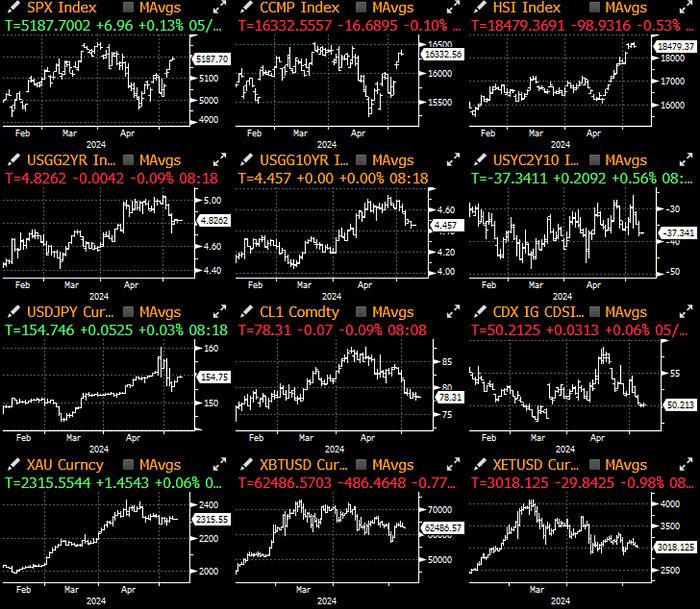

Another quiet session for macro assets with prices largely in a holding pattern across the board. A couple of Fed speakers went on tape with diverging views — NY Fed Williams (centrist dove) echoed Powell’s view that it would be “totality of the data — not just CPI or employment” that will drive the Fed’s view on rate policy. Furthermore, he reiterated that “eventually we’ll have rate cuts”, but monetary policy remains in a “very good place” for now, and that the labour market is coming into “better balance” post NFP. On the other hand, Minneapolis Fed Kashkari (hawk) stated that interest rates will likely need to be held at current levels for an “extended period”, and that “it’s much more likely we would just sit here for longer than we expect or the public expects right now until we see what effect our monetary policy is having”. Furthermore, he tried his best to keep rate hikes in the picture by stating that “I think the bar for [the Fed] raising is quite high but it’s not infinite. There is a limit when we say, ‘OK, we need to do more’”, with the bar being inflation staying entrenched at around 3%.

