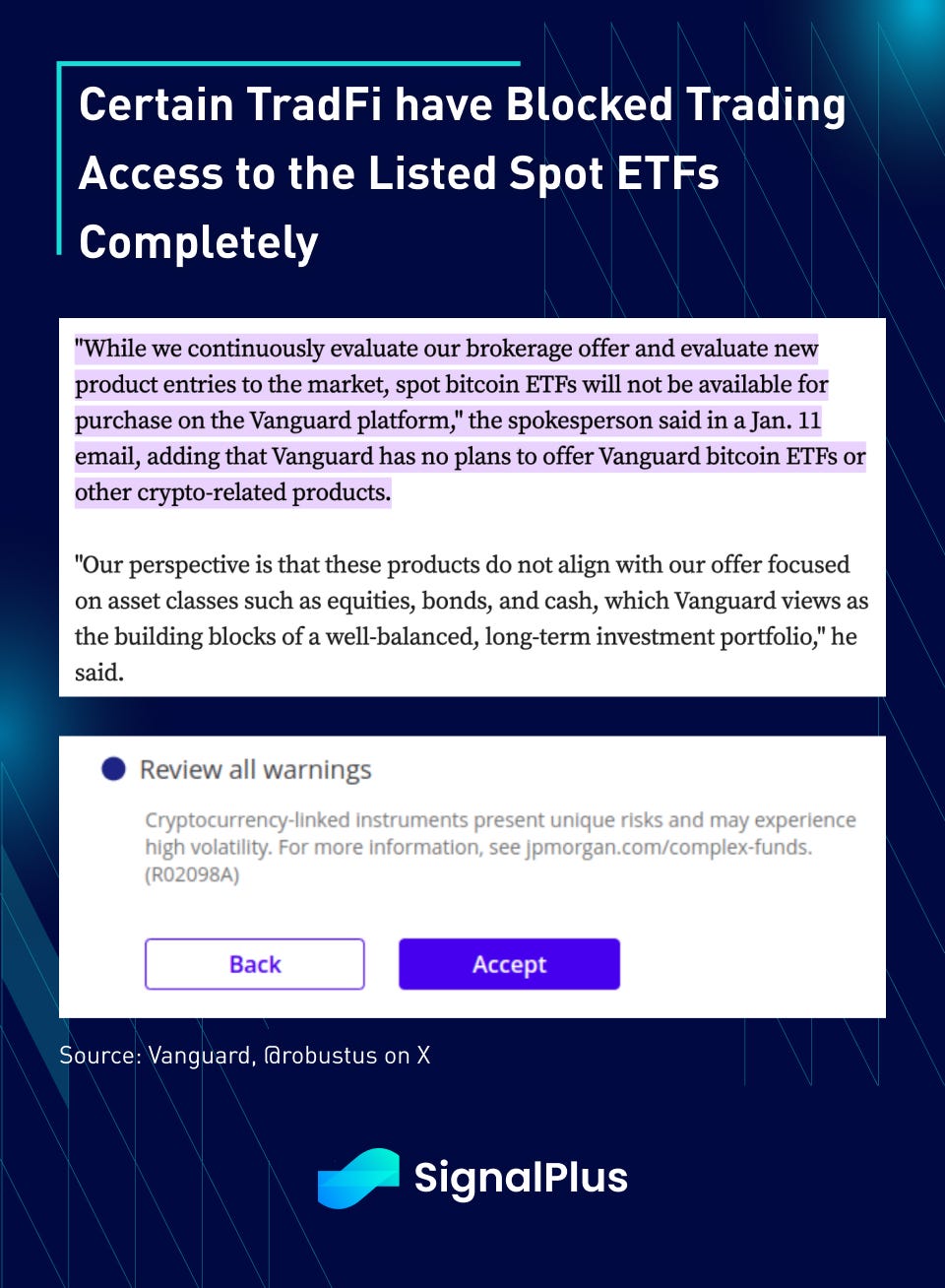

However, it wouldn’t be crypto news without some usual caveats; there have been reports from multiple sources that some trading brokerages and banks have been… somewhat less than willing to promote or allow the trading of these US listed ETFs, with Vanguard the most explicit in blocking their clients from trading these products completely off their platforms, citing ‘mis-alignment’ with their core offerings.

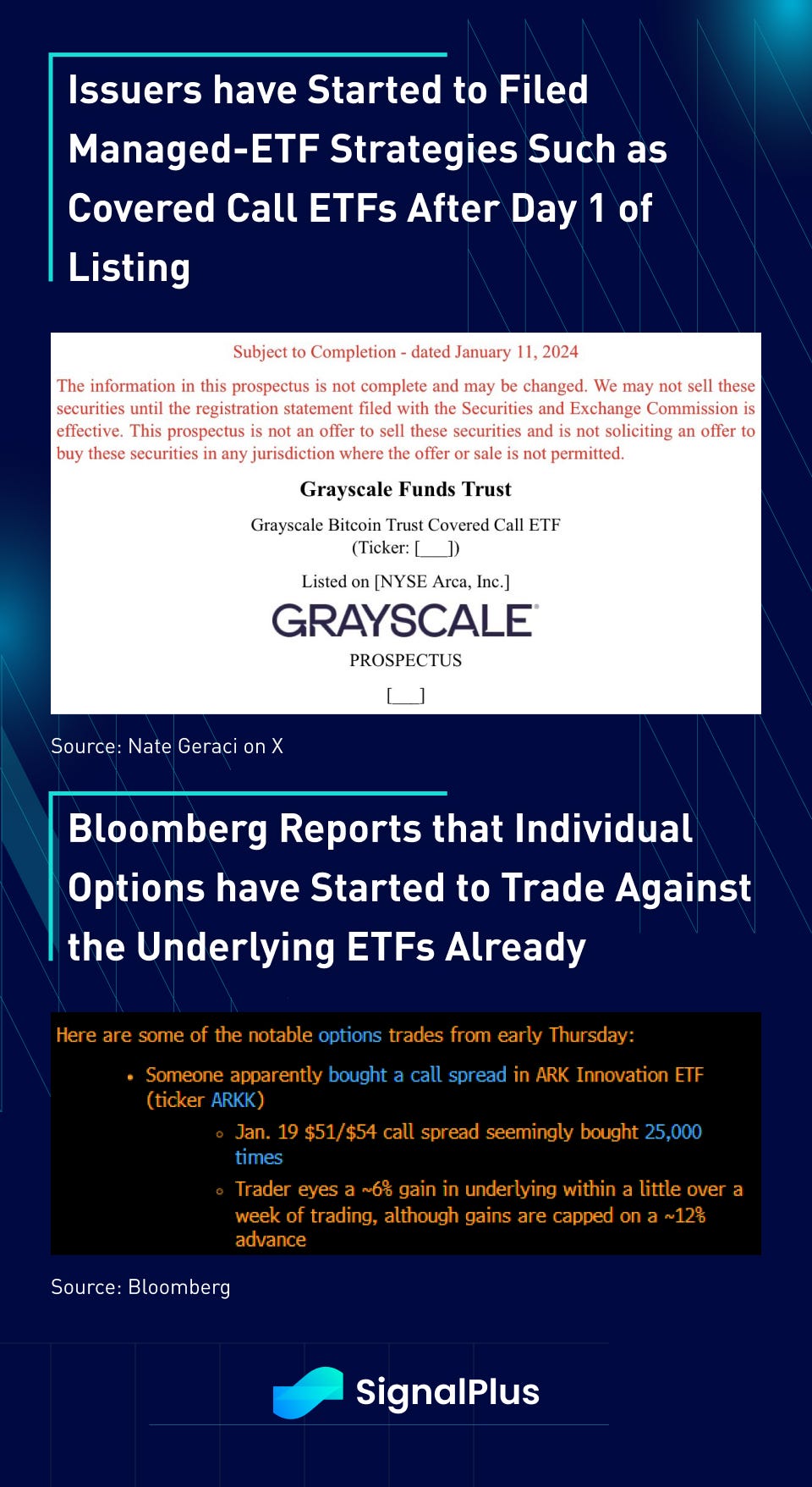

Nevertheless, the floodgates have been opened, and the availability of a ‘USD settled’ Bitcoin proxy has effectively created a ‘non-deliverable’ market for TradFi investors who might not want dabble in the blockchain, and wish to stay within their comfortable fiat rails. We believe this development opens up a massive investor base and institutions now who can trade BTC (and soon ETH) as ‘just another asset class’, without having to engage in a tiresome and often ideological argument over what crypto stands for. Surely enough, within just 24 hours, there have been reports of issuers filing Covered Calls as a separate ETF, and this should proliferate quickly into all sorts of ‘managed-ETF’ strategies involving options and leverage that have been done thousands of times over in the TradFi space. 2024 is going to be a tremendously exciting year for crypto participants, especially in the area of derivatives.

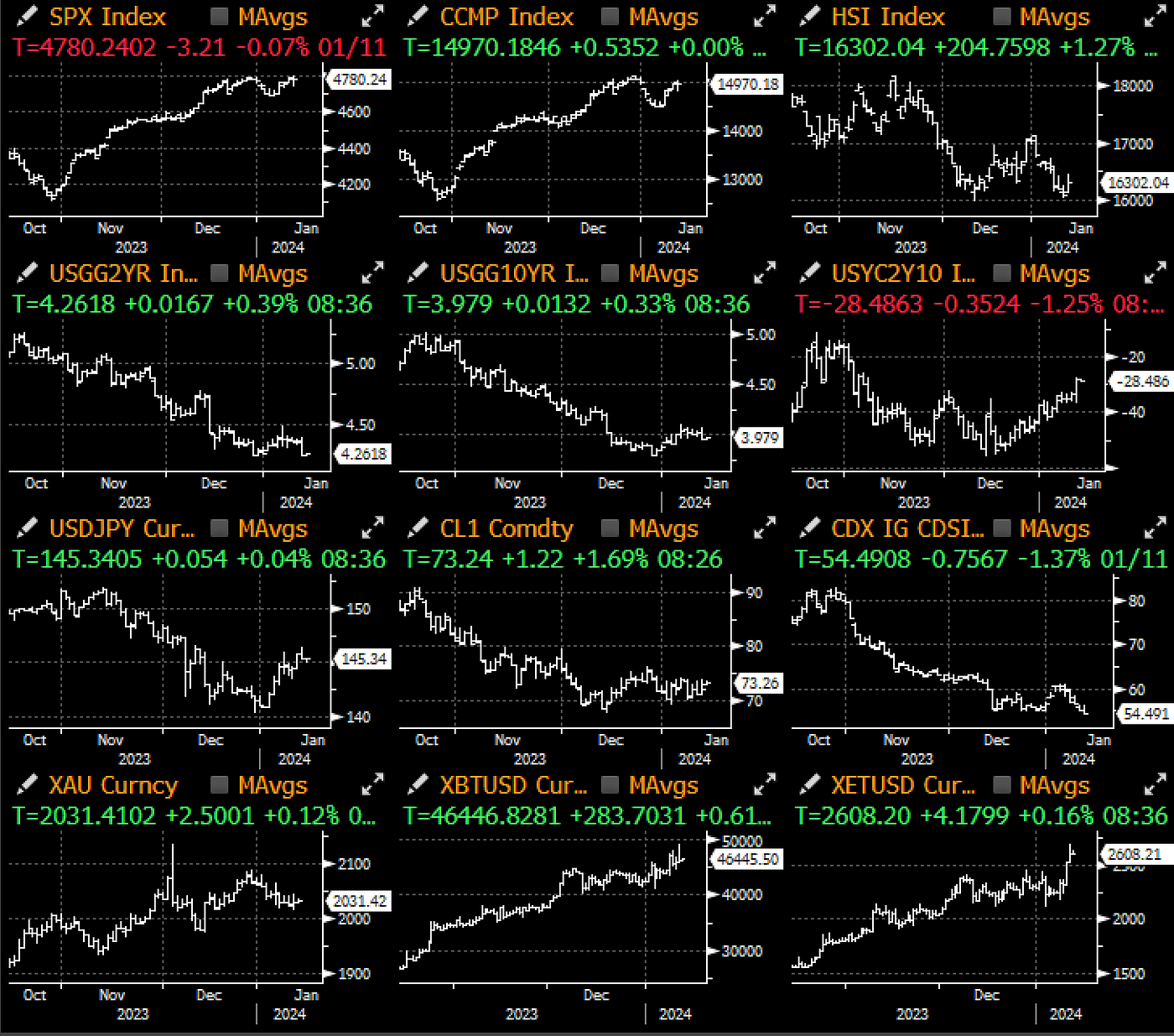

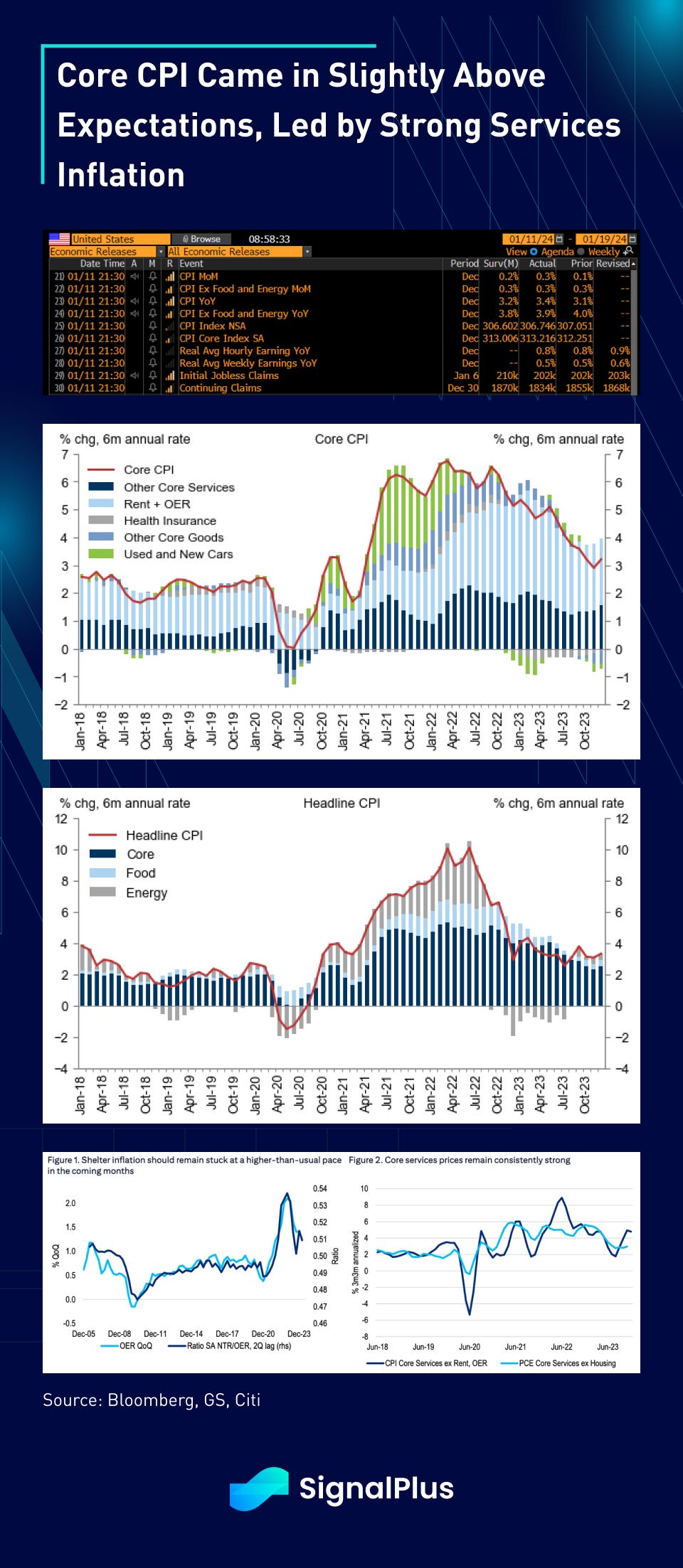

Back in TradFi land, core CPI came in slightly above consensus on a non-rounded basis (0.31% vs 0.26%), led by persistent strength in used car prices, apparel, core services, and OER. Headline prices came in at 0.3% due to a 0.2% increase in food prices and a 0.4% increase in energy. On a longer term basis, core CPI has troughed in the 3–4% annualized camp over the better part of the last 6 months, still significantly above the Fed’s long-term target, while underpinned by strong service inflation across both shelter and non-shelter categories.

While the data is unlikely to change the market’s outlook on the Fed, this could put a damper on how dovish Fed officials can sound without deviating too far from the party line. March cutting odds remained stable at ~65–70%, with CY2024 cuts still pricing in a full 150bp of easing by year end.

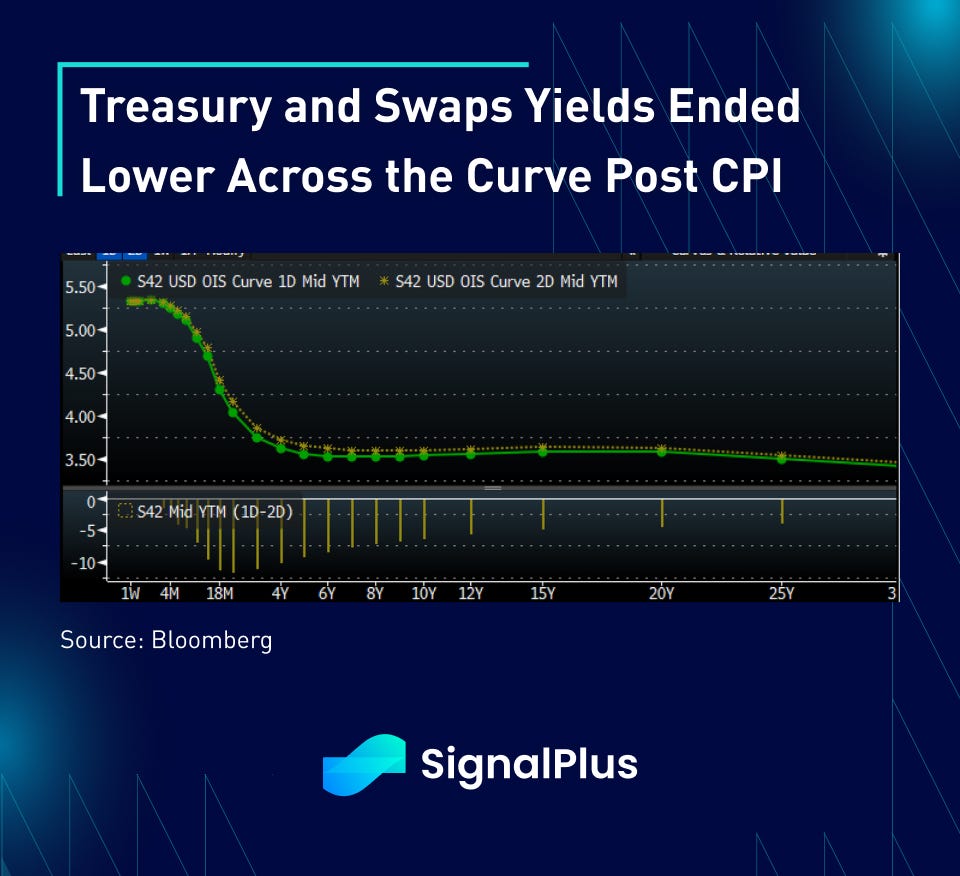

Fed’s Mester, a noted hawk, stated that “I think March is probably too early in my estimate for a rate decline because I think we need to see some more evidence”, which the market actually took as somewhat dovish given the lack of a more forceful pushback from her. She had previously noted that markets were ahead of itself in terms of pricing in Fed cuts post the December FOMC, so this was seen as another baby step towards acceptance of incoming rate cuts. Bond yields ended around 6bp across the curve in a bull-steepening manner, with 2yrs leading the way with a 9bp drop back towards 4.25%.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments