Couple of mixed data prints out of the US yesterday, with the early 8:15am ADP showing a stronger than expected jobs print with +184k jobs added and +15k in prior revisions. A particular strength was noted in the ‘job changer’ pay growth, which saw an over 10% jump in pay YoY, with accompanying commentary stating that the biggest wage increases came in the areas of construction, financial services, and manufacturing.

On the other hand, US ISM services fell -1.2 points to 51.4 in March, with a large drop (-5.2 points) in prices paid and sits at the lowest levels since March 2020. The rest of the components were mixed, but the miss in prices paid and employment sub-components helped temporarily to stall the grind higher in bond yields on the day.

Over at the end, Atlanta Fed President Bostic reiterated his hawkish stance by sticking to just a single rate cut in Q4, caveating by saying that it is dependent on his economic view coming to fruition, though “his contacts” are not informing him of any weakness coming in the employment markets yet.

On the other hand, Powell struck a more dovish tone by insisting that the disinflation process shall continue despite strong economic growth, and implies that rates are currently restrictive and needs to come down. Furthermore, his Q&A were also littered with dovish tidbits such as “productive capacity has moved up perhaps more than output”, “large increase in population may have helped to bring inflation down”, and there “maybe be more supply side gains to be had” with regards to capacity pressures.

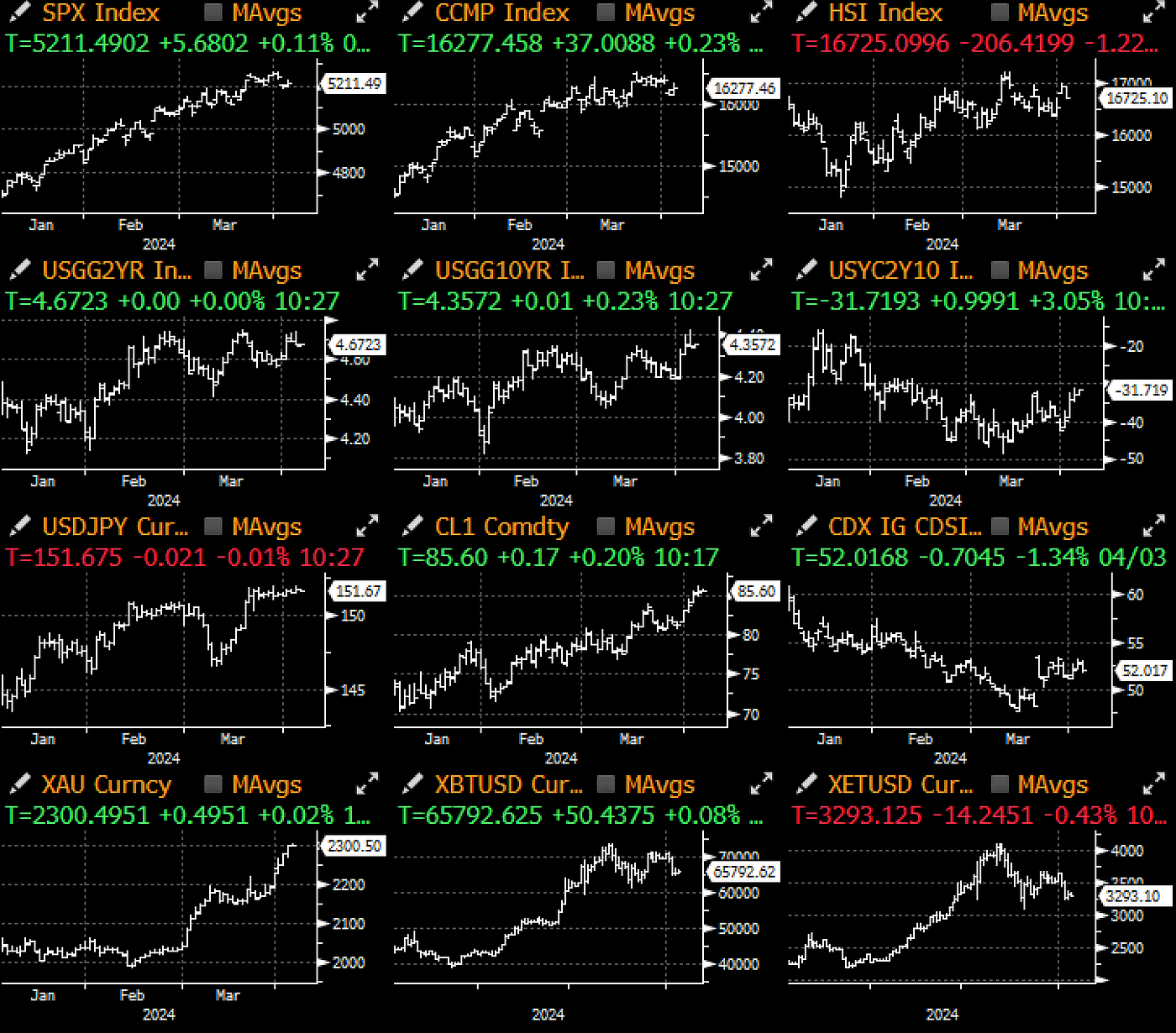

10y treasury yields remained at YTD highs but without much market fear (yet), though they might servce to be a headwind for stocks in Q2 based on prior factor analysis.

Looking ahead, Friday’s NFP is expected to remain solid with a slight slowdown, though the wide divergence between the establishment survey (strong) vs household employment data (much weaker) continues to be major source of variability. Given the recent sell off in fixed income, markets are probably entering into the market with a hawkish bias, with a weaker NFP report likely to cement the odds of June cuts back to above 75%.

In crypto, ETF inflows were much stronger yesterday, with both Fidelity and Blackrock adding substantial inflows, offseting the surprising ARK outflows from the day before. Net inflows totalled $220mm including -75mm from Grayscale, helping ot stabilize BTC prices at around the $65.5k area as market tries to regain its footing.

You can search SignalPlus in the Plugin Store of ChatGPT 4.0 to get real-time crypto information. To receive timely updates and engage with a broader community, we cordially invite you to join and follow our official link for seamless communication and interaction with community members.

SignalPlus Official Links

Trading Terminal: https://t.signalplus.com

Twitter: https://twitter.com/SignalPlus_Web3

Discord: https://discord.gg/signalplus

Telegram: https://t.me/SignalPlus_Official

Medium: https://medium.com/@signalplus_web3

Website: https://www.signalplus.com/

Trading Ideas: https://t.me/SignalPlus_Playground

Comments