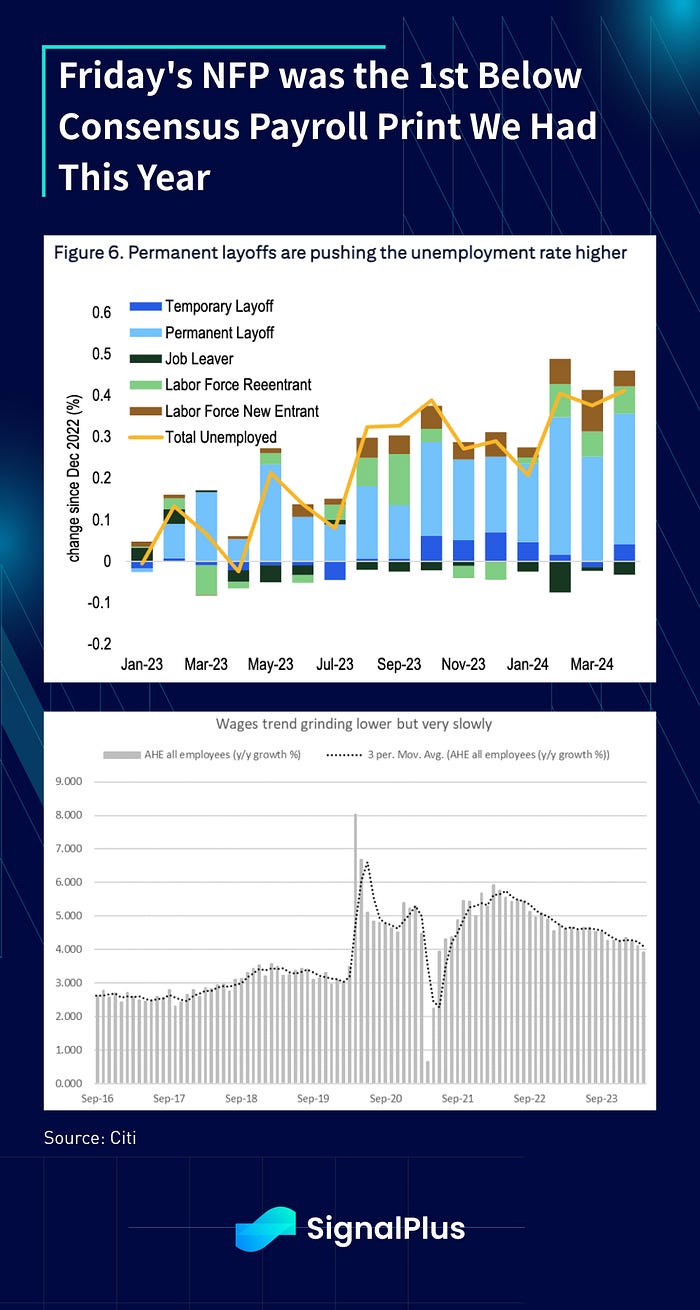

For the first time all year, we had a below-consensus payroll print (that didn’t surprise to the upside), with headline job creation coming in at +175k (from a previous average pace of ~275k), and the unemployment rate unexpectedly rising from 3.83% to 3.87%.

Other higher frequency and alternative measures of labour conditions have already been cooling, such as with the recent JOLTS report that has been showing a lower job openings to unemployed ratio, as well as a multi-year low in the private sector hiring and quit rates.

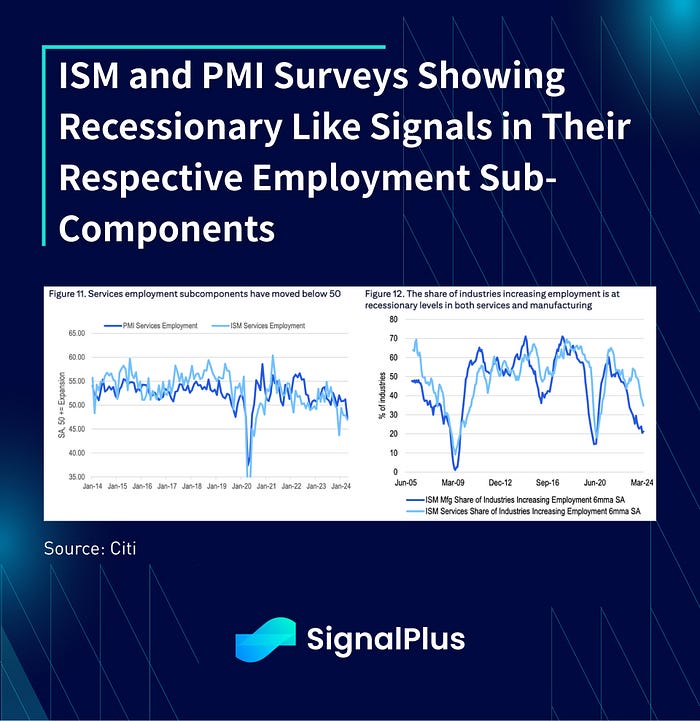

Furthermore, weak hiring trends have been quite pronounced with smaller businesses, with employment subcomponents weakening across both ISM and PMI surveys and the % of firms that are hiring across services and manufacturing sectors falling to levels more typically seen in a recession.

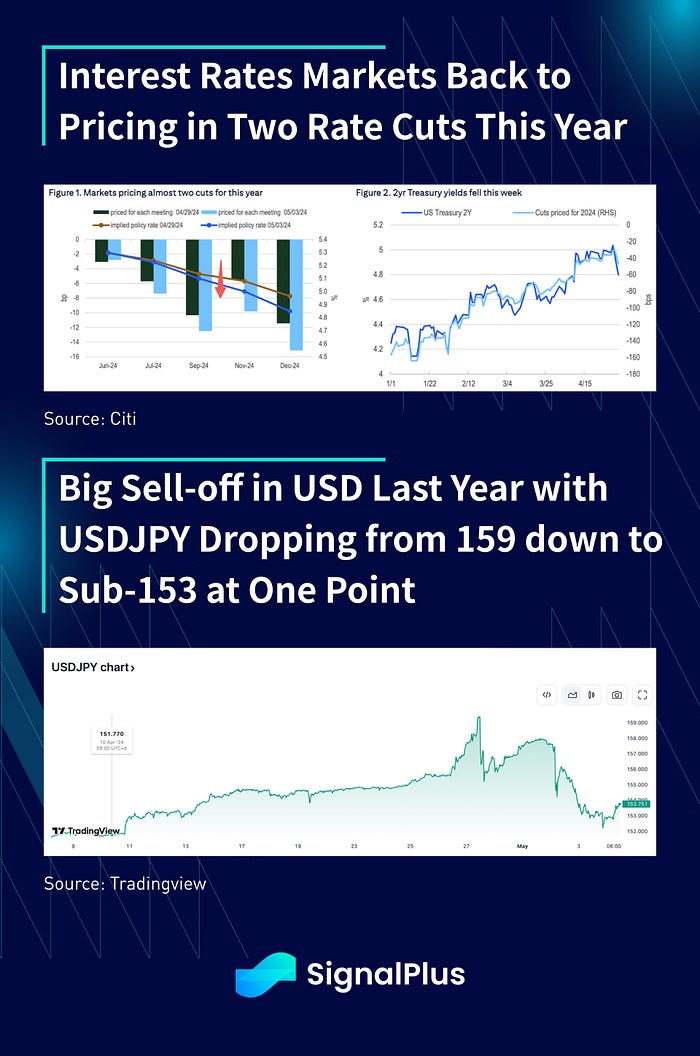

Recall our Friday commentary where we noted that the risk-reward for the NFP was asymmetrically skewed to the dovish wide, especially given the Fed’s FOMC explicit guidance that they are increasing their vigilance against a weakening labour market, and are willing to ignore recent bouts of inflation. And a softening labour market was what we saw, sparking yet another relief risk rally as rate cuts were back in the fold.

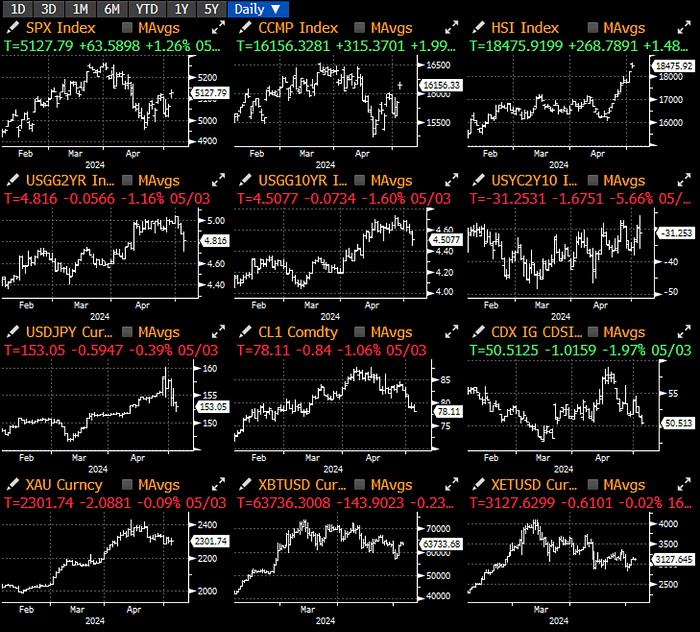

2yr treasuries fell from 5% back down to 4.8%, 10y yields are back at 4.5%, in abull steepening move, and 2024 rate cuts back to pricing in nearly 2 full cuts by year-end. Tech stocks rallied 2%, with SPX closing above 5100, and USDJPY dropped from a high of 159 last week to 152.5 over the past 48 hours. All-in-all, a strong goldilocks relief rally to close the week with market sentiment buoyed by a dovish rate backdrop.

Marco data will be quiet this week with Fed-speak likely to take precedent over second-tier US data. China will see money supply/ aggregate financing data this week, while the US will see Barkin, Williams, Kashkari, Jerrferson, Collins, Cook, Bowman taking turns to chime in on policy this week. After a few weeks of risk-flushing out, positioning is likely much cleaner compared to March, with sentiment likely to have found a near-term floor, as least until data starts to point towards more ‘hard-landing’ concerns (if that ever happens). SPX realized volatility has remained very low as investors have been busy adjusting their portfolio mix, rather than bailing out of stocks outright, with Bloomberg reporting a change in SPX leadership amidst the current correction period, albeit a bit of a musical chairs amongst the ‘magnificient 7’. We wouldn’t be surprised to see a slow, upward grind in risk assets from here.

With crypto exhibiting increasing correlation to macro sentiment, prices rebounded smartly on Friday with spot breaking >$64k during the weekend as sentiment shifted back towards an easier Fed / lower forward rates / stronger equity prices even as spot gold delivered a weak showing. US ETF inflows were strong on Friday at +$378M, with even Grayscale showing its first inflow in recent memory at +$63M. We maintain our bias from last week where we felt that risk-reward has turned more neutral at the current macro juncture, and would expect to be better buyers on dips in the near term.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments