The cross-asset risk-off theme continued and arrived earlier than the market. The US session opened with mixed US ISM data which saw the index linger around 2-year lows (47.4) and reporting the 14th consecutive month of contraction. The sub-components saw a larger drop than expected in prices paid, offset by a strong employment sub-index and new export orders.

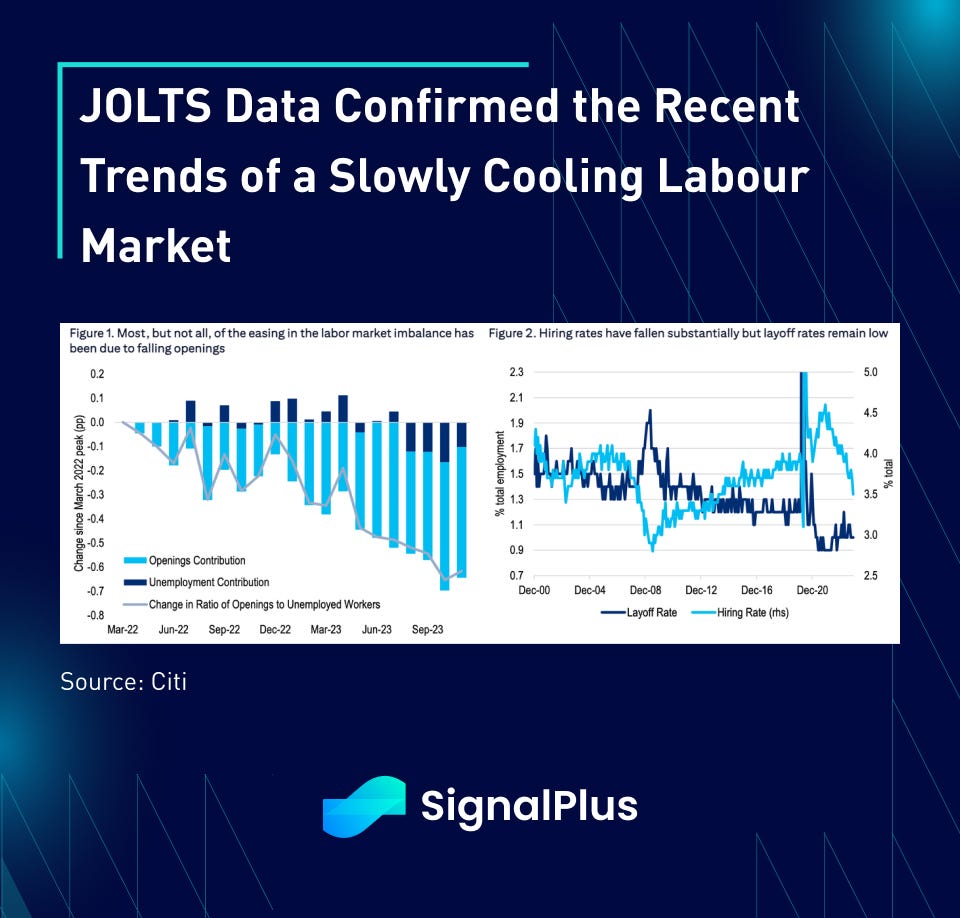

JOLTS job openings fell in November with large openings seen in the construction sector as the red-hot housing sector are finally seeing early cracks in its facade, coupled with revised openings across both the education and health services sectors as well. The quit rate fell further in November down to 2.2%, while the hiring rate also eased off to 3.5%, continuing the recent trend of a weakening labor market. However, the ratio of openings to unemployed remained at an elevated 1.4-to-1 ratio, well above pre-pandemic levels, and lay-off rates also remain low, suggesting no immediate and critical concerns… yet.

The Dec FOMC Minutes elicited more market excitement, where initial headlines suggested a reticence for any early rate cuts, citing that rates ‘could stay at peak longer than anticipated’. Other comments were more even-heeled, with further comments on concerns over easing financial conditions offset against the acknowledgment that inflation has peaked and that officials discussed the possibility of halting QT at some point.

‘Hawkish’ Headlines

*SEVERAL SAID RATE COULD STAY AT PEAK LONGER THAN ANTICIPATED

*FED OFFICIALS SAW POLICY REMAINING RESTRICTIVE FOR SOME TIME

*MANY SAID EASING FINANCIAL CONDITIONS COULD PRESENT CHALLENGE

‘Dovish’ Headlines

*FED MINUTES: OFFICIALS SAW POLICY RATE LIKELY AT OR NEAR PEAK

*OFFICIALS ACKNOWLEDGED PROJECTIONS SHOW CUTS BY END-2024

*FOMC SAW UPSIDE RISKS TO INFLATION AS HAVING DIMINISHED

*MINUTES SHOWED DISCUSSION ON WHEN TO FLAG BALANCE-SHEET CHANGE

Source: WSJ, Bloomberg

On the Topic of a Slowing Down of Quantitative Tightening:

“Several participants remarked that the Committee’s balance sheet plans indicated that it would slow and then stop the decline in the size of the balance sheet when reserve balances are somewhat above the level judged consistent with ample reserves. These participants suggested that it would be appropriate for the Committee to begin to discuss the technical factors that would guide a decision to slow the pace of runoff well before such a decision was reached in order to provide appropriate advance notice to the public.”

Source: Bloomberg, Federal Reserve

Treasury yields ended gently lower on the day, with early corporate hedging pressures giving way to better bond buying thanks to the drop in ISM prices paid and a slowdown in JOLTS data. Supportive comments from Richmond Fed’s Barking (Fed making “real progress” on inflation) and balanced FOMC minutes also helped, particularly on the new insights regarding a potential QT reduction being discussed.

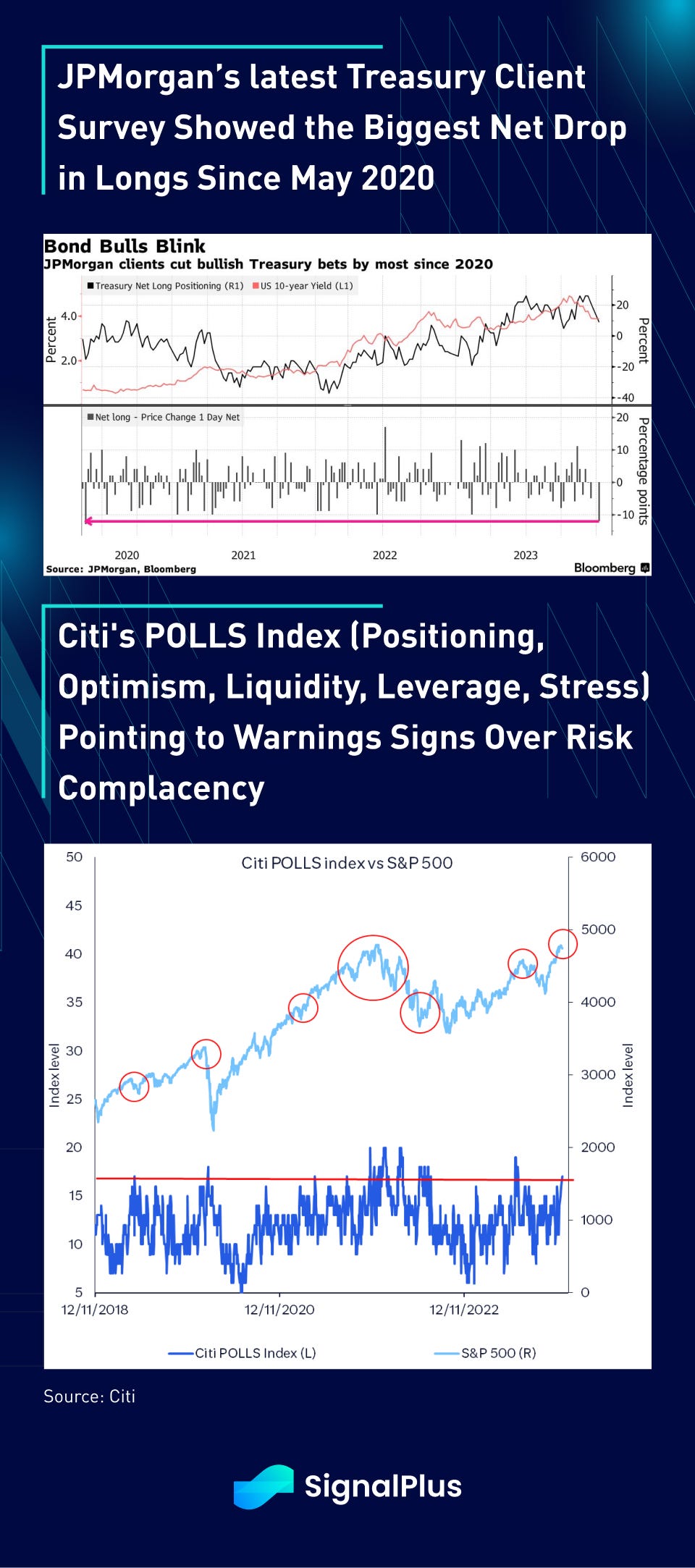

Weak equity markets (SPX/Nasdaq lost another -1% yesterday) also led to some risk-off related hedging in bonds, while a significant drop in fixed income longs from JPM’s latest Treasury client survey points to a cleaner position setup heading into NFP. On the other hand, equity longs remain off-side to start the new year with a number of sentiment surveys, such as Citi’s ‘POLLS’ index flashing potential warning signs with investor over-complacency to start the year.

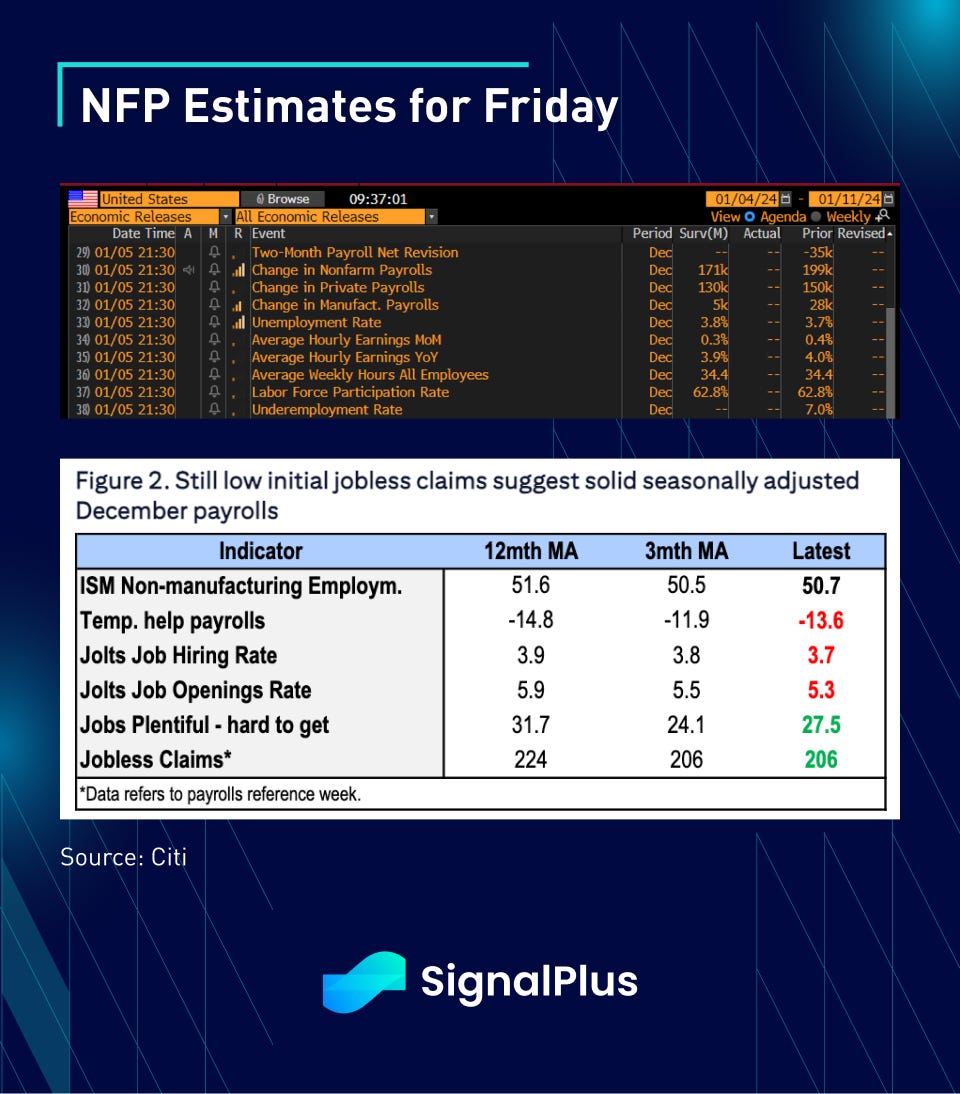

On NFP, Bloomberg consensus shows a headline print of +171k with an unemployment rate of 3.8% and 0.3% on AHE. However, the market is likely expecting an upside bias to the print thanks in part to positive seasonal adjustments around the new year. An upward payrolls beat with AHE stuck close to 4% YoY should give the Fed a hawkish pause in their economic assessments, though we wouldn’t expect officials to go out of their way to react hawkishly to stronger data. Risk-reward likely favours a buy-the-dip move should risk assets come off aggressively post-NFP.

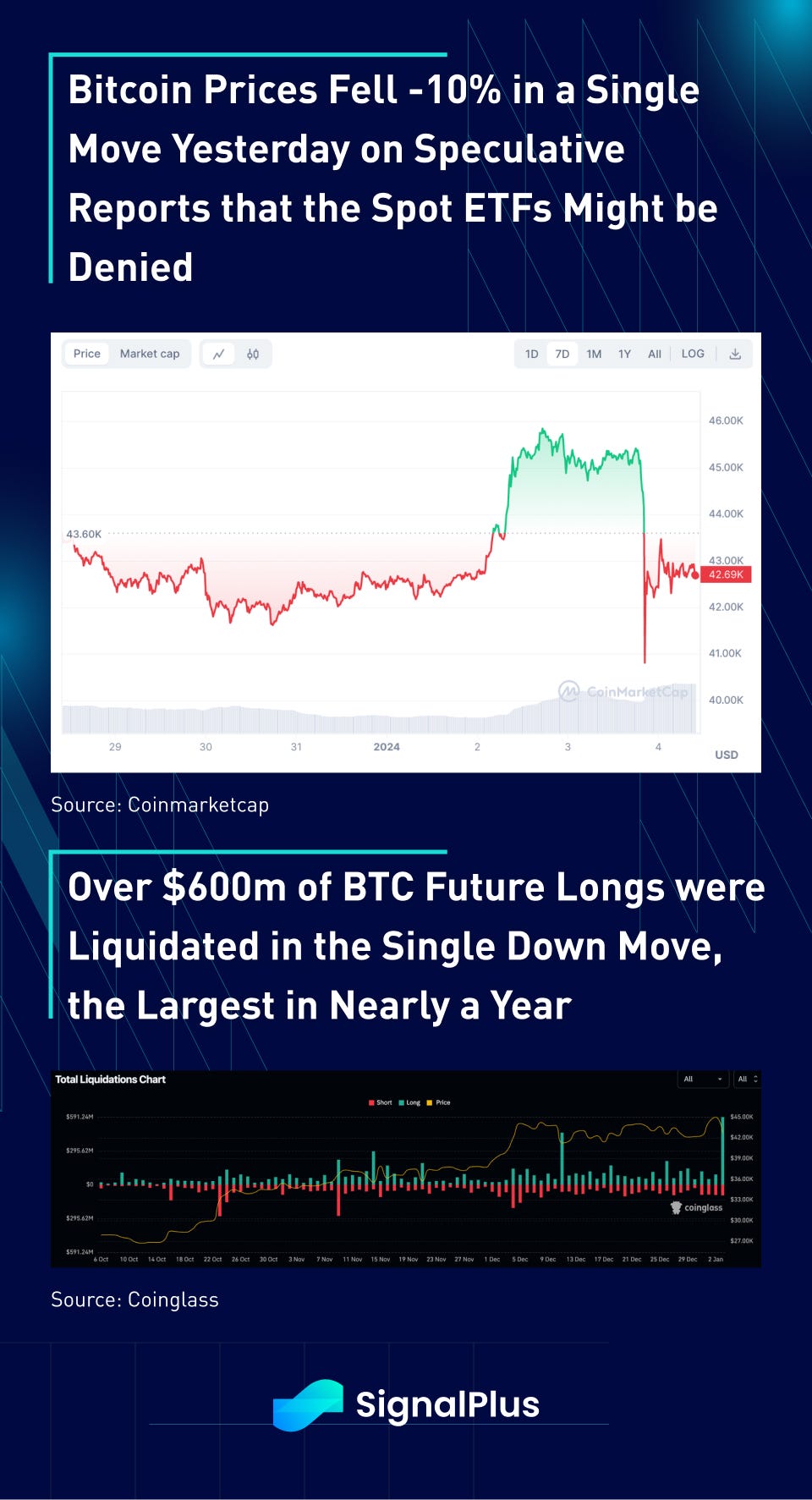

In crypto, we saw the 1st roller-coaster ride of the year, where BTC fell from over $45k to $41k in a single ‘candle’ with over $600mm in long BTC futures liquidated in a hurry, the largest stop-outs in more than 6 months. With speculative fervor running at extremes as we inch closer to the imminent SEC decision, a commentary piece report out of Matrixport suggested that the SEC would reject the spot ETF approval, and was largely blamed for sparking the spot sell-off around the NY open.

The surprising reaction to the commentary and the extent of pricing carnage sparked various reactions and clarifications on Twitter, including from Mr. Jihan Wu personally, and clarifications from Bloomberg analyst Balchunas that the spot ETF plans remain on track with a “90%” probability based on their own market intelligence. Stay safe out there!

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Options Toolkits: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Comments