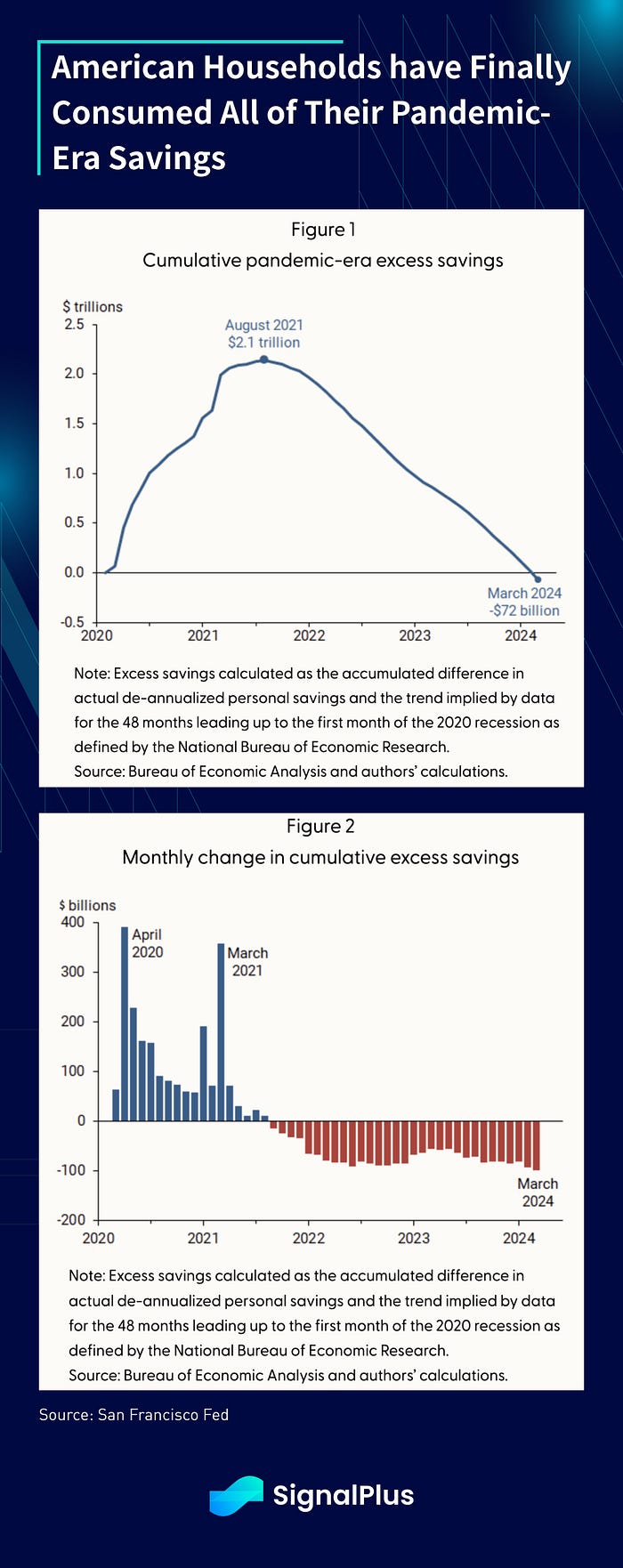

On the data side, these comments arrived on the heels of a weekend release from the SF Fed that the cumulative excess savings from the pandemic-era has been exhausted, going down from a peak of $21T in August 2021 to -$72B in March 2024. Straight from the SF piece: “the depletion of these excess savings is unlikely to result in American households sharply cutting their spending levels as long as they are able to support their consumption habits through continuous employment or wage gains…and higher debt”. While this might be true in the meantime, the combination of this against still high rates and a slowing labour market will surely put macro observers back on watch for more signs of an economic slowdown.

Not much to note elsewhere on asset prices, though corporate issuers are taking advantage of the current lull in activity to go on another issuance spree. A whopping 14 borrowers announced deals on Tuesday, totally more than $34bln of new issues being priced over the past 2 days alone, blowing past earlier estimates. Yield demand remains insatiable with orderbooks seeing >4.4x in oversubscription, despite corporate spreads coming in at the tightest levels since 2007.

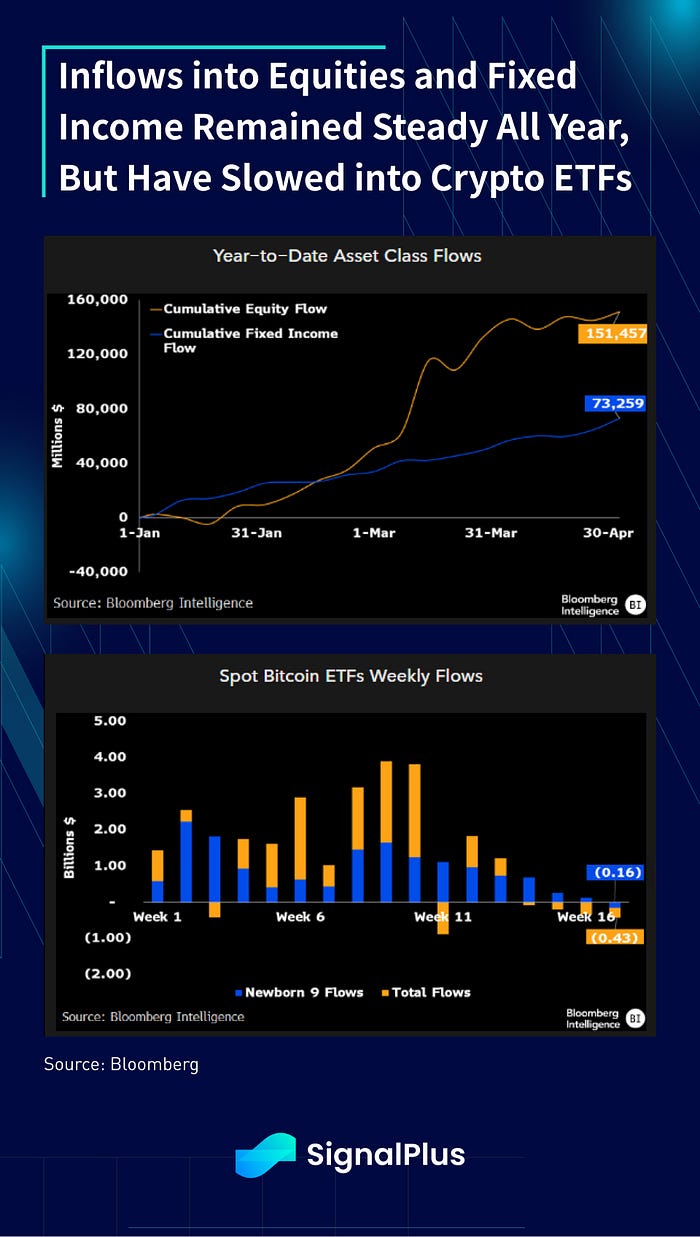

On flows, inflows remained steady all year for equities and fixed income and shows no signs of stopping despite current valuations. On crypto, ETFs saw their 3rd weekly outflows with Greyscale showing another massive -459M of selling today (IBIT data not yet updated), leading to a late NY 2–3% drop in BTC prices on the outflow data.

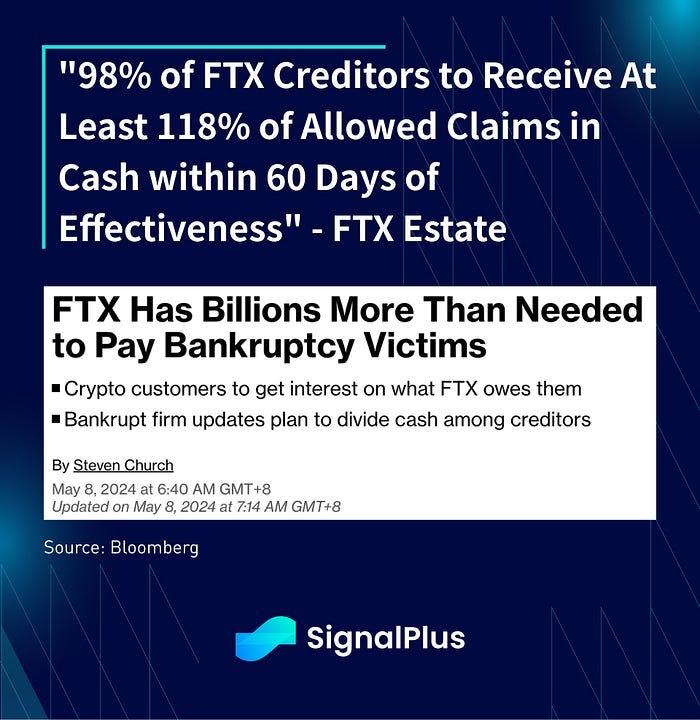

On a more positive note, the FTX bankruptcy estate announced that “98% of FTX Creditors to Receive At Least 118% of Allowed Claims in Cash within 60 Days of Effectiveness” and “Other Creditors to Receive 100% of Allowed Claims plus Billions in Compensation for the Time Value of Their Investments” on their official filing. After disposing all of its assets, FTX expects to have as much as $16.3B in cash left over to distribute to its customers, significantly more than its creditor liability of $11B. Ironic enough, this will go down as probably the largest single liquidity ‘off-ramp’ event in crypto history. Will the creditors pile these recoveries back into crypto, or will find their way back into conventional assets? Interesting times we live in.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